MGMT 20000 Lecture Notes - Lecture 26: Relative Risk, Interest Expense

14 Nov 2018

School

Department

Course

Professor

Document Summary

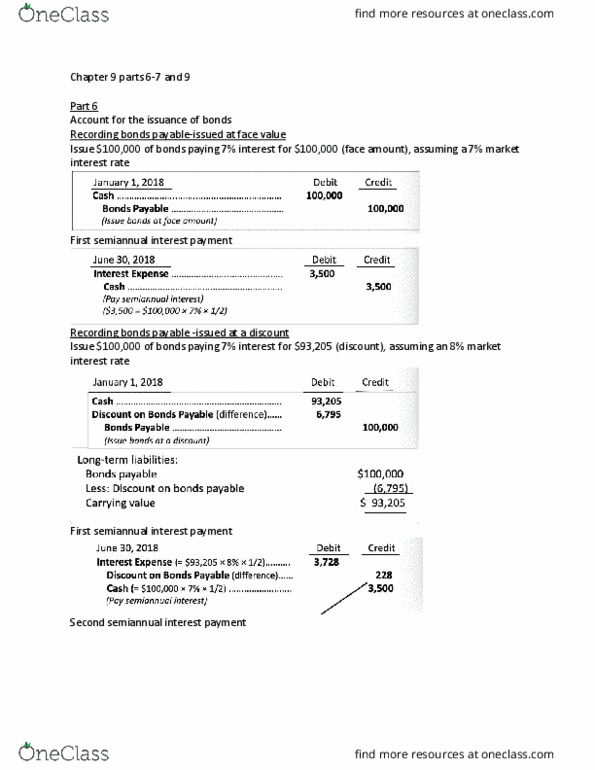

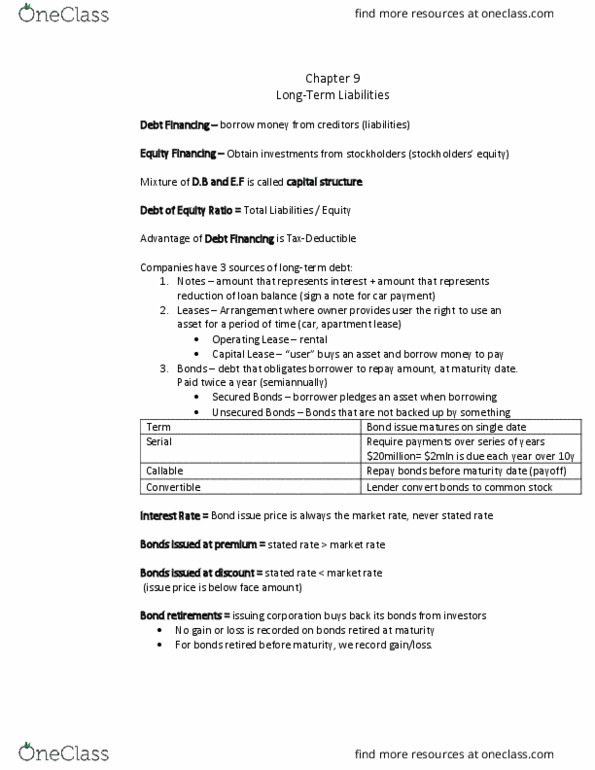

Accounting valuation for bonds at a date of issuance. Issuance and marketing of bonds to the public. Selling price of a bond issue is set by the. On jan. 1, 2018, ,000 of bonds are issued with a stated interest rate of 7%. The bonds are due on 10 years with interest payable semiannually on june 30 and dec. 31 each year. Pricing bonds issued at face (market interest rate of 7% / slated interest rate. Bonds: ,000 at 7% interest and a 7% market interest rate. If the market interest rate at the date of issuance of a bond exceeds the face or slated interest rate, the bond will be sold at premium. Face value is the principle amount of a bond as stated on the bond certificate. Investors are willing to invest in the bonds at rates that are higher than the stated interest rate. If bonds are issued at a premium, the face or stated interest rate is.