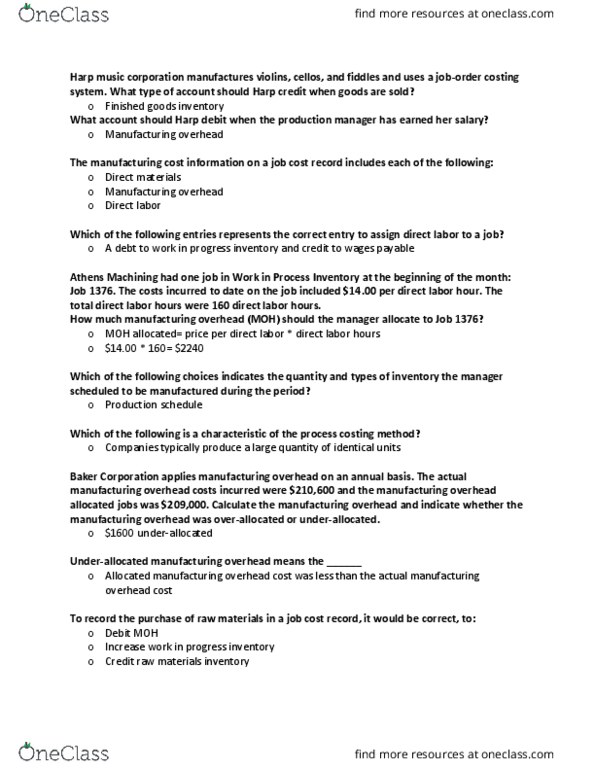

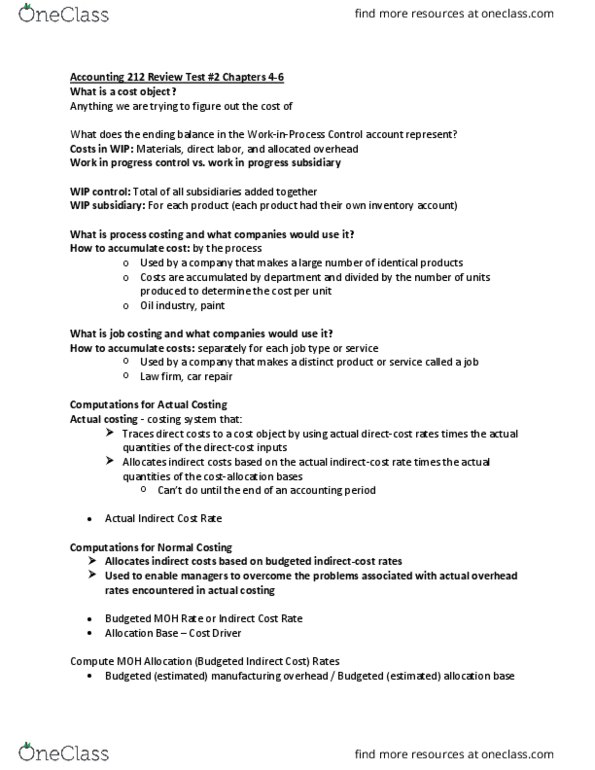

AC 212 Lecture Notes - Lecture 3: Production Schedule, Purchase Order, Financial Statement

Document Summary

Get access

Related Documents

Related Questions

1.) On January 31, Village Bank had 500,000 shares of $3 parvalue common stock outstanding. On that date, the company declareda 10% stock dividend when the market price of the stock was $62 pershare. The immediate effect of this dividend upon Village Bankwas:

A.)A reduction in cash of $3,794,500. | |||||||||||||||||||||||||||||||||||||||||

B.) A reduction in retained earnings of $3,100,000. | |||||||||||||||||||||||||||||||||||||||||

C.) A reduction in retained earnings of $150,000. | |||||||||||||||||||||||||||||||||||||||||

| D.) A liability to the stockholders of $150,000. 2.) Mayfair Corporation has outstanding 70,000 shares of $1 parvalue common stock as well as 20,000 shares of 7%, $100 par valuecumulative preferred stock. At the beginning of the year, thebalance in retained earnings was $800,000, and one year's dividendswere in arrears. Net income for the current year is $580,000.Compute the balance in retained earnings at the end of the year ifMayfair Corporation pays a dividend of $3 per share on its commonstock this year.

3.) During the years 2009 through 2011, Powers, Inc., reportedthe following amounts of net income (dollars in thousands):

4.) Hines Cannery issued capital stock in 2009 for $700,000.During 2009 the company paid dividends of $250,000. What is theeffect of these events in Hines' statement of cash flows for2009?

6.) Which of the following is a characteristic of manufacturingoverhead in a job order cost system?

|

7.) A job order cost system traces direct materials cost to aparticular job by means of:

A.) | Materials requisitions. |

B.) | A production budget. |

C.) | The Materials Inventory controlling account. |

D.) | A debit to the job cost sheet for the job. |

8.) Which of the following costing systems would always use jobcost sheets?

A.) | Job order costing. |

B.) | Process costing. |

C.) | Activity-based costing. |

D.) | All three systems. |

9.) Edwards Auto Body uses a job order cost system. Overhead isapplied to jobs on the basis of direct labor hours. During thecurrent period, Job No. 337 was charged $425 in direct materials,$475 in direct labor, and $190 in overhead. If direct labor costsan average of $16 per hour, the company's overhead application rateis:

A.) | $7.27 per direct labor hour. |

B.) | $6.40 per direct labor hour. |

C.) | $17.50 per direct labor hour. |

D.) | $40 per direct labor hour. |

10.) Marty's Metal Shop uses a job order cost system. It appliesoverhead to jobs at a rate of 175% of direct labor costs. Job No.2617 required $800 in direct labor costs. The job was initiallybudgeted to require $850 in direct labor costs. Overhead applied toJob No. 2617 during the period amounted to:

A.) | $850. |

B.) | $1,400. |

C.) | $1,275. |

D.) | Some other amount. |

11.) In a job cost system, the Work-in-Process Inventorycontrolling account may be reconciled to the total of the:

A.) | Employee time cards. |

B.) | Materials requisitions. |

C.) | Work-in-Process Inventory records for each department orprocess. |

D.) | Job cost sheets. |

12.) For the month of December, its first month of operations,the Radcliffe Corporation completed and transferred 800 units ofproduct costing $80,000 to produce to Finished Goods Inventory. IfRadcliffe sold 650 units during the same month, how much was costof goods sold for the same period?

A.) | $80,000. |

B.) | $8,000. |

C.) | $6,500. |

D.) | $65,000. |

13.) The computation of equivalent full units is generally notnecessary when:

A.) | Beginning work-in-process inventories are significantly largerthan ending work-in-process inventories. |

B.) | Beginning and ending work-in-process inventories differ onlyslightly. |

C.) | The number of units in ending work-in-process exceeds the numberof units completed and transferred to finished goods during theperiod. |

D.) | Per-unit costs become distorted as a result of not computingequivalent full units of production. |

14.) During July, the equivalent full units of direct materialsadded to the product worked on by Department A amounted to a totalof 90,000 applied as follows: beginning inventory, 20,000 units;units started and completed in July, 60,000 units; and endinginventory, 10,000 units. Assuming that the cost of direct materialsrequisitioned by the department in July was $135,000; the amount ofthe materials cost to be assigned to the ending inventory wouldbe:

A.) | $16,875. |

B.) | $54,000. |

C.) | $15,000. |

D.) | $18,000. |

Hello,

When attempting to access the Study Guide/Workbook to AccompanyManagerial Accounting (1st edition), I need assistance. In thet-tables, h. is showing to be $46,700. However when I read h. atthe top for given data, it reads "completed all jobs but one; thejob cost sheet for this job shows $2100 for direct materials $2000for direct labor $4100 applied overhead". Can you please help me tounderstand where the $46700 is coming from? Is there a formula? Iam trying to complete the work in process inventory and finishedgoods inventory t-tables.

Thank you in advance for your assistance.

Question:

Study Guide/Workbook to accompany Managerial Accounting (1stEdition)

Chapter 2, Problem 5PSA

Problem

Recording Manufacturing Costs and AnalyzingManufacturing Overhead

Christopherâs Custom Cabinet Company uses a job order costingsystem with overhead applied as a percentage of direct labor costs.Inventory balances at the beginning of 2009 follow:

Raw materials inventory | $15,000 |

Work in process inventory | 5,000 |

Finished goods inventory | 20,000 |

The following transactions occurred during January:

(a) Purchased materials on account for $26,000.

(b) Issued materials to production totaling $22,000, 90percent of which was traced to specific jobs and the remaindertreated as indirect materials.

(c) Payroll costs totaling $15,500 were recorded asfollows:

$10,000 for assembly workers

3,000 for factory supervision

1,000 for administrative personnel

1,500 for sales commissions

(d) Recorded depreciation: $6,000 for machines, $1,000for office copier.

(e) Had $2,000 in insurance expire, allocated equallybetween manufacturing and administrative expenses.

(f) Paid $6,500 in other factory costs in cash.

(g) Applied manufacturing overhead at a rate of 200percent of direct labor cost.

(h) Completed all jobs but one; the job cost sheet forthis job shows $2,100 for direct materials, $2,000 for directlabor, and $4,000 for applied overhead.

(i) Sold jobs costing $50,000; the company usescost-plus pricing with a markup of 30 percent.

Required:

1.Set up T-accounts, record the beginningbalances, post the January transactions, and compute the finalbalance for the following accounts:

Raw Materials Inventory

Work in Process Inventory

Finished Goods Inventory

Cost of Goods Sold

Manufacturing Overhead

Selling and Administrative Expenses

Sales Revenue

Other accounts (Cash, Payables, etc.)

2. Determine how much gross profit the companywould report during the month of January beforeany adjustment is made for the overhead balance.

3. Determine the amount of overâor underappliedoverhead.

4. Compute adjusted gross profit assuming thatany overâor underapplied overhead balance is adjusted directly toCost of Goods Sold.

Step-by-step solution

Step 1 of 1

Req. 1

Raw Materials Inventory | Work in Process Inventory | Finished Goods Inventory | |||

1/1 15,000 | b. 22,000 | 1/1 5,000 | h. 46,700 | 1/1 20,000 | i. 50,000 |

a. 26,000 | b. 19,800 | h. 46,700 | |||

Bal. 19,000 | c. 10,000 | Bal. 16,700 | |||

g. 20,000 | |||||

Bal. 8,100 | |||||

Cost of Goods Sold | Manufacturing Overhead | Selling and Administrative Expenses | |

i. 50,000 | b. 2,200 | g. 20,000 | c. 2,500 |

c. 3,000 | d. 1,000 | ||

d. 6,000 | e. 1,000 | ||

e. 1,000 | Bal. 4,500 | ||

f. 6,500 | |||

Bal. 1,300 Overapplied | |||

Sales Revenue | Other Accounts (Cash, Payables, etc.) | ||

i. 65,000 | i. 65,000 | a. 26,000 | |

c. 15,500 | |||

d. 7,000 | |||

e. 2,000 | |||

f. 6,500 | |||

Bal. 8,000 | |||

Supporting Calculations:

b. Direct Materials $22,000 x 90% = $19,800;

Indirect Materials $22,000 x 10% =$2,200

c. Selling and administrative salaries = $1,000 + $1,500 =$2,500

g. Applied manufacturing overhead = $10,000 X 200% = $20,000

h. Ending Balance in WIP = $2,100 + $2,000 + $4,000 = $8,100

Cost of Goods Manufactured = $5,000 +$19,800 + $10,000 + $20,000 - $8,100 =

$46,700

i. Sales Revenue = $50,000 X 1.3 = $65,000

Req. 2

Unadjusted gross profit = $65,000 - $50,000 = $15,000

Req. 3

Manufacturing overhead is $1,300 overapplied.

Req. 4

Adjusted gross profit = $65,000 â ($50,000 - $1,300) =$16,300

Comment