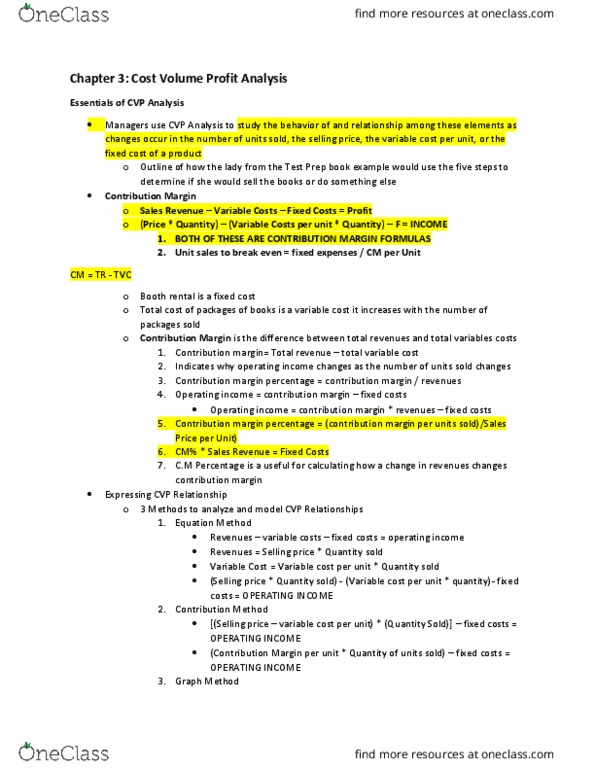

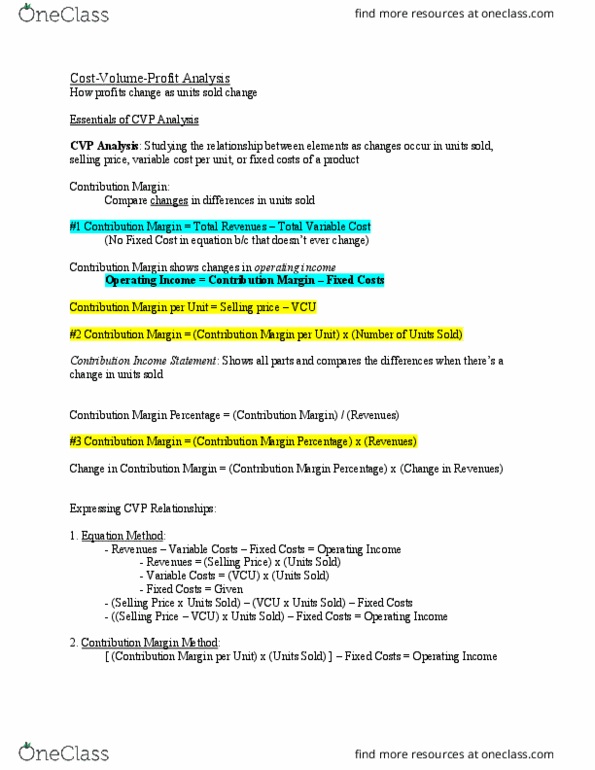

33:010:275 Lecture Notes - Lecture 5: Earnings Before Interest And Taxes, Contribution Margin, Expense Ratio

Document Summary

Get access

Related Documents

Related Questions

Shown here is an income statement in thetraditional format for a firm with a sales volume of 7,900 units.Cost formulas also are shown: |

| Revenues | $ | 34,500 | |

| Cost of goods sold ($5,600 + $2.2/unit) | 22,980 | ||

| Gross profit | $ | 11,520 | |

| Operating expenses: | |||

| Selling ($1,180 +$0.1/unit) | 1,970 | ||

| Administration ($3,550 +$0.2/unit) | 5,130 | ||

| Operating income | $ | 4,420 | |

| | | ||

the optional account names for the three boxes under variableexpense are:

Requirement 1: |

Prepare an income statement in the contributionmargin format. (Omit the "$" sign in yourresponse.) |

| revenues | $ | |

| Variable expenses: | ||

| cost of good sold | $ | |

selling expense | ||

| administrative expense | ||

| Total variable expenses | ||

| Contribution margin | $ | |

| Fixed expenses: | ||

| costof good sold | $ | |

| admistratitve expenses | ||

| selling expenses | ||

| Total fixed expenses | ||

| operating income | $ | |

| | ||

| Requirement 2: |

Calculate the contribution margin per unit andthe contribution margin ratio. (Omit the "$" and "%" signs inyour response. Round contribution margin per unit to 2 decimalplaces and contribution margin ratio to whole number.) |

| Contribution margin per unit | $ |

| Contribution margin ratio | % |

| Requirement 3: | |

| (a) | Calculate the firm's operating income (or loss)if the volume changed from 7,900 units to 11,850 units.(Do not round yourintermediate calculations. Round your answer to the nearest dollaramount. Omit the "$" sign in your response.) |

| operating income | $ |

| (b) | Calculate the firm's operating income (or loss)if the volume changed from 7,900 units to 3,950 units. (Do not round your intermediatecalculations. Round your answer to the nearest dollar amount. Inputall amount as positive values. Omit the "$" sign in yourresponse.) |

| operating income | $ |

| Requirement 4: | |

| Refer to your answer to requirement 1 for total revenues of$34,500. | |

| (a) | Calculate the firm%u2019s operating income (orloss) if unit selling price and variable expenses per unit do notchange, and total revenues increase by $10,500. (Do not round your intermediatecalculations. Round your answer to the nearest dollar amount. Omitthe "$" sign in your response.) |

| operating income | $ |

| (b) | Calculate the firm's operating income (or loss)if unit selling price and variable expenses per unit do not change,and total revenues decrease by $3,000. (Do not round your intermediatecalculations. Round your answer to the nearest dollar amount. Inputthe amount as positive value. Omit the "$" sign in yourresponse.) |

| operating income | $ |

Mathews Company manufactures only one product. For the year ended December 31, the The excess of sales over variable costs.contribution margin increased by $20,280 from the planned level of $681,720. The president of Mathews Company has expressed some concern about this increase and has requested a follow-up report.

The following data have been gathered from the accounting records for the year ended December 31:

| Actual | Planned | DifferenceâIncrease (Decrease) | ||||

| Sales | $1,339,000 | $1,318,980 | $20,020 | |||

| Variable costs: | ||||||

| Variable cost of goods sold | $507,000 | $533,520 | $(26,520) | |||

| Variable selling and administrative expenses | 130,000 | 103,740 | 26,260 | |||

| Total variable costs | $637,000 | $637,260 | $(260) | |||

| Contribution margin | $702,000 | $681,720 | $20,280 | |||

| Number of units sold | 13,000 | 14,820 | ||||

| Per unit: | ||||||

| Sales price | $103 | $89 | ||||

| Variable cost of goods sold | 39 | 36 | ||||

| Variable selling and administrative expenses | 10 | 7 | ||||

Required:

1. Prepare a contribution margin analysis report for the year ended December 31.

| Mathews Company | ||

| Contribution Margin Analysis | ||

| For the Year Ended December 31 | ||

| Planned contribution margin | $ | |

| Effect of change in sales: | ||

| Sales quantity factor | $ | |

| Unit price factor | ||

| Total effect of change in sales | ||

| Effect of changes in variable cost of goods sold: | ||

| Variable cost quantity factor | $ | |

| Unit cost factor | ||

| Total effect of changes in variable cost of goods sold | ||

| Effect of changes in variable selling and administrative expenses: | ||

| Variable cost quantity factor | $ | |

| Unit cost factor | ||

| Total effect of changes in variable selling and administrative expenses | ||

| Actual contribution margin | $ | |

2. At a meeting of the board of directors on January 30, the president, after reviewing the contribution margin analysis report, made the following comment:

It looks as if the price increase of $14 was a favorable tradeoff for decreased sales volume, yet variable cost of goods sold was less than planned and variable selling and administrative expenses were out of control and needed to be investigated. He went on to say that since the favorable tradeoff between higher price and lower sales volume was so successful, the company should consider increasing the sales price to $130.

Do you agree or disagree with the president's proposal and which reason would best explain your decision about the data?

a) Disagree with the president because the majority of the decrease in the variable cost of goods sold was due to the variable cost quantity factor and the increased variable selling and administrative expenses are probably a result additional selling efforts needed to be competitive at higher prices.

b) Agree with the president because the unit cost factor for the variable selling and administrative cost is greater than the unit cost factor for the variable cost of goods sold, making an investigation necessary.

c) Agree with the president because the total effect of change in sales is greater than the total effect of changes in variable cost of goods sold, making an additional price raise attractive for more profits.

d) Disagree with the president because the contribution margin as a percentage of sales is greater for the planned sales level than the actual sales level, making his concern about variable selling and administrative expenses unwarranted.

e) Agree with the president because the majority of the decrease in the variable cost of goods sold was due to the sales price factor, as well as an increase in the variable selling and administrative expenses as a percentage of sales, making an additional price raise attractive for more profits.

Phoenix Companyâs 2017 master budget included the following fixed budget report. It is based on an expected production and sales volume of 15,000 units.

| PHOENIX COMPANY Fixed Budget Report For Year Ended December 31, 2017 | |||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| Sales | $ | 3,150,000 | |||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| Cost of goods sold | |||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| Direct materials | $ | 945,000 | |||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| Direct labor | 225,000 | ||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| Machinery repairs (variable cost) | 45,000 | ||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| DepreciationâPlant equipment (straight-line) | 300,000 | ||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| Utilities ($45,000 is variable) | 195,000 | ||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| Plant management salaries | 200,000 | 1,910,000 | |||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| Gross profit | 1,240,000 | ||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| Selling expenses | |||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| Packaging | 90,000 | ||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| Shipping | 105,000 | ||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| Sales salary (fixed annual amount) | 235,000 | 430,000 | |||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| General and administrative expenses | |||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| Advertising expense | 125,000 | ||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| Salaries | 230,000 | ||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| Entertainment expense | 85,000 | 440,000 | |||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| Income from operations | $ | 370,000 | |||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

|

| |||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

The companyâs business conditions are improving. One possible result is a sales volume of 18,000 units. The company president is confident that this volume is within the relevant range of existing capacity. How much would operating income increase over the 2017 budgeted amount of $370,000 if this level is reached without increasing capacity?

| |||||||||||||||||||||||||||||||||||

An unfavorable change in business is remotely possible; in this case, production and sales volume for 2017 could fall to 12,000 units. How much income (or loss) from operations would occur if sales volume falls to this level? (Enter any loss with minus sign.)

| |||||||||||||||||||||||||