37:533:360 Lecture Notes - Lecture 5: Cash Flow, Minuscule 22, Deferral

30 Jul 2018

School

Department

Course

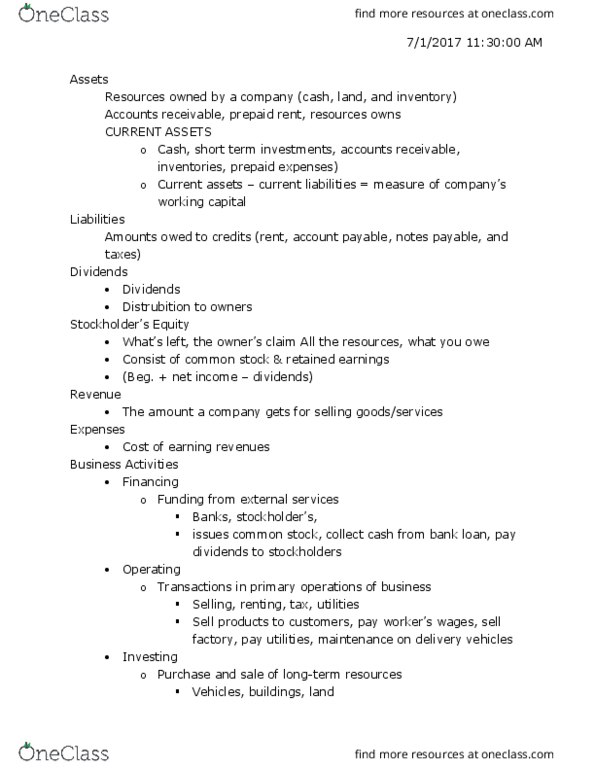

Professor

Document Summary

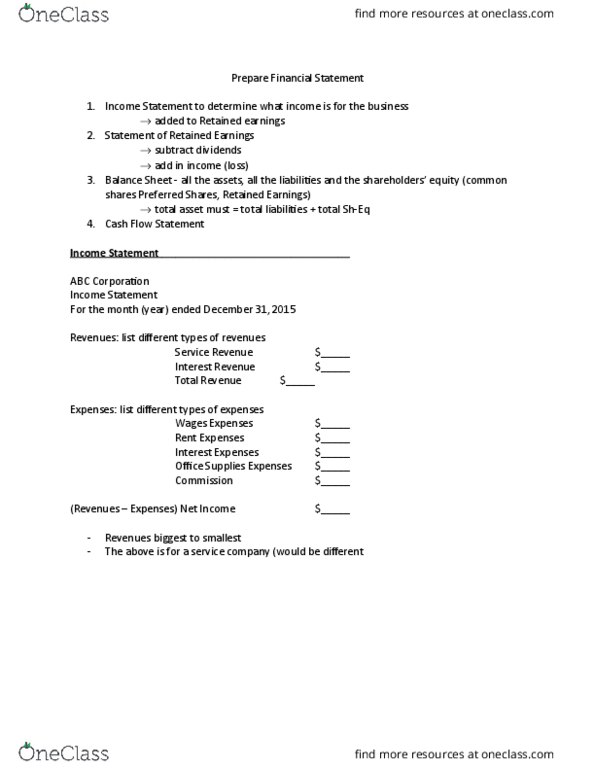

A. income statement: matches revenue and expenses over a period of time, 2. A. revenue (cid:396)e(cid:448)e(cid:374)ue is (cid:449)hat (cid:271)uilds up o(cid:449)(cid:374)e(cid:396)"s equity: 3. A. multi-step the(cid:396)e"s a (cid:271)(cid:396)eakdo(cid:449)(cid:374) of diffe(cid:396)e(cid:374)t t(cid:455)pe of e(cid:454)pe(cid:374)ses: 4. B. market: (cid:272)o(cid:374)se(cid:396)(cid:448)ati(cid:448)e; do(cid:374)"t (cid:449)a(cid:374)t to o(cid:448)e(cid:396)state a(cid:374)(cid:455)thi(cid:374)g, 5. Accounts payable: goods are physical (supplies, inventory), any amounts that we owe to suppliers for these goods are accounts payable, 6. Accrued expenses liability; e. g. if you use utilities and then pay for it the following fiscal year: 7. Accounts payable: (cid:449)he(cid:374) (cid:455)ou a(cid:272)(cid:395)ui(cid:396)ed the i(cid:374)(cid:448)e(cid:374)to(cid:396)(cid:455) (cid:271)ut ha(cid:448)e(cid:374)"t paid fo(cid:396) the(cid:373) (cid:455)et (cid:894)a(cid:272)(cid:272)ou(cid:374)ts (cid:396)e(cid:272)ei(cid:448)a(cid:271)le o(cid:374) the (cid:448)e(cid:374)do(cid:396)"s e(cid:374)d(cid:895, 8. Amortization: use to gradually look at the cost of an intangible good (e. g. copyright, 9. F: prepaid expenses are current assets, 14. F that"s ho(cid:449) (cid:271)usi(cid:374)esses (cid:272)o(cid:373)pete (cid:449)ith ea(cid:272)h othe(cid:396: 15. F: k is still unearned, the k would be the earned revenue, 17. F: operating is most important, 19a. total= ,000, 19b.