ACCT 301 Lecture 5: Chapter 5 Financial Study Guide

Document Summary

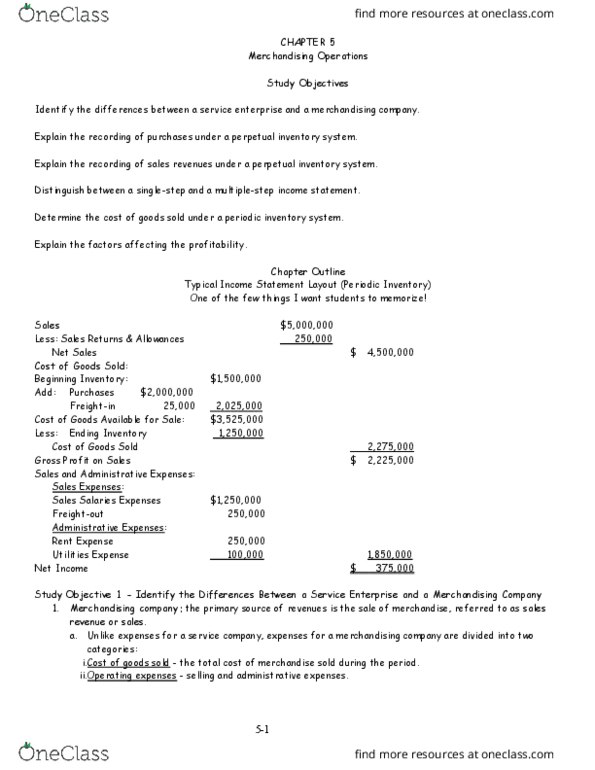

Merchandising companies that sell to retailers are known as wholesalers. Gross profit equals the difference between net sales revenues and cost of goods sold. Net income will result if gross profit exceeds operating expenses. Two categories of expenses in merchandising companies are cost of goods sold and operating expenses. The primary source of revenue for a wholesaler is the sale of merchandise. Under a perpetual inventory system accounting records continuously disclose the amount of inventory. Operating expenses - cost of goods sold = gross profit. The primary difference between a periodic and perpetual inventory system is that a periodic system determines the inventory on hand only at the end of the accounting period. Inventory becomes part of cost of goods sold when a company sells the inventory. The periodic inventory system is used most commonly by companies that sell low-priced, high- volume merchandise.