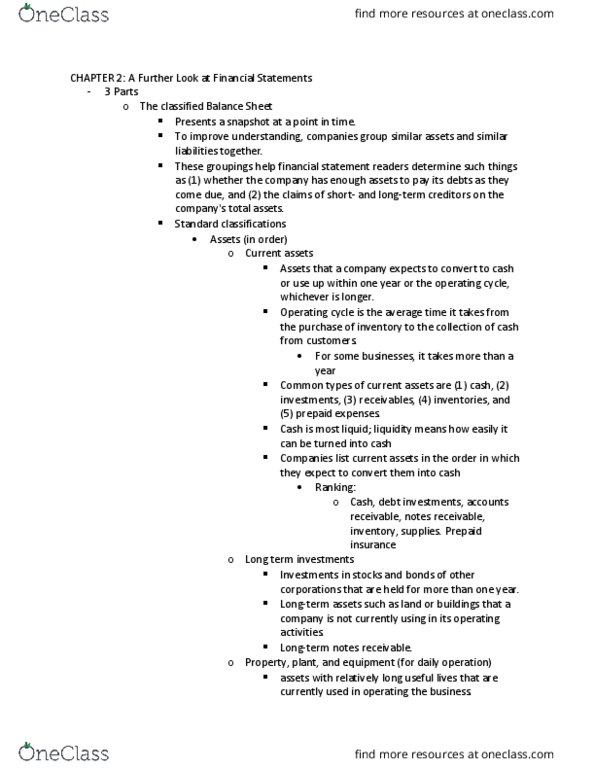

ACC 210 Lecture Notes - Lecture 2: International Accounting Standards Board, Accounting, Public Company Accounting Oversight Board

Document Summary

Get access

Related Documents

Related Questions

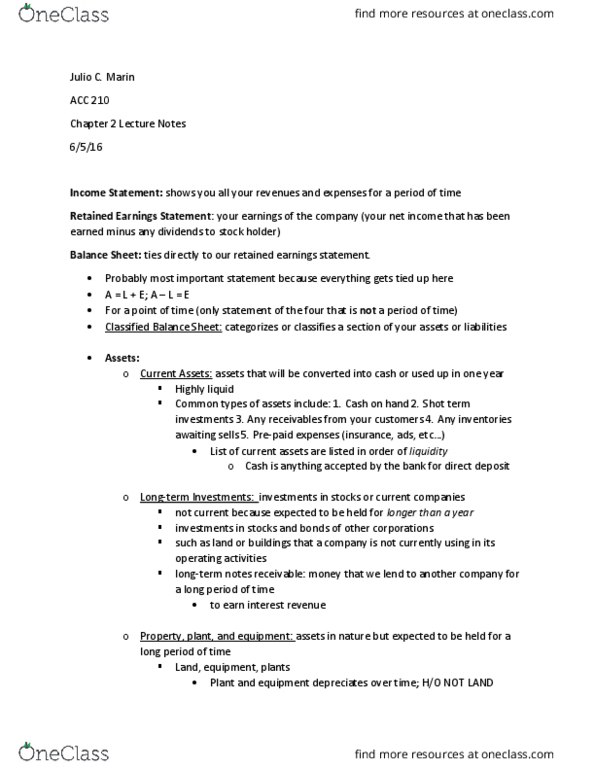

| Balance Sheet | 2015 | 2016 | 2017 | |||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| Assets | ||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| Cash | 807,000 | 628,000 | 612,000 | |||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| Accounts Receivables | 2,582,000 | 2,896,000 | 4,605,000 | |||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| Inventories | 2,870,000 | 5,181,000 | 7,319,000 | |||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| Total Current Assets | 6,259,000 | 8,705,000 | 12,536,000 | |||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| Net Fixed Assets | 2,216,000 | 2,423,000 | 5,538,000 | |||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| Total Assets | 8,475,000 | 11,128,000 | 15,074,000 | |||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| Liabilities and Equity | ||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| Accounts Payable | 961,000 | 1,648,000 | 3,137,000 | |||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| Notes Payable | 400,000 | 800,000 | 2,860,000 | |||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| Accruals | 440,000 | 800,000 | 1,150,000 | |||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| Total Current Liabilities | 1,801,000 | 3,248,000 | 7,147,000 | |||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| Long Term Debt | 1,350,000 | 1,908,000 | 1,867,000 | |||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| Common Stock | 3,650,000 | 3,650,000 | 3,650,000 | |||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| Retained Earnings | 1,674,000 | 2,322,000 | 2,410,000 | |||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| Total Equity | 5,324,000 | 5,972,000 | 6,060,000 | |||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| Total Liabilities and Equity | 8,475,000 | 11,128,000 | 15,074,000 | |||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| Income Statement | 2015 | 2016 | 2017 | |||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| Sales | 26,820,000 | 28,966,000 | 30,703,000 | |||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| Cost of Sales | 21,216,000 | 23,550,000 | 26,140,000 | |||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| Gross Profit | 5,604,000 | 5,416,000 | 4,563,000 | |||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| Operating Expenses | 2,574,000 | 3,225,000 | 3,866,000 | |||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| Operating Profit | 3,030,000 | 2,191,000 | 697,000 | |||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| Interest | 91,000 | 275,000 | 469,000 | |||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| Earnings Before Taxes | 2,939,000 | 1,916,000 | 228,000 | |||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| Taxes (48%) | 1,411,000 | 919,000 | 110,000 | |||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| Net Income | 1,528,000 | 997,000 | 118,000 | |||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| ||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

ABC Company, a toy manufacturer, believes the coming holiday season (between Thanksgiving in late November and Christmas on the 25thof December) will be a very good one, expecting an increase of 20% in its sales. Outside economic analysts believe the effects of the recent recession are over. Consumer confidence is high. To meet that 20% increase, however, inventories must be built up so, to finance that expansion, ABC wants to borrow $1,000,000 from its bank.

You are the loan officer who must make the decision as to whether or not to give ABC the money. You are going to prepare ratios for 3 years, the Cash Conversion Cycle for the same period and operating cash flow for the years for which you have figures.

Review the Balance Sheets and Income Statements for ABC over the 3 years and answer the following questions (20 points each).

3) Operating Cash Flow is the first of the 3 parts to the Statement of Cash Flows.

a) Define operating cash flow. What does it tell us?

b) Calculate ABCâs operating cash flows for those years for which figures are available.

c) Does your analysis of ABCâs operating cash flows change your conclusions listed in 1) and 2) above?

4) Do you believe ABCâs cash position and its management of cash needs improvement? If so, how would you recommend they do it?

Answer Questions in Bold!