ACCT 2301 Lecture 13: Notes Chapter 13

6 Nov 2018

Department

Course

Professor

Document Summary

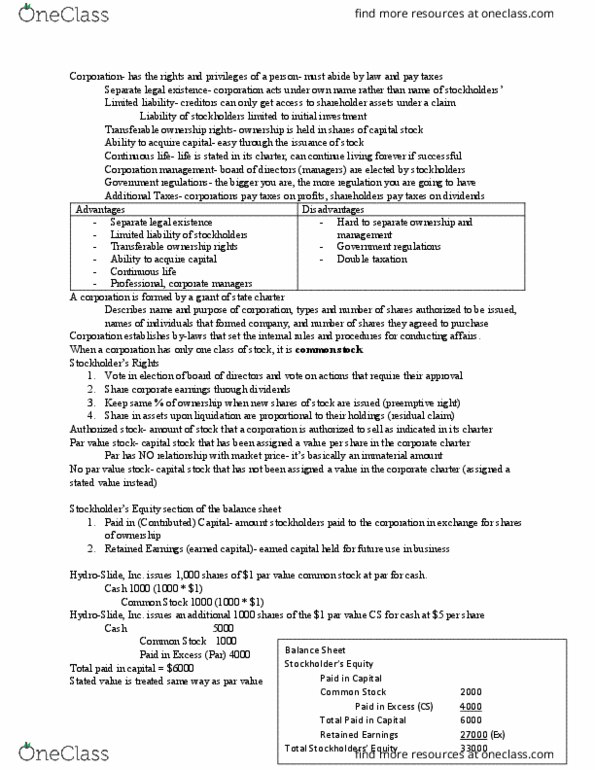

Separate legal entity: a corporation is a separate legal entity. Authorized stock: total number of shares that can be issued. Issued stock: stock that has been issued at some point in time. Treasurer stock: stock that has been issued and then repurchased by the corporation. Common stock: represents basic ownership of the corporation. Preferred stock: receive dividends before common stockholders and the share of investment before common stockholders (but don t have right to vote) Par value: minimum value that stock can be issued for (arbitrary amount. No-par: stock that has no amount (par) assigned to it. Stated value stock: no-par stock that has been assigned an amount similar to par value. Paid in capital: stockholder investment (common stock, preferred stock, paid in capital excess of par) Retained earnings: accumulated profit and losses, less dividends, over the life of the corporation. Stock issued in exchange for asset other than cash: