ACTG 2200 Lecture 5: Week 5 & 6 Notes

4 Feb 2017

School

Department

Course

Professor

Document Summary

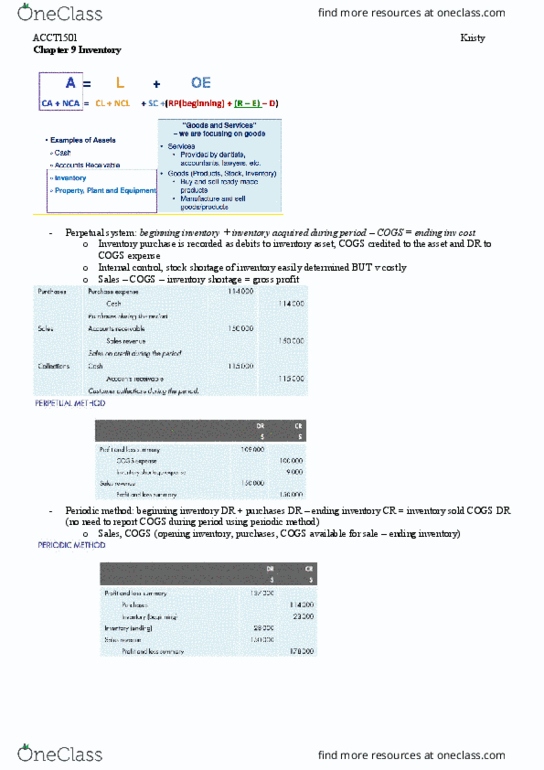

Manufacturing (building products: raw material, work in progress (labor, finished goods (overhead) Beginning inventory + purchases = cost of goods available for sale. Cost flow assumptions: fifo, whatever the price of first product, that is value of cogs, lifo, weighted average. If held onto inventory too long, it will lose value. Ar turnover = sales on acct / avg. accts receivable. Sales rev cogs = gross profit. Gross profit operating expenses = net income. Tangible: land, buildings, equipment, natural resources. Pay million for land, building, and equipment: land = ,000. 2/12 of million: building = ,000. Definite lives: patent 20 years, copyright creator"s life + 70 years, franchises. Definite lives: buildings, equipment, natural resources. Systematic & rationale allocation of cost of asset. Allocation of its life as an expense. Take part of total cost and put it into depreciation. Original cost current balance in acc.