ACC 311 Lecture Notes - Lecture 6: Income Statement, Equity Method, Income Tax

14 Feb 2018

School

Department

Course

Professor

Document Summary

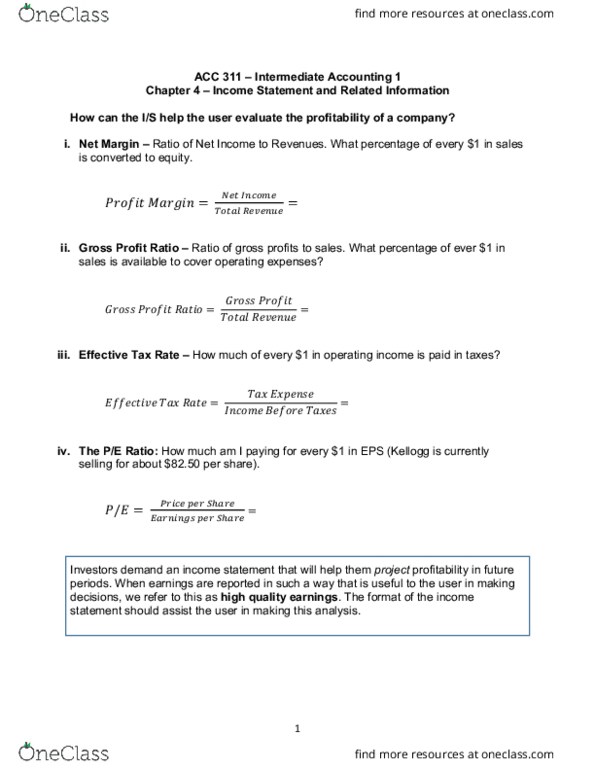

The income statement provides investors and creditors with information that helps them predict the amounts, timing, and uncertainty of future cash flows. Usefulness of the income statement: evaluate the past performance of the company, provide a basis for predicting future performance, help assess the risk or uncertainty of achieving future cash flows. Limitations of the income statement: companies omit items from the income statement that they cannot measure reliably, income numbers are affected by the accounting methods employed, income measurement involves judgment. Income statement sections: operating section, sales or revenue, cogs, selling expenses, administrative or general expenses, nonoperating section, other revenues and gains, other expenses and losses, income tax, discontinued operations, noncontrolling interest, earnings per share. Single step has only 2 groupings: revenues and expenses: primary advantage: simple presentation and absence of any implication that one type of revenue or expense item has priority over another.