ACC 311 Lecture Notes - Lecture 14: Historical Cost, Write-Off, Markdown

31 Mar 2018

School

Department

Course

Professor

Document Summary

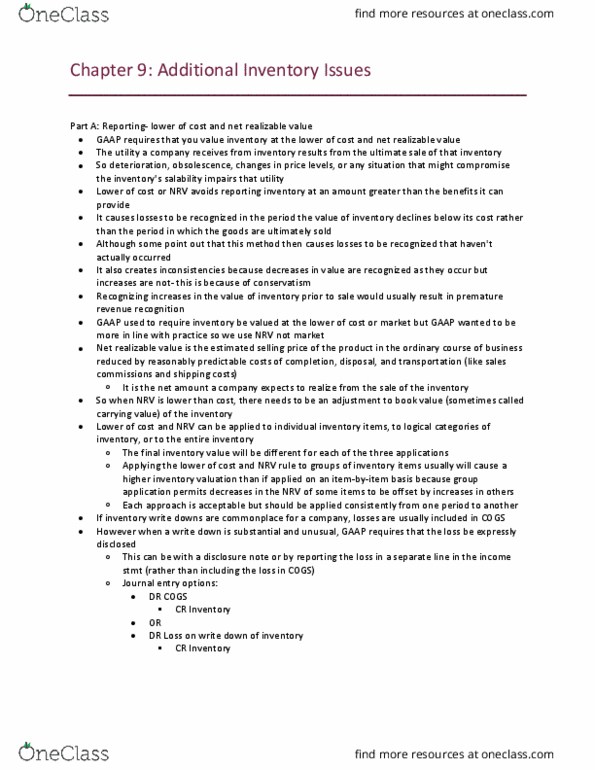

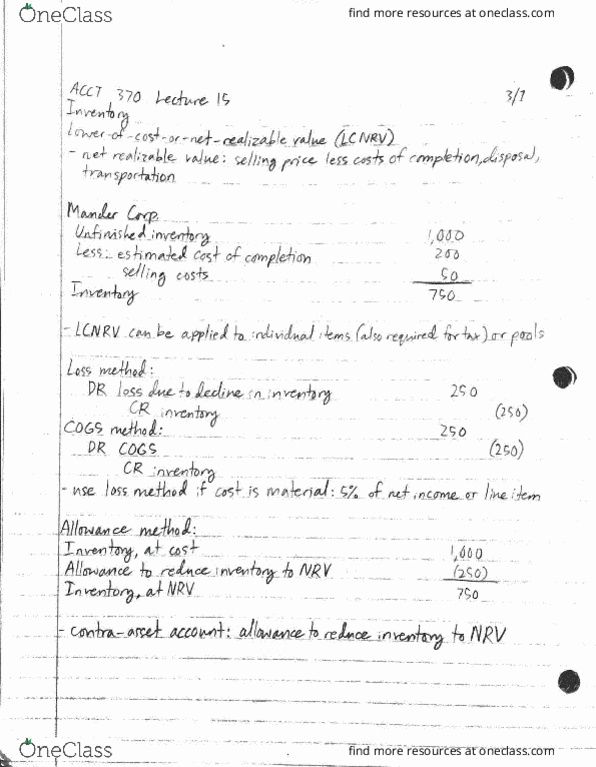

Companies abandon the historical cost principle when future utility of asset drops below its original cost. Net amount a company expects to realize from the sale of inventory. Estimated selling price in ordinary course of business less reasonably predictable costs of completion, disposal and transportation. Report inventory on balance sheet as nrv. Debit cogs for write-down of inventory to nrv. Debit loss due to decline of inventory to nrv. Can also use allowance account credit that instead of inventory. Close that account when company sells all those goods and open. Exception to nrv method for those companies using lifo or retail inventory methods. Instead of comparing cost to nrv, created a designated market value. Sales value - cost of completion = nrv - allowance for normal profit margin (% of sales) = nrv less normal profit margin. Lower limit: nrv less a normal profit margin. Prevents over or understating inventory with these floor and ceiling limits.