ECON 20A Lecture 17: Firm Under Perfect Competition

Document Summary

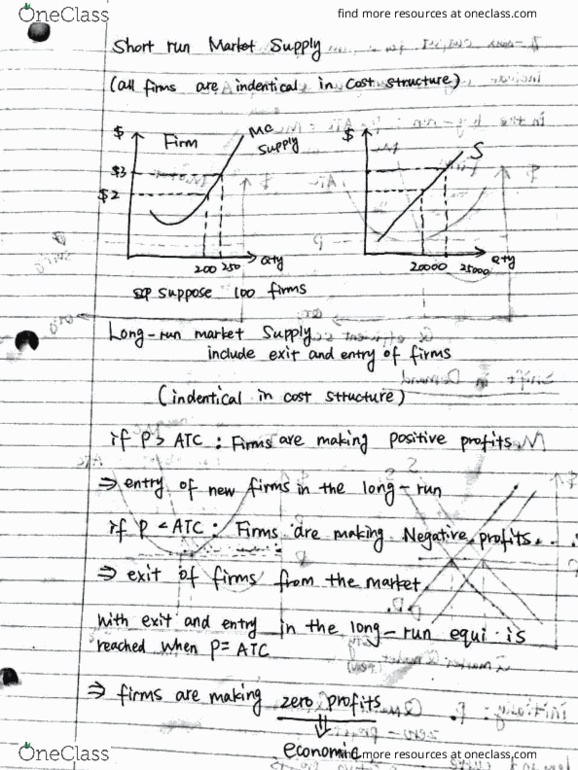

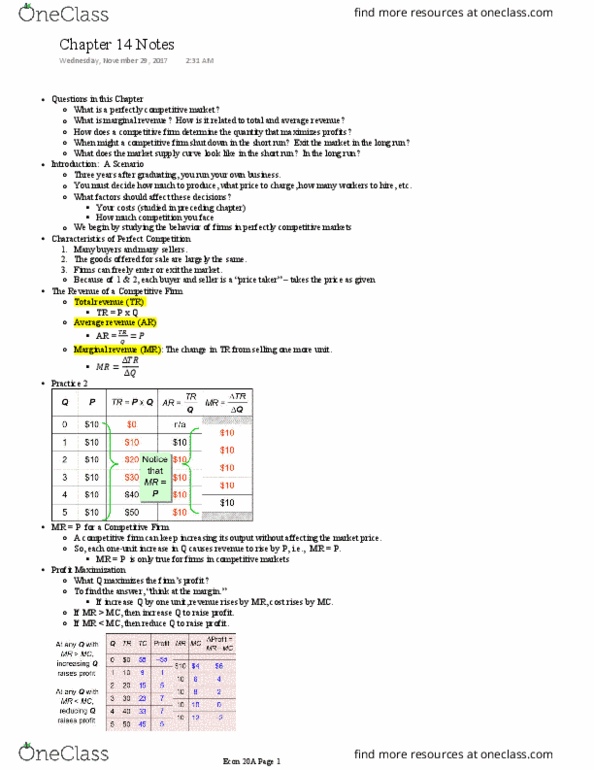

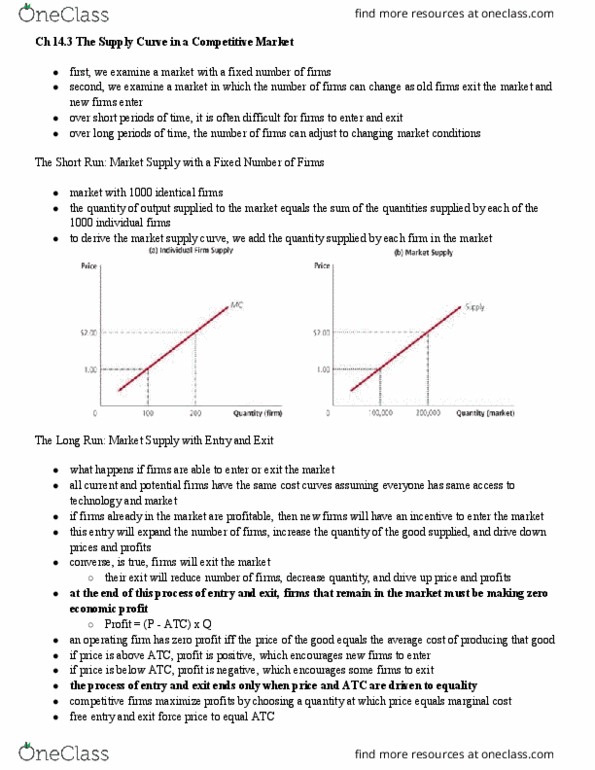

A = tr - tc: long term supply curve (mc above atc, short term supply curve (mc above avc) Market supply under perfect competition short run. Long run market supply with entry and exit. Long run equilibrium for firms in a perfectly competitive market. So, in the competitive eq"m: p = mc. Recall, mc is cost of producing the marginal unit. P is value to buyers of the marginal unit. So, the competitive eq"m is efficient, maximizes total surplus. For a firm in a perfectly competitive market, price = marginal revenue = average revenue. If p > avc, a firm maximizes profit by producing the quantity where mr = mc. Avc, a firm will shut down in the short run. If p < atc, a firm will exit in the long run. In the short run, entry is not possible, and an increase in demand increases firms" profits.