ECON 1 Lecture Notes - Lecture 9: Laissez-Faire, Economic Surplus, Demand Curve

5/3/18

Chapter 7: Consumers, Producers, and the Efficiency of Markets

- Allocation of resources refers to:

o How much of each good is produced

o Which producers produce it

o Which consumers consume it

- Welfare economics: studies how the allocation of resources affects economic well-being

- Willingness to pay: the maximum amount a buyer is willing to pay for that good

o Measures how much the buyer values the good

o Ex: If the price of an iPod is $200, the only buyers who will buy the iPod are those who have a

higher WTP than the market price of the iPod ($200)

▪ QD is the amount of those willing to buy the product

o You can create a demand curve by finding out the QD for each price (P) and then graphing it

▪ The less buyers there are, the more the D curve will look like a staircase

▪ The more buyers there are, the smaller the steps are → make it a smooth curve

▪ At any Q, the height of the demand curve is the WTP of the marginal buyers

• Marginal buyer: buyer who would leave the market if P were any higher

- Consumer surplus: the amount a buyer is willing to minus the amount the buyer actually pays

o CS = WTP – P

o Oly get to ejoy osuer surplus if you’re illig to pay aoe the arket prie alue

o In the demand curve, the total CS equals the area under the demand curve above the price,

from 0 to Q

o Higher price reduces CS:

▪ Fall in CS due to buyers leaving the market

▪ Fall in CS due to remaining buyers paying higher P

- Cost: the value of everything a seller must give up to produce a good (opportunity cost)

o Includes cost of all resources used to produe a good, iludig the alue of the seller’s tie

o A seller will produce and sell the good/service only if the price exceeds his/her cost

o Cost is a measure of willingness to sell

o At each Q, the height of the S cruve is the cost of the marginal seller

▪ Marginal seller: the seller who would leave the market if the price were any lower

- Producer surplus: the aout a seller is paid for a good ius the seller’s ost

o PS = P – cost

o Total PS equals the area above the supply curve under the price, from 0 to Q

o Lower price reduces PS:

▪ Fall in PS due to sellers leaving market

▪ Fall in PS due to remaining sellers getting lower P

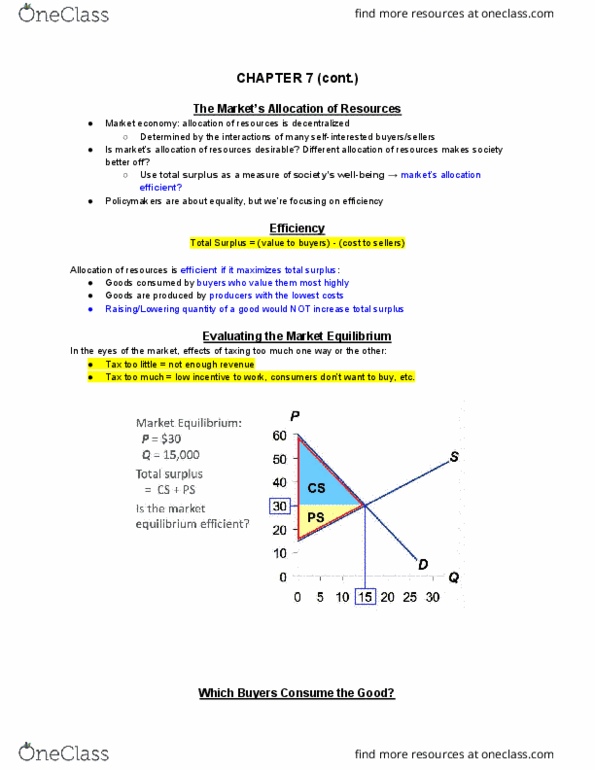

- Total surplus = CS + PS

o = total gains from trade in a market

o = (value to buyers) – (cost to sellers)

- Efficiency

o Total surplus = (value to buyers) – (cost to sellers)

o An allocation of resources is efficient if it maximizes total surplus, meaning:

▪ The goods are consumed by the buyers who value them most highly

▪ The goods are produced by the producers with the lowest costs

▪ Raising/lowering the quantity of a good would not increase total surplus

- Evaluating the market equilibrium

o The buyers who value the good most highly are the ones who consume it

o The sellers with the lowest cost produce the good

find more resources at oneclass.com

find more resources at oneclass.com

Document Summary

Chapter 7: consumers, producers, and the efficiency of markets. Allocation of resources refers to: how much of each good is produced, which producers produce it, which consumers consume it. Welfare economics: studies how the allocation of resources affects economic well-being. Consumer surplus: the amount a buyer is willing to minus the amount the buyer actually pays: cs = wtp p, o(cid:374)ly get to e(cid:374)joy (cid:272)o(cid:374)su(cid:373)er surplus if you"re (cid:449)illi(cid:374)g to pay a(cid:271)o(cid:448)e the (cid:373)arket pri(cid:272)e (cid:448)alue. Cost: the value of everything a seller must give up to produce a good (opportunity cost) Total surplus = cs + ps: = total gains from trade in a market, = (value to buyers) (cost to sellers) Evaluating the market equilibrium: the buyers who value the good most highly are the ones who consume it, the sellers with the lowest cost produce the good.