ECON 3A Lecture Notes - Lecture 13: Accrual, Balance Sheet, Net Income

Document Summary

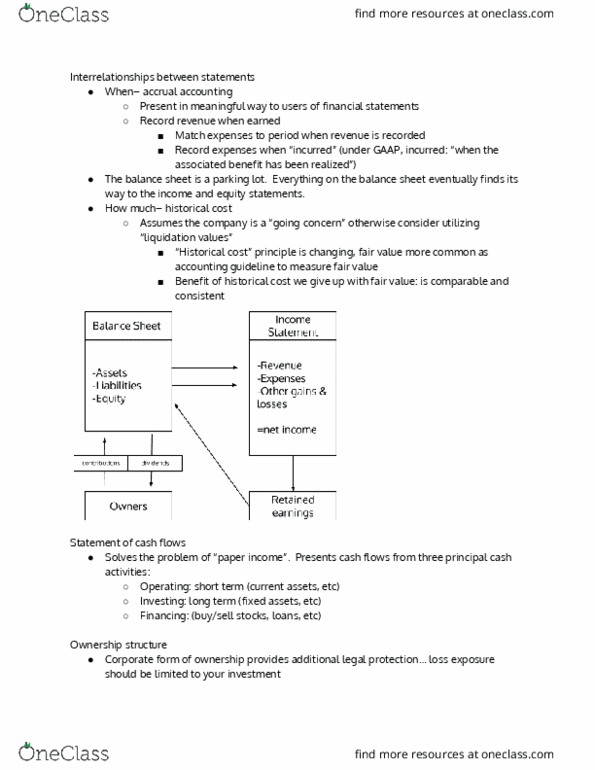

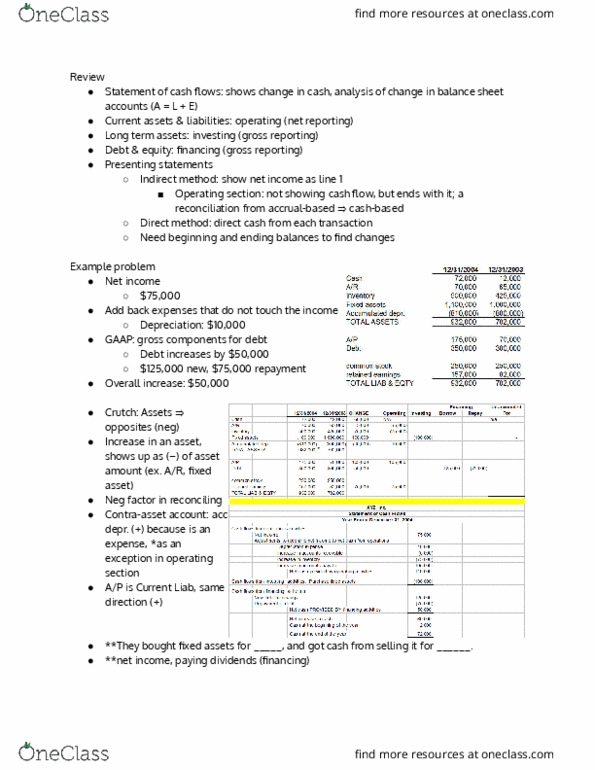

Statement of cash flows, users of the financial statements both. Bridges the gap created by paper income resulting from applying an accrual basis of accounting. Reconciles gaap income to operating cash flows and separately displays cash from investing and financing activities. Operating is like an income statement for cash. Is losing money after 2005 operating cash flows dips below zero. Indirect method reconciles income vs. operating cash flows. Analysis of change in all other balance sheet accounts combined. Reconcile change in each of balance sheet accounts, statement of cash flows. Principally affects current accounts on balance sheet (ar/ap, inventory, cash) Typical presentation called indirect because it reconciles the net income (accrual) to cash from operations. Think of it as net income, adjusted for non-cash activities, including changes in current assets. Gross basis: show in full what flows in and out. Reconciles net income to cash flows from operations by: