ACCT207 Lecture Notes - Lecture 7: Jordache, Accounts Receivable, Current Asset

17 Oct 2018

School

Department

Course

Professor

Document Summary

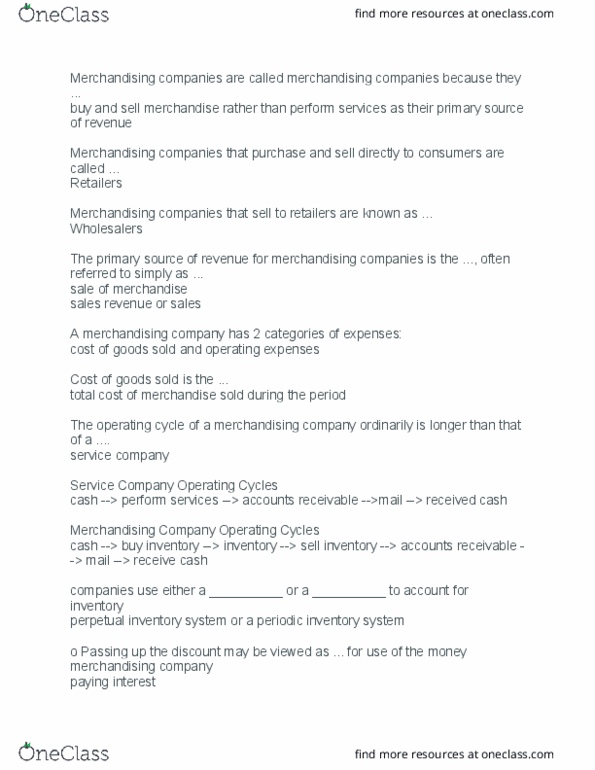

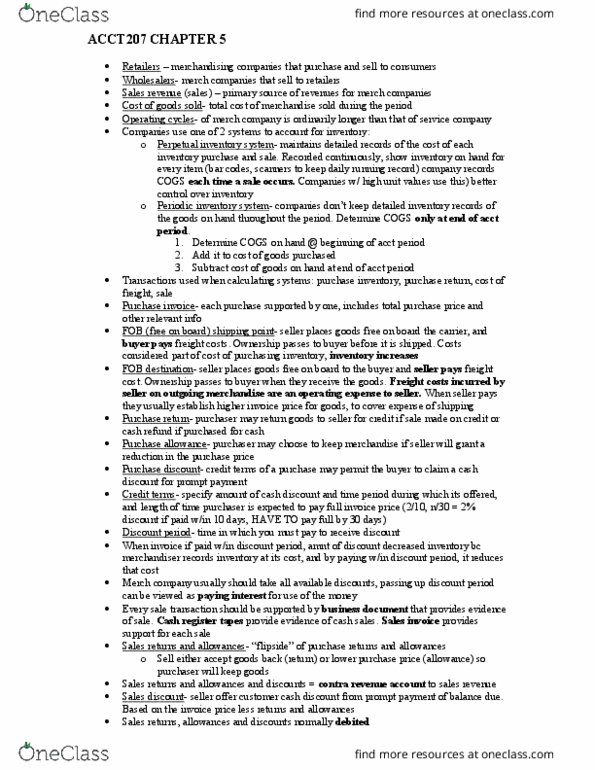

Amounts due from individuals/companies that are expected to be collected in cash. Accounts: amounts customers owe on account that result from a sale. Notes: written promise (formal instrument) for amount to be received. Other: interest, loans, advances, income taxes refundable, etc. Service organization records receivable after service performed on account. Merchandiser records receivable at the point of sale on account. Seller may offer discount to encourage early payment. Buyer might return goods found to be unacceptable. Example: jordache co. sells merchandise on account to polo company for. Polo returns merchandise worth to jordache co. Describe how companies value accounts receivable and record their disposition. Sales on account raise the possibility of accounts not being collected. Seller records loss that result from extending credit as bad debt expense. No matching, receivable not stated at net realizable value, not acceptable for financial reporting. Better matching, receivable stated at net realizable value, required by gaap.