FINC314 Lecture Notes - Lecture 12: Stock Fund, Market Risk, Weighted Arithmetic Mean

26 Jan 2017

School

Department

Course

Professor

Document Summary

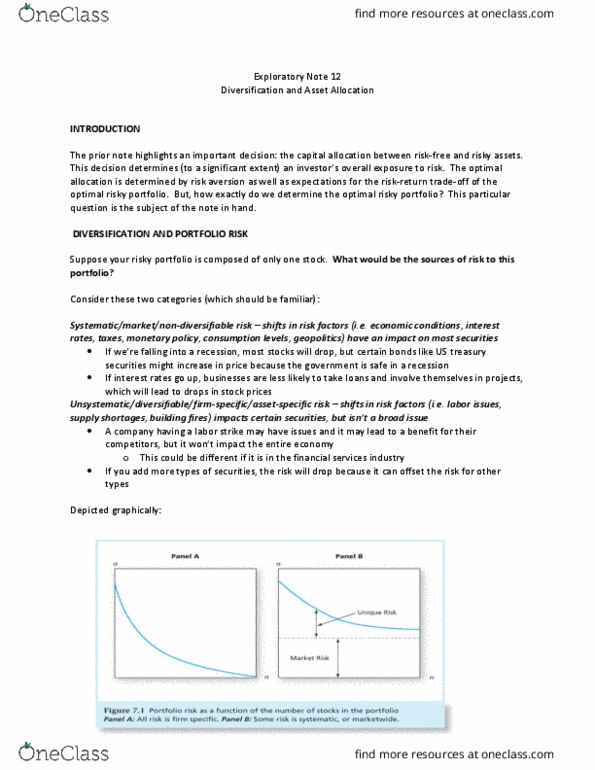

The prior note highlights an important decision: the capital allocation between risk-free and risky assets. This decisio(cid:374) deter(cid:373)i(cid:374)es (cid:894)to a sig(cid:374)ifica(cid:374)t exte(cid:374)t(cid:895) a(cid:374) i(cid:374)vestor"s overall exposure to risk. The optimal allocation is determined by risk aversion as well as expectations for the risk-return trade-off of the optimal risky portfolio. This particular question is the subject of the note in hand. Suppose your risky portfolio is composed of only one stock. Consider these two categories (which should be familiar): Systematic risk (market risk, non-diversified risk) example (recession) Changes in gdp will have an effect if they are substancial, but securities will be effected. Stocks will probably go down and gold will probably move up, (cid:271)o(cid:374)ds (cid:449)ill pro(cid:271)a(cid:271)ly (cid:373)o(cid:448)e up. Tbills (cid:449)ill (cid:373)ost likely (cid:373)o(cid:448)e up a lot. It does(cid:374)"t affe(cid:272)t all assets i(cid:374) the same way but theyre all being effected. Also- changes in consumer behavior, interest rates, taxation.