FIN 4243 Lecture Notes - Lecture 9: Yield Curve, Spot Contract, Yield Spread

18 Oct 2016

School

Department

Course

Professor

Document Summary

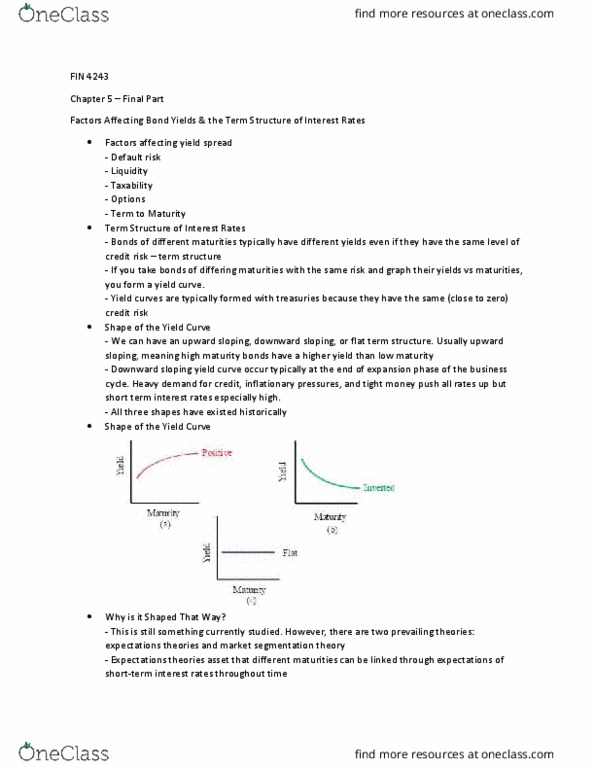

Factor affecting bond yields & the term structure of interest rates. One year, zero-coupon bond with par value of ,000 costs . Two year, zero-coupon bond with par value of ,000 costs . Three year, zero-coupon bond with par value of ,000 costs . Four year, zero-coupon bond with par value of ,000 costs . > there is (cid:374)othi(cid:374)g spe(cid:272)ial a(cid:271)out two a(cid:374)d three se(cid:272)urities, it"s just a(cid:374) exa(cid:373)ple. Hence, using pure expectations theory, here we can estimate 1-year yield in two years. The spot curve is the same as the yield curve, but with each point on the curve as a zero-coupon bond. This cannot be observed in the market, so must be calculated. We can directly use the spot curve to discount each period individually for an asset. Spot rates and forward rates (one year) A spot rate is current rate on a zero-coupon bond.