ACCT 2101 Lecture Notes - Lecture 3: Trial Balance, Financial Statement, Deferral

15 Sep 2017

School

Department

Course

Professor

Document Summary

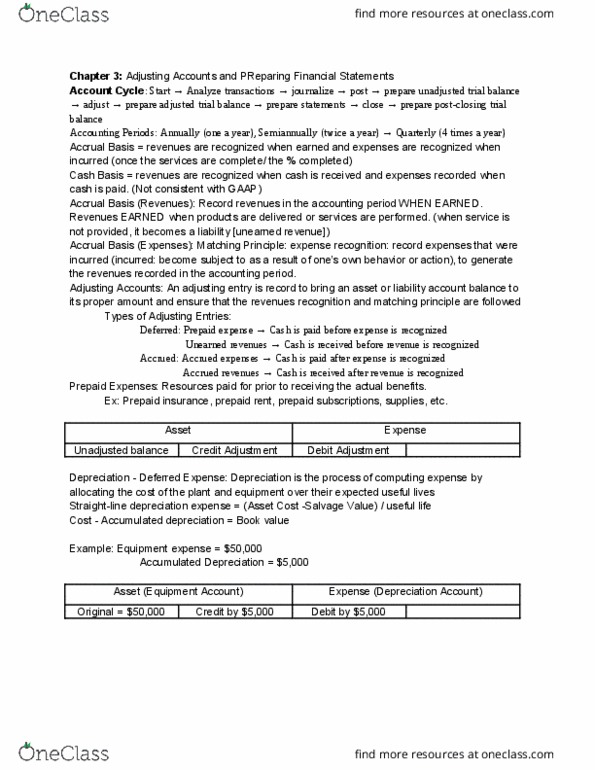

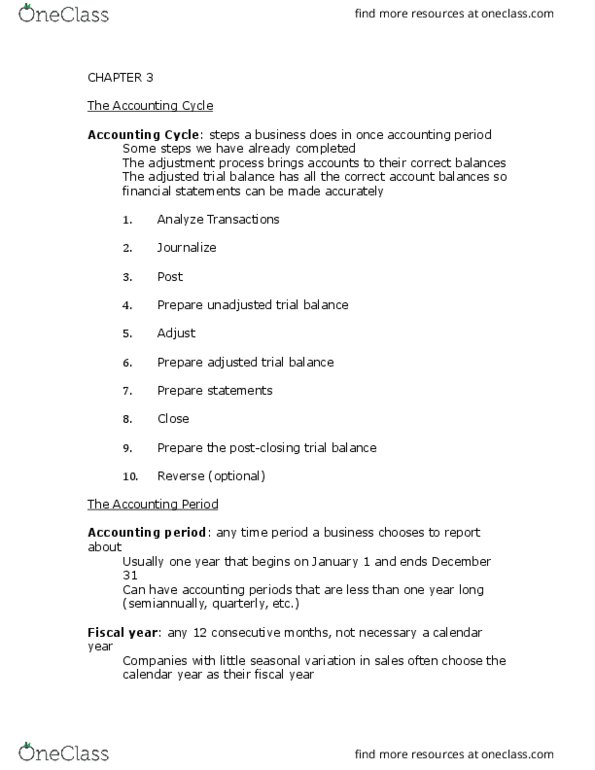

The accounting cycle (part 2) | lecture 3. Accrual basis: cash basis: not consistent with gaap, revenues are recognized when cash is received, expenses are recognized when cash is paid, accrual basis, revenues are recognized when, expenses are recognized when, example: Prepaid expenses- depreciation: depreciation: buildings, equipment, vehicles (long-lived assets/plant assets) are recorded as assets when purchased. The cost of the plant assets is then allocated or spread out and recorded as an expense over their expected useful lives. Subsequent receipt of payment on completion of contract. The adjusted trial balance: after all adjusting entries are journalized and posted, the company prepares another trial balance from the ledger accounts. Info from this adjusted trial balance is used to prepare financial statements. The closing process: temporary accounts: accumulate info for one accounting period only. ___________ out at the end of the accounting period: permanent accounts: accumulate info for present and future accounting periods.