AGED 260 Lecture Notes - Lecture 7: Cash Flow, Net Income, Financial Statement

15 Dec 2017

School

Department

Course

Professor

Document Summary

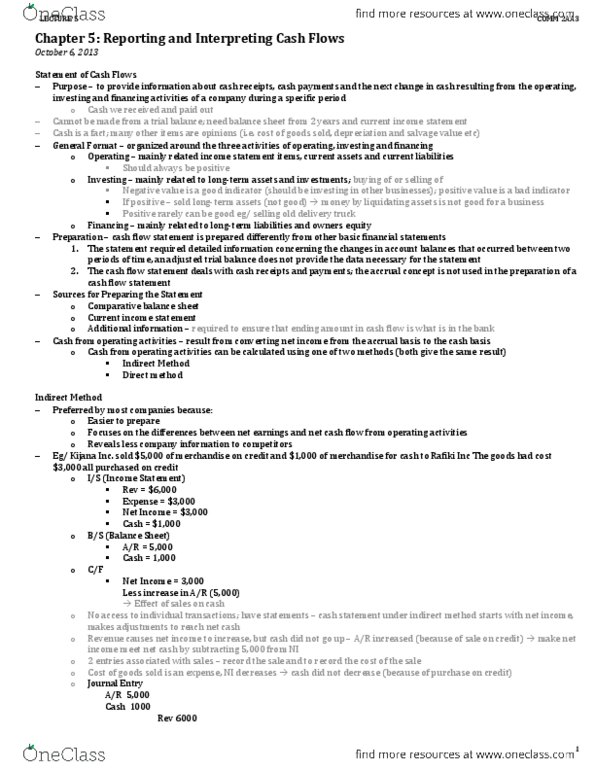

What are three sections of the statement t of cash flows: operating, investing, financial. Classify the following items: interest paid, interest received, dividend paid, dividend received. Direct method- cash effect of each operating activity is reported directly in the statement. Indirect method- net cash flow is derived indirectly by starting with reported net income and adding or subtracting items to convert that amount to a cash basis. Items that affected ni but have no cash effect: depreciation, amortization. Items that affected ni and cash but not from an operating activity: gains and loss in sale of property and equipment, operating items for which the income effect differs from the cash flow effect (current assets/ liabilities) Increases n current assets- negative adjustment to ni. Decreases in current assets-positive adjustment to ni. Decreases in current liabilities-negative adjustment to ni. Ni to cfo: decreases in current liabilities: debit interest expense.