AGED 260 Lecture Notes - Lecture 7: Income Tax, High High, Financial Statement

15 Dec 2017

School

Department

Course

Professor

Document Summary

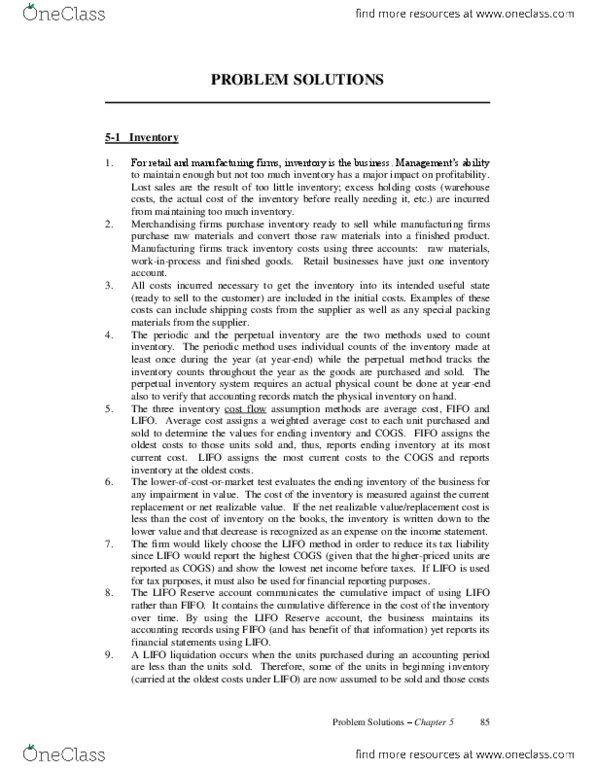

Comparative financial statements are recast to reflect the changes. Point of making change-to compare numbers across different period-comparitability. Adoption of a new fasb accounting standard. Switch between acceptable accounting principle under current gaap. Cost of goods available for sale: =bop inventory+new purchases, =eop inventory+cogs. Lifo conformity rule: irs requires that firms use lifo for tax reporting should also use lifo for financial reporting keep companies on track. If you save on taxes, you have to report that. Spencer company changed from lifo to fifo for both financial reporting and tax purposes in: assume a rising cost environment. The cumulative effect of change on inventory balance is 1,137 at the end of 2014. Debit- inventory 1137 (going from lifo to fifo going from low cogs to high cogs is low to high inventory. ?credit-retained earnings 910= (1-20)*1137 (have to make a prior period adjustment) Debit- deferred tax asset 227 (accounts for temporary differences)