AECN 201 Lecture Notes - Lecture 2: Mercantilism, Cash Cash, North American Free Trade Agreement

Document Summary

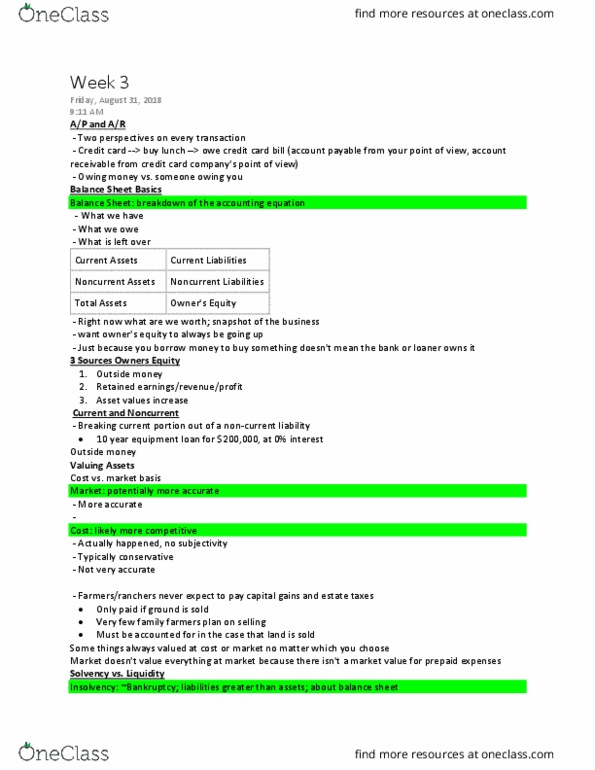

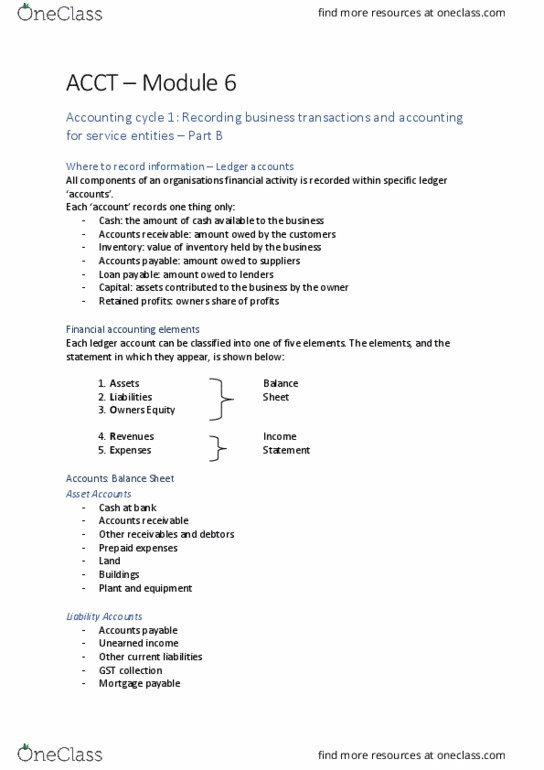

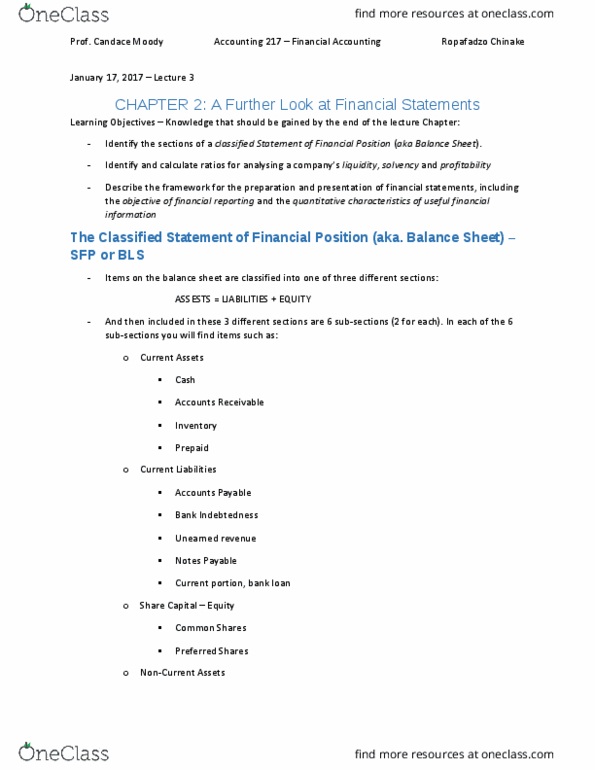

Where industry is going: competing with all other industries. Current: less than one year, something that will be turned into cash/used within one accounting period. Inventory: finished product to be sold: cash, a/r (accounts receivable): a loan extended to someone else, prepaid expenses, prepaid insurance. Non-current: things that will not be liquidated for greater than one year; something owned to produce something/make money; often economic capital. Revenue: cash or non-cash value of products produced and sold. Expenses: costs that happen because a product is being produced (cash/non-cash) Direct: can be tied directly to units produced. Indirect: can"t be tied directly to units produced. Accounting equation (assets - liabilities = owners equity) Statement of cash flows: looks at cash in and out and why the cash is moving in such a way. Cash in/out: timing of cash in and out. Steel industry at full capacity restricts choices for consumers. Can be difficult for everyone to agree on terms.