MRKT 325 Lecture Notes - Lecture 3: Spot Market, Futures Exchange, 2 On

Document Summary

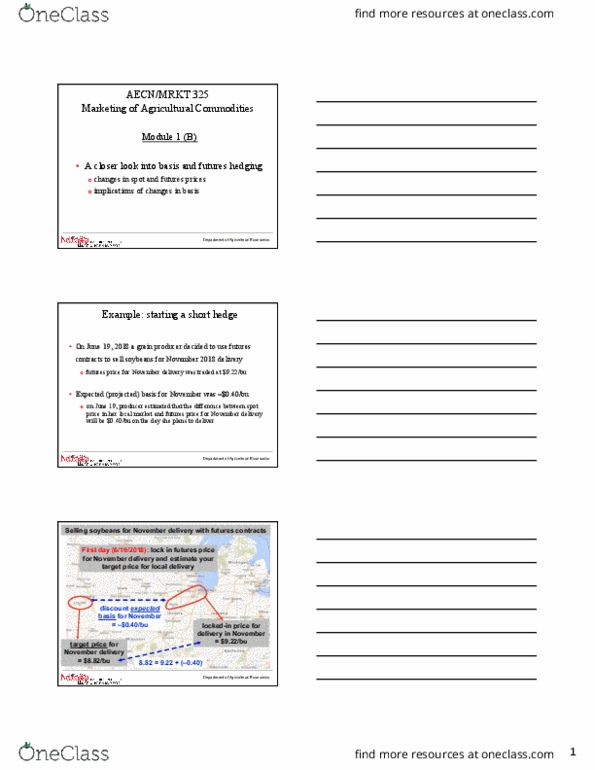

Module 1 (d: rolling hedges with futures contracts, switching delivery months during the hedge. Readings: marketing with futures contracts rolling hedges (handout, all previous readings for this module are useful in terms of using futures contracts in commodity marketing, but none of them talks specifically about rolling hedges (posted on canvas) Basic idea: example: now let"s fast-forward to september 20, 2017. The producer checks the futures prices and notices that they are trading at. . 50/bu for december 2017 delivery and . 62/bu for march 2018 delivery: she sees an opportunity to make extra money by waiting until. The cost of carry for this producer is sh. 03/bu/month. . 50/bu (out of december contract) sells at . 62/bu (enter march contract) 2017 nothing happens delivers in local spot market sells at. Short hedger gains when basis narrows (less negative: lose if expected basis in the more distant delivery month is wider than expected basis in current delivery month.