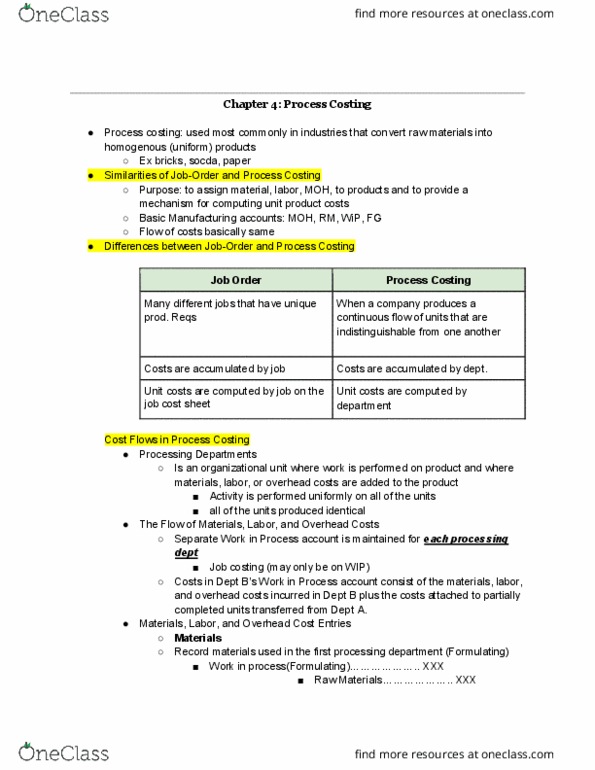

ACCT 226 Lecture Notes - Lecture 6: Finished Good

Document Summary

Get access

Related Documents

Related Questions

| Can anyone please help me do the ledger accounts for accounts receivable, accounts payable, sales revenue, raw materials,salaries and wages payable,cost of goods sold, work in process, salaries and wages expense, finished good, advertising expense, manufacturing overhead, depreciation expense, accumulated depreciation. General Journal | ||||||

| Date | Description | Debit | Credit | |||

| Dec 1 ,17 | Raw material | $ 10,000 | ||||

| Accounts payable | $ 10,000 | |||||

| 5-Dec | Work in progress | $ 1,600 | ||||

| raw material | $ 1,600 | |||||

| 10-Dec | Work in progress | $ 150 | ||||

| salaries and wages payable | $ 150 | |||||

| Manufacturing overhead | $ 2,000 | |||||

| salaries and wages payable | $ 2,000 | |||||

| Salaries and wages expense | $ 3,000 | |||||

| accounts payable | $ 3,000 | |||||

| 15-Dec | Work in progress | $ 1,900 | ||||

| raw material | $ 1,900 | |||||

| 16-Dec | manufacturing overhead | $ 500 | ||||

| account payable | $ 500 | |||||

| 17-Dec | Advertising expense | $ 1,200 | ||||

| accounts payable | $ 1,200 | |||||

| 20-Dec | Manufacturing overhead | $ 150 | ||||

| accuulated depreciation | $ 150 | |||||

| Depreciation expense | $ 600 | |||||

| accounts payable | $ 600 | |||||

| 22-Dec | Work in progress | $ 1,800 | ||||

| manufacturing overhead | $ 1,800 | |||||

| 26-Dec | finished goods | $ 3,520 | ||||

| work in progress | $ 3,520 | |||||

| 28-Dec | accounts receivable | $ 15,000 | ||||

| sales revenue | $ 15,000 | |||||

| cost of goods sold | $ 3,520 | |||||

| finished goods | $ 3,520 | |||||

| 31-Dec | work in progress | $ 60 | ||||

| salaries and wages payable | $ 60 | |||||

| work in progress | $ 900 | |||||

| manufacturing overhead | $ 900 | |||||

| cost of goods sold | $ 50 | |||||

| manufacturing overhead | $ 50 | |||||

Zachary Modems, Inc. acquired a subsidiary named Anywhere, Inc. (AI). AI manufactures a wireless modem that enables users to access the Internet through cell phones. The following trial balance was drawn from the accounts of the subsidiary:

| Cash | $ | 184,600 | ||||||

| Raw materials inventory | 3,680 | |||||||

| Work in process inventory | 5,530 | |||||||

| Finished goods inventory | 6,450 | |||||||

| Common stock | $ | 119,060 | ||||||

| Retained earnings | 81,200 | |||||||

| Totals | $ | 200,260 | $ | 200,260 | ||||

The subsidiary completed the following transactions during 2017:

1. Paid $55,380 cash for direct raw materials.

2. Transferred $46,160 of direct raw materials to work in process.

3. Paid production employees $73,860 cash.

4. Applied $48,910 of manufacturing overhead costs to work in process.

5. Completed work on products that cost $150,410.

6. Sold products that cost $131,950 for $167,950 cash. Record the recognition of revenue in a row labeled 6a and the cost of goods sold in a row labeled 6b.

7. Paid $18,450 cash for selling and administrative expenses.

8. Actual overhead costs paid in cash amounted to $50,710.

9. Closed the Manufacturing Overhead account. The amount of over- or underapplied overhead was insignificant (immaterial).

10. Made a $4,580 cash distribution to the owners

REQUIRED

A. Prepare a schedule of cost of goods manufactured and sold.

| |||||||||||||||||||||||||||||||||||||||

I need to Prepare entries for a job order, cost system, and cost of goods manufactured schedule, but my numbers aren't matching up. Please answer both parts of the question.

Case Inc. is a construction company specializing in custom patios. The patios are constructed of concrete, brick, fiberglass, and lumber, depending upon customer preference. On June 1, 2017, the general ledger for Case Inc. contains the following data.

| |||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||