ACCT 2301 Lecture Notes - Lecture 4: Net Income, Common Stock, Retained Earnings

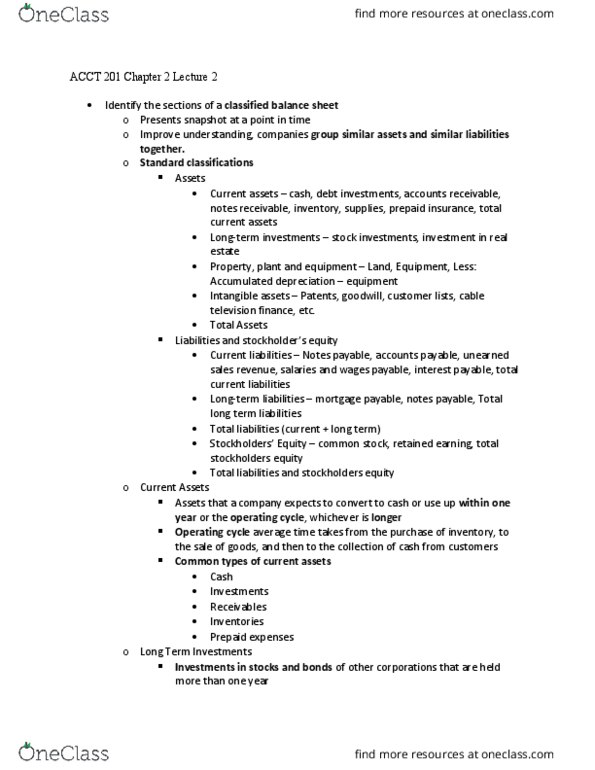

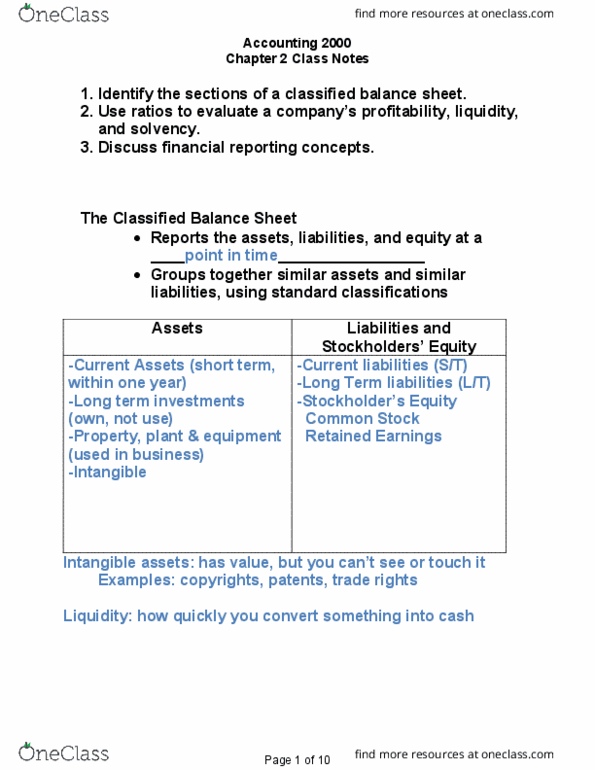

Classified balance sheet:

-Presents the main categories of the basic accounting equation; Assets, Liabilities and

Stockholder’s Equity.

-Common sub groupings:

1) Current assets:

-Cash and other assets that can be converted into cash or used up within the normal operating

cycle

-listed first on B/S

2) Long-term assets

3) Current liabilities

4) long-term liabilities

5) Stockholders’ equity

Current assets

-Cash and other assets that can be converted into cash or used up within the normal operating cycle, or

one year, whichever is longer.

-Listed first on the balance sheet in order of liquidity.

Long term assets:

Assets the company does not expect to convert into cash during the normal operating cycle, or one year,

whichever is longer.

Common types:

-Property, plant, and equipment

-Intangible assets

-Other long-term assets

Intangible assets:

Assets that lack a physical presence

Common examples:

¡Brand names

¡Copyrights

¡Patents

¡Trademarks

Current liabilities:

Liabilities that must be settled within the normal operating cycle, or one year, whichever is longer

Common examples:

¡Accounts payable

¡Accrued expenses payable

¡Short-term notes payable

¡Other current liabilities

Long term liabilities:

find more resources at oneclass.com

find more resources at oneclass.com

Document Summary

Presents the main categories of the basic accounting equation; assets, liabilities and. Cash and other assets that can be converted into cash or used up within the normal operating cycle. Listed first on b/s: long-term assets, current liabilities, long-term liabilities, stockholders" equity. Cash and other assets that can be converted into cash or used up within the normal operating cycle, or one year, whichever is longer. Listed first on the balance sheet in order of liquidity. Assets the company does not expect to convert into cash during the normal operating cycle, or one year, whichever is longer. Liabilities that must be settled within the normal operating cycle, or one year, whichever is longer. Debt obligations not due to be settled within the normal operating cycle, or one year, whichever is less. The residual ownership interest in the assets of a business after its liabilities have been paid off.