MGT 200 Lecture Notes - Lecture 7: Risk-Free Interest Rate, Interest Rate Risk, Current Yield

Document Summary

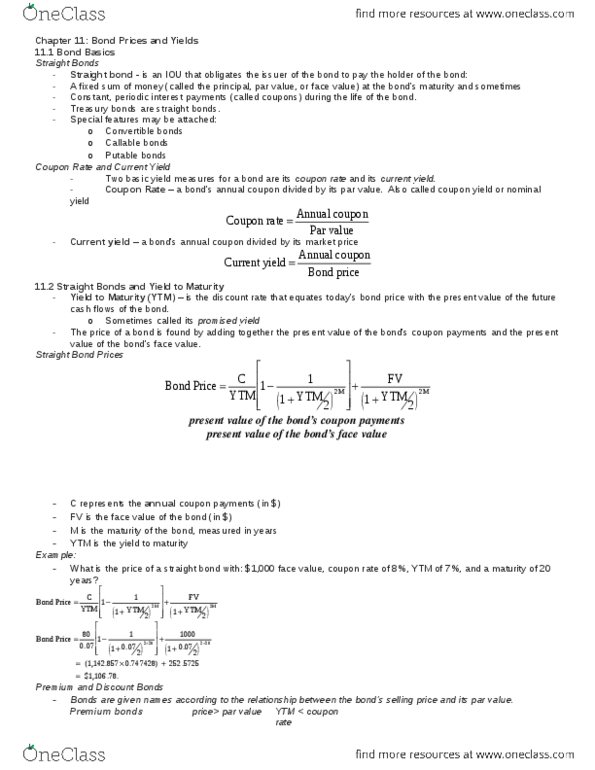

Debt security claim on a specified periodic stream of income. Bond- security issued in connection with a borrowing arrangement. Borrower issues/sells a bond to the lender for some cash. Issuer must make payments to the bondholder semiannual coupon payments. Issuer repays the debt by paying the bond"s par value/face value. Coupon rate determines the interest payment = coupon rate x par value. Treasury notes maturities between 1 and 10 years. Treasury bonds maturities between 10 and 30 years. Accrued interest = annual coupon payment / 2 x days since last coupon / days separating coupons. Call provisions on caorpoate bonds issuer can repurchase the bond at a specified call price before the maturity date pay for repurchase of existing higher coupon bonds to issue lower coupon bonds. Have higher coupons and yields because of the risk that they might be called bacl. Convertible bonds can exchange bond for a # of shares of common stock.