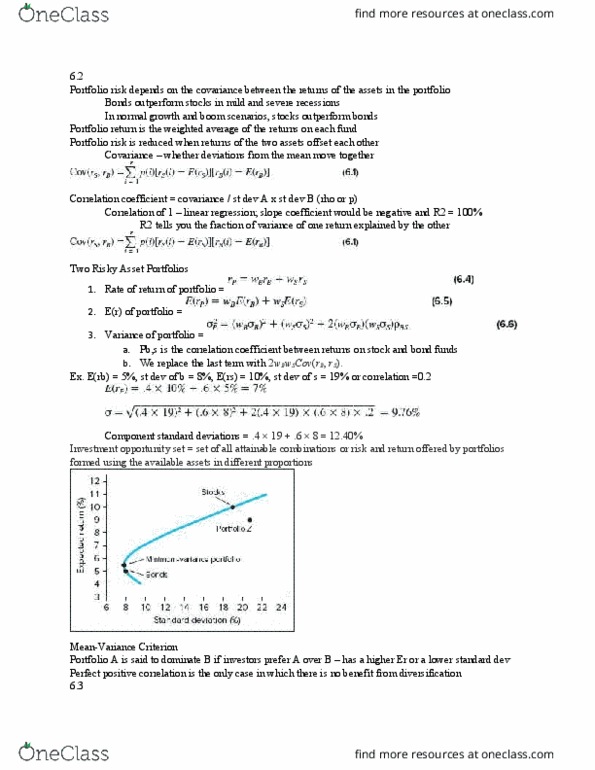

MGT 200 Lecture Notes - Lecture 3: Treynor Ratio, Efficient Frontier, Risk Premium

Document Summary

Shifting money to rf asset reduces the risk and the return of the portfolio. Risky asset increases the risk and return of the portfolio. When we don"t borrow, all assets lie on the same cal. Using 50% leverage, y = 1. 5 borrow at rf rate and invest everything in the risky asset. Rc = (1. 5 * . 15) + (-0. 5*. 07) = 19% Have cash and borrow to invest, so 420 / 300 = 1. 4. Rf rate = 7% and while the return on the risky asset is still 15% The cal line for investors is kinked because they cannot borrow at the rf rate. If you borrow the 50% leverage at 9% interest instead of 7% rf rate. Erc = 1. 5 * . 15 + (1-1. 5) * . 09 = 18% St dev = 1. 5 * . 22 = 33% The slope of the cal line decreases when borrow at a higher interest rate.