Verified Documents at University of Waterloo

- Introduction to Financial Accounting

- University of Waterloo

- Verified Notes

Browse the full collection of course materials, past exams, study guides and class notes for AFM101 - Introduction to Financial Accounting at University of Waterloo verified by …

PROFESSORS

All Professors

All semesters

Haihao Lu

fall

30Verified Documents for Haihao Lu

Class Notes

Taken by our most diligent verified note takers in class covering the entire semester.

AFM101 Lecture Notes - Lecture 1: Accounting Equation, Office Supplies, Accounts Receivable

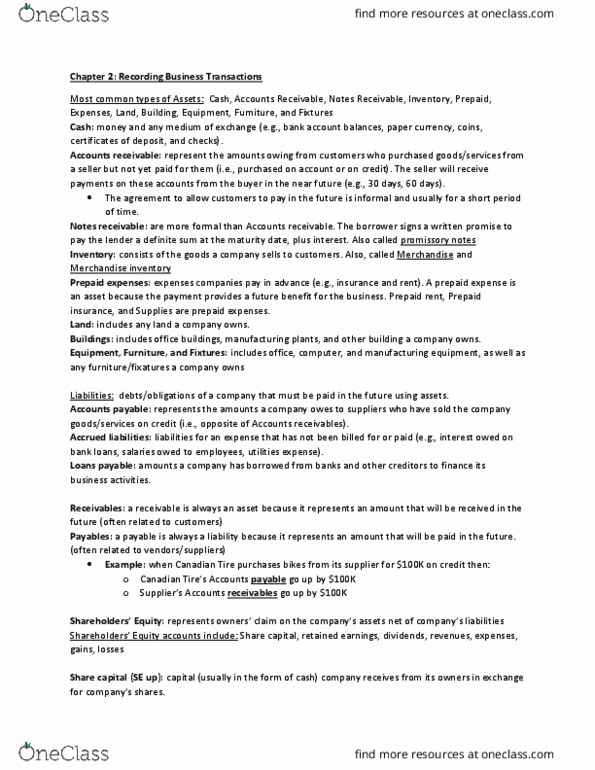

Most common types of assets: cash, accounts receivable, notes receivable, inventory, prepaid, Cash: money and any medium of exchange (e. g. , bank acco

624

AFM101 Lecture Notes - Lecture 1: Management Accounting, Cash Flow Statement, Retained Earnings

387

AFM101 Lecture Notes - Lecture 1: Management Accounting, Operating Cash Flow, Cash Flow

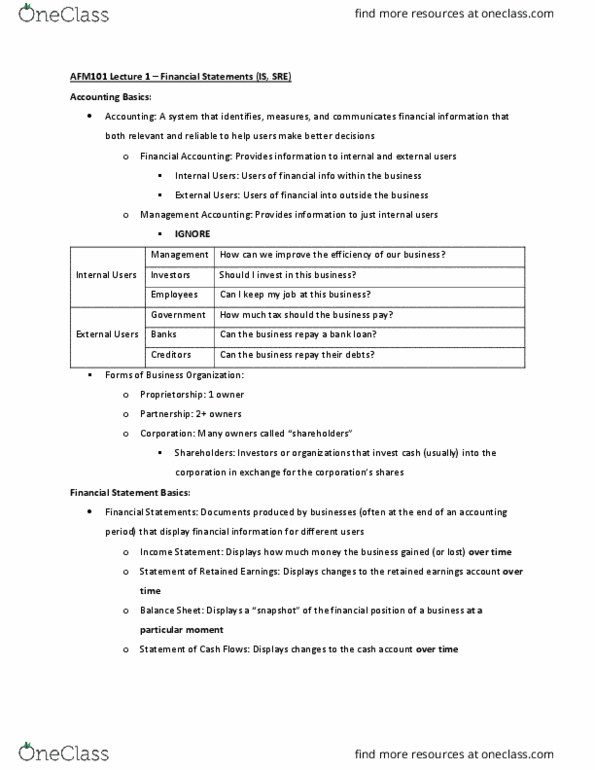

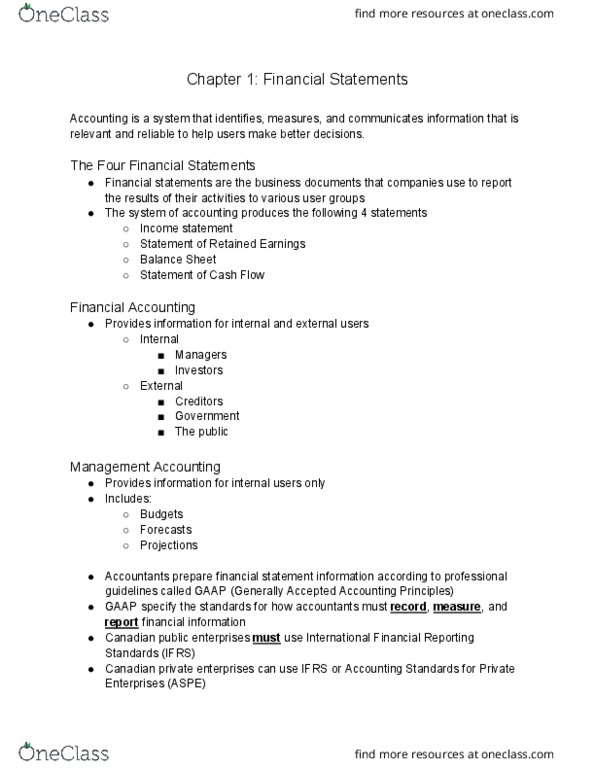

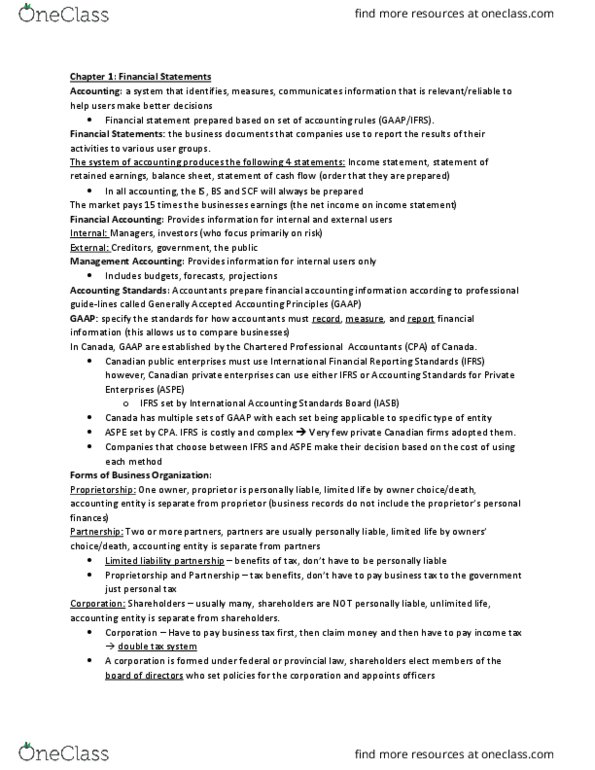

Accounting is a system that identifies, measures, and communicates information that is relevant and reliable to help users make better decisions. Finan

4189

AFM101 Lecture Notes - Lecture 1: Accrual, A Question Of Balance, Cash Cash

Accounting: a system that identifies, measures, communicates information that is relevant/reliable to help users make better decisions: financial state

928

AFM101 Lecture Notes - Lecture 2: Retained Earnings, A Question Of Balance, Share Capital

369

AFM101 Lecture Notes - Lecture 2: Cash Flow Statement, Retained Earnings, Share Capital

334

AFM101 Lecture Notes - Lecture 3: Deferral, Share Capital, Retained Earnings

356

AFM101 Lecture Notes - Lecture 3: Retained Earnings, Accounting Equation, Faithful Representation

The overall objective of accounting is to provide financial information about the reporting entity that is useful to existing and potential investors,

372

AFM101 Lecture Notes - Lecture 4: The Ledger, Retained Earnings, Share Capital

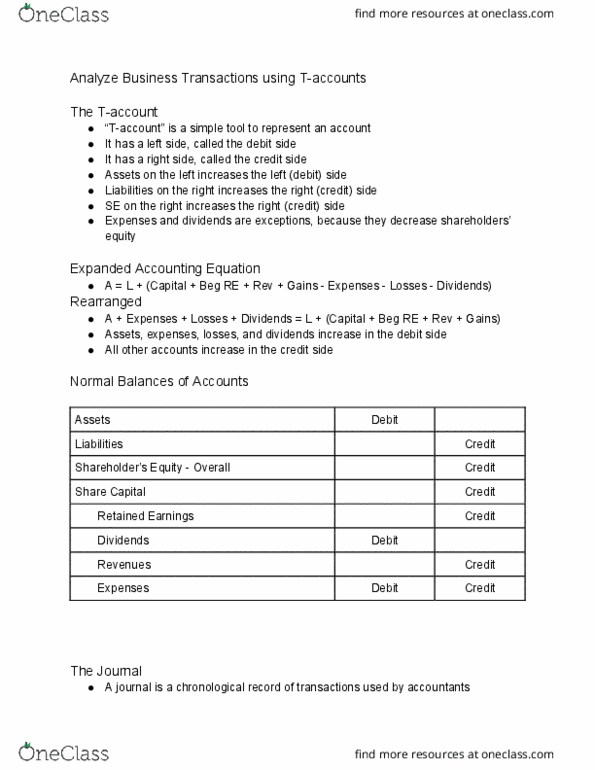

It has a left side, called the debit side. It has a right side, called the credit side. T-account is a simple tool to represent an account. Assets on t

253

AFM101 Lecture Notes - Lecture 4: Share Capital, Cash Cash, Retained Earnings

Unearned revenue: unearned revenue: used when a service is paid in advance. T-accounts: t-accounts: t-charts that represent their assigned account, acc

428

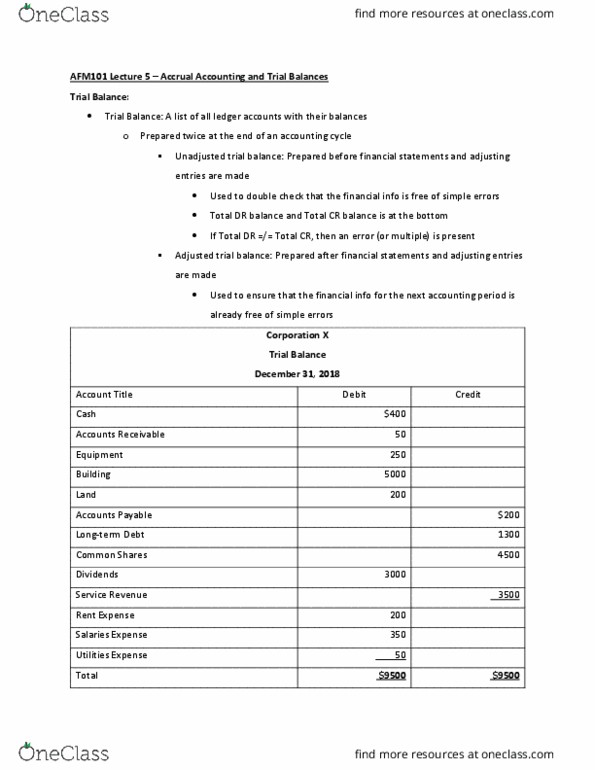

AFM101 Lecture Notes - Lecture 5: Trial Balance, Financial Statement, Accounting Information System

516

AFM101 Lecture Notes - Lecture 5: Costco, Revenue Recognition, Matching Principle

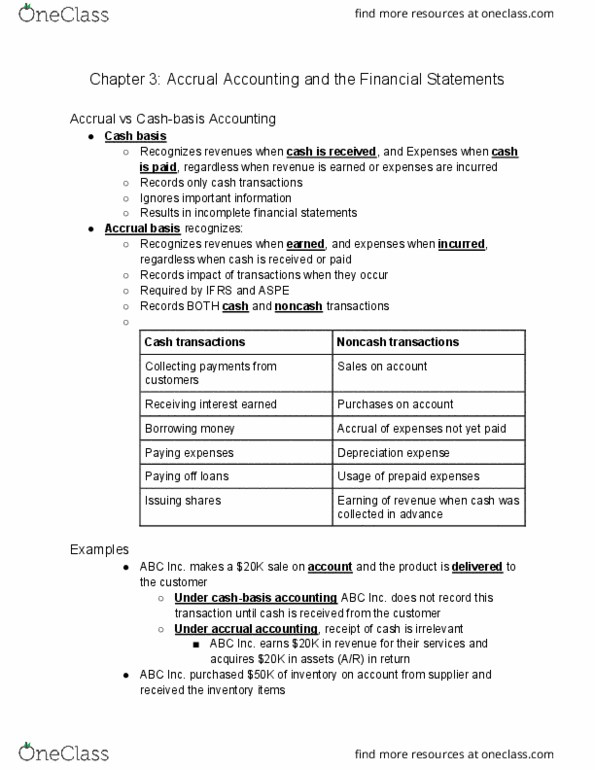

Chapter 3: accrual accounting and the financial statements. Recognizes revenues when cash is received, and expenses when cash is paid, regardless when

859

AFM101 Lecture Notes - Lecture 6: Operating Expense, Financial Statement, Fiscal Year

Afm101 lecture 6 end-of-year procedures and ratios. Depreciation: depreciation: an estimate of the lost in monetary value to a long-term asset over tim

451

AFM101 Lecture Notes - Lecture 6: Current Liability, Balance Sheet, Retained Earnings

The income statement is recorded first because it reports net income or net loss, which is needed to prepare the statement of retained earnings. The ba

389

AFM101 Lecture Notes - Lecture 7: Money Market Fund, Cash Cash, Cash Flow

On the statement of cash flows, the definition of cash includes: E. g. treasury bills, money market funds, etc. Cash equivalents are short-term, highly

3108

AFM101 Lecture Notes - Lecture 7: Cash Cash, Money Market Fund, Cash Flow

Afm101 lecture 7 cash flows statements and cash. Cash flow activities: operating activities: activities that directly contribute to the revenue of a bu

416

AFM101 Lecture Notes - Lecture 8: Free Cash Flow, Accrual, Cash Flow

296

AFM101 Lecture Notes - Lecture 9: Money Market Fund, Cash Cash, Bank Reconciliation

Companies usually combine all cash amounts into a single total balance sheet called cash & cash equivalents . Cash is the most liquid asset because

4120

AFM101 Lecture Notes - Lecture 11: Non-Sufficient Funds, Accounts Receivable, Bank Reconciliation

510

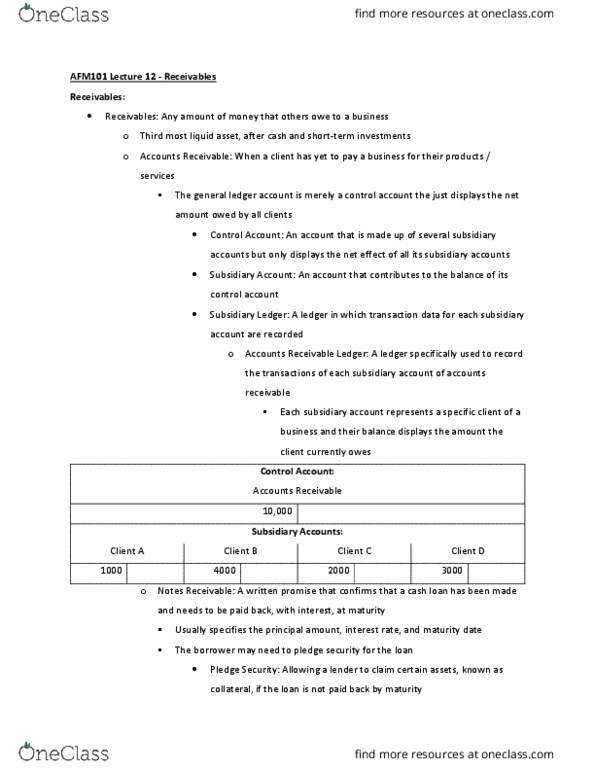

AFM101 Lecture Notes - Lecture 12: Operating Expense, Income Statement, Cash Flow

Companies rarely collect all of their a/r. So, companies must account for their uncollectible a/r (i. e. , bad debts) Customers that do not have cash a

574

AFM101 Lecture Notes - Lecture 12: General Ledger, Market Liquidity, Accounts Receivable

If we look at the t-account of afda (assume the total uncollectible amount is and the current afda balance is ): 70 = 100 - 30 the (cid:271)ad de(cid:

614

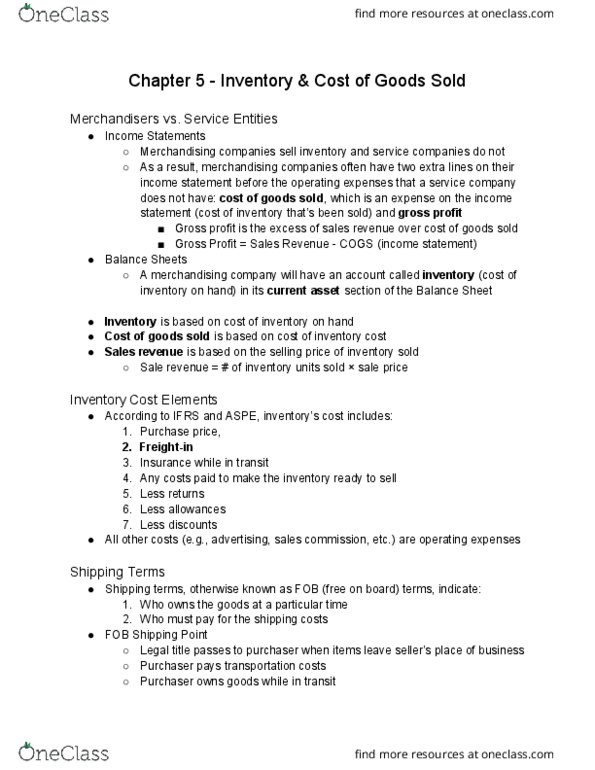

AFM101 Lecture Notes - Lecture 13: Gross Profit, Income Statement, Current Asset

Chapter 5 - inventory & cost of goods sold. Merchandising companies sell inventory and service companies do not. Gross profit is the excess of sale

372

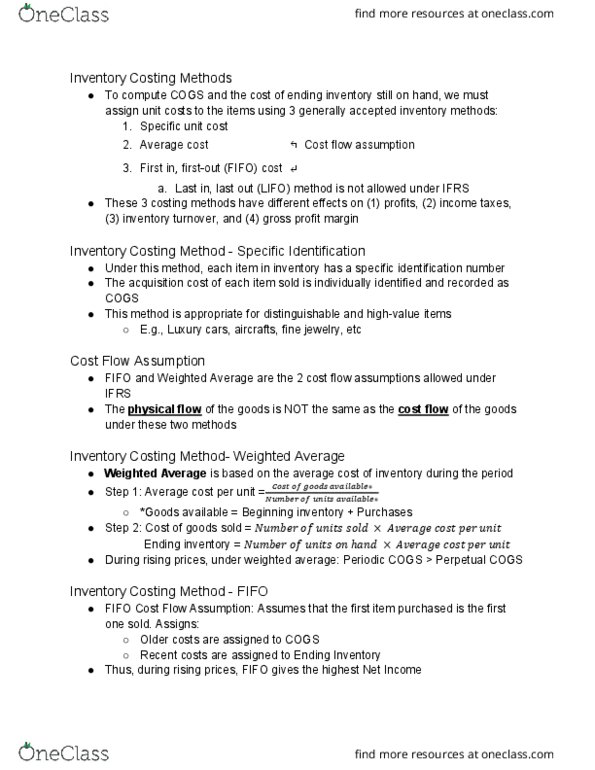

AFM101 Lecture Notes - Lecture 14: Inventory Turnover, Weighted Arithmetic Mean, Gross Profit

These 3 costing methods have different effects on (1) profits, (2) income taxes, (3) inventory turnover, and (4) gross profit margin. Under this method

2123

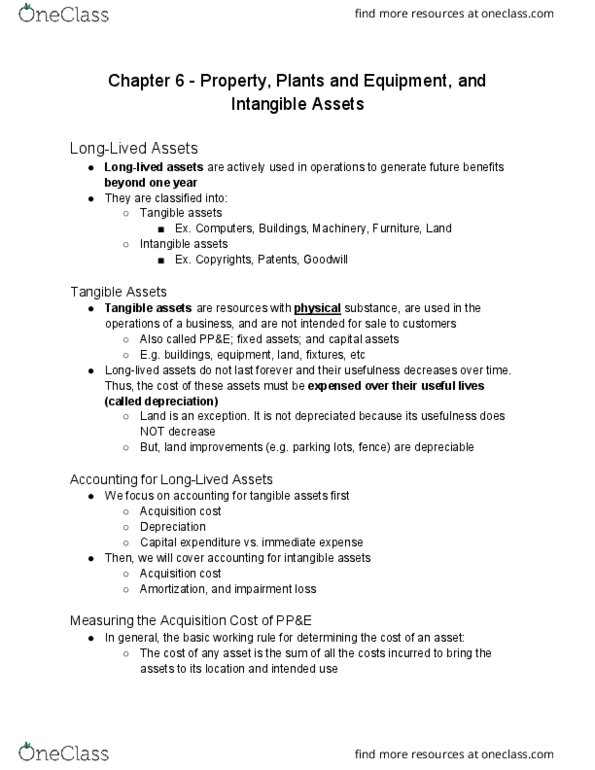

AFM101 Lecture Notes - Lecture 15: Asset, Land Development, Capital Expenditure

Chapter 6 - property, plants and equipment, and. Long-lived assets are actively used in operations to generate future benefits beyond one year. Tangibl

690

AFM101 Lecture Notes - Lecture 16: Book Value, Product Return, Intangible Asset

Companies purchase plant assets whenever they need them, not just at the beginning of the year. Thus, companies must compute depreciation for partial y

473

AFM101 Lecture Notes - Lecture 17: Agrium, Equity Method, Bruce Power

Chapter 7 - investments & the time value of money. The investor usually holds less than 20% of the voting shares and would normally play no importa

3117

AFM101 Lecture Notes - Lecture 18: Contingent Liability, Promissory Note, Current Liability

Liabilities are debts or obligations arising from past transactions that will be paid with assets or services in the future. There are two types of lia

591

AFM101 Lecture Notes - Lecture 19: Effective Interest Rate, Book Value, Operating Lease

Over the life of the bond issue, the discount and premium accounts are amortized. In the case of discounts: the discount is allocated to interest expen

5154

AFM101 Lecture Notes - Lecture 20: Legal Personality, Share Capital, Retained Earnings

Corporations differ from proprietorships and partnerships because of the following features: separate legal entity, continuous life and transferability

3165

AFM101 Lecture Notes - Lecture 21: Retained Earnings, Preferred Stock, Stock Split

4176