Verified Documents at Ohio State University

- Principles of Microeconomics

- Ohio State University

- Verified Notes

Browse the full collection of course materials, past exams, study guides and class notes for ECON 2001.01 - Principles of Microeconomics at Ohio State University verified by our …

PROFESSORS

All Professors

All semesters

Jeffrey Buser

fall

32Ida Mirzaie

fall

4Jeffrey Buser

fall

17William John White III

fall

4Verified Documents for Jeffrey Buser

Class Notes

Taken by our most diligent verified note takers in class covering the entire semester.

ECON 2001.01 Lecture 3: ECON2001.01, lec 3

We have learned that when markets allowed to reach their equilibrium, they are efficient; marginal benefit=marginal cost. Be competitive or behave as i

447

ECON 2001.01 Lecture 4: ECON2001.01, lec 4

Mother theresa used money given to her to help the poor. This is acting in self interest because her goal is to help the poor. When market are working

322

ECON 2001.01 Lecture 5: ECON2001.01, lec 5

Law of supply holds 90% of the time - not too bad. Supple refers to the quantity of a good that sellers are willing and able to supply to the market at

231

ECON 2001.01 Lecture 6: ECON2001.01, lec 6

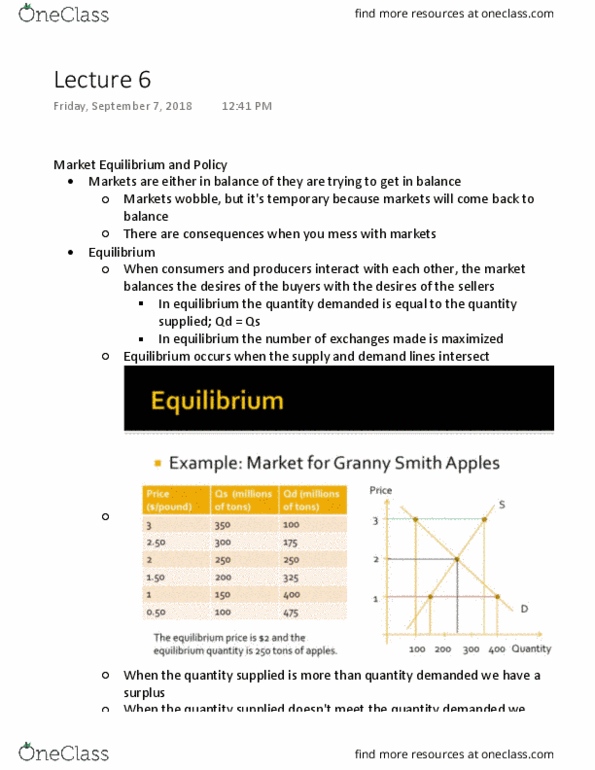

Markets are either in balance of they are trying to get in balance. Markets wobble, but it"s temporary because markets will come back to balance. There

720

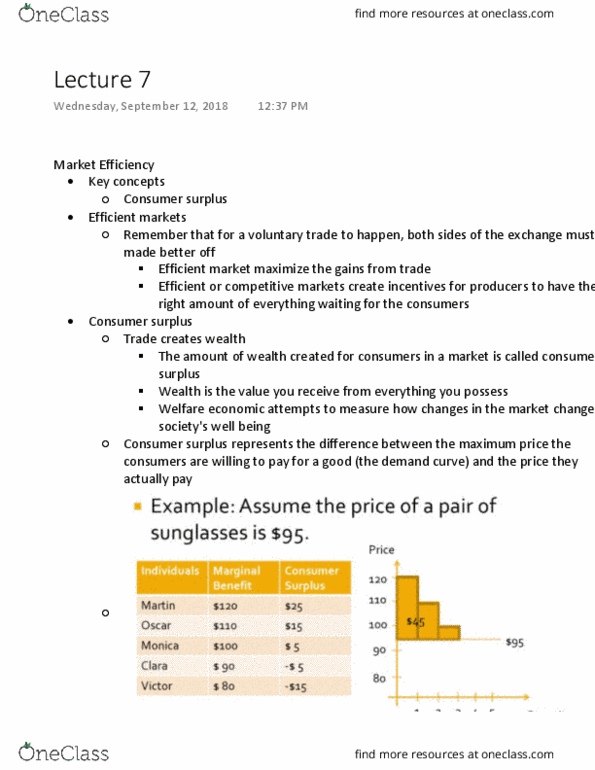

ECON 2001.01 Lecture Notes - Lecture 7: Planned Economy, Marginal Utility, Marginal Cost

Remember that for a voluntary trade to happen, both sides of the exchange must b made better off. Efficient or competitive markets create incentives fo

1223

ECON 2001.01 Lecture 8: ECON2001.01, lec 8

241

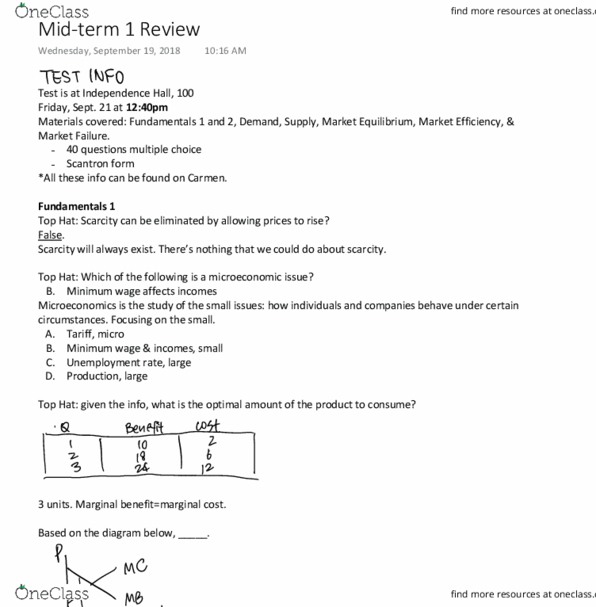

ECON 2001.01 Lecture 9: Mid-term 1 Review

2433

ECON 2001.01 Lecture 9: ECON2001.01, lec 9

The law of demand is a fundamental law in economics that describes the relationship between the price of a good, service, or resource and the quantity

237

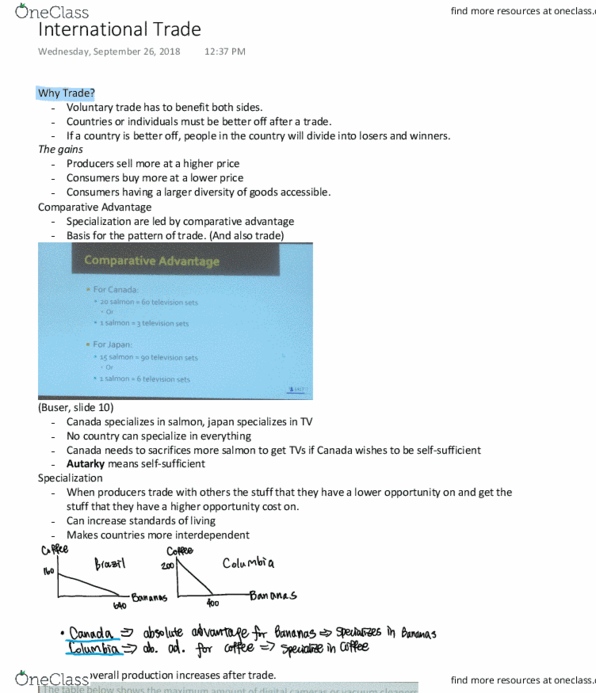

ECON 2001.01 Lecture Notes - Lecture 11: Autarky, Comparative Advantage, Opportunity Cost

We have learned that any voluntary exchange must be beneficial to both sides. Exchanges between two individuals must leave both individuals better off.

225

ECON 2001.01 Lecture Notes - Lecture 11: Opportunity Cost

Voluntary trade has to benefit both sides. Countries or individuals must be better off after a trade. If a country is better off, people in the country

269

ECON 2001.01 Lecture Notes - Lecture 12: Trade Restriction, Price Floor, Deadweight Loss

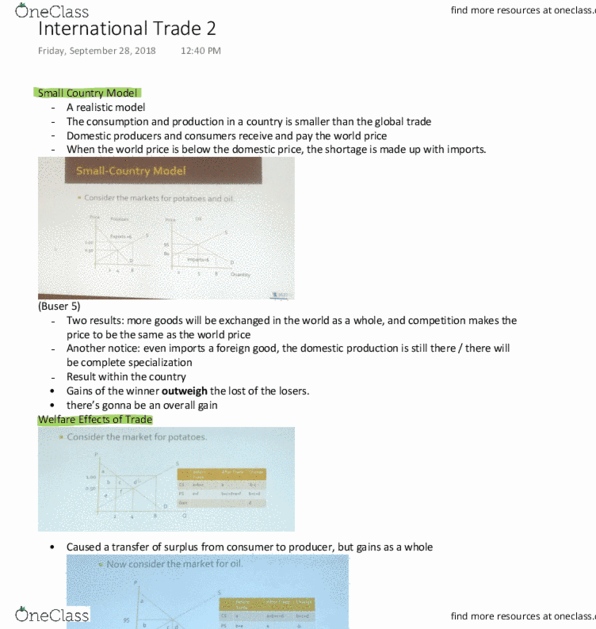

A more realistic model of international trade is called the small-country model. The small-country model assumes the production and consumption of a go

321

ECON 2001.01 Lecture Notes - Lecture 12: Voluntary Export Restraints

The consumption and production in a country is smaller than the global trade. Domestic producers and consumers receive and pay the world price. When th

249

ECON 2001.01 Lecture Notes - Lecture 13: Arc Elasticity, Demand Curve, Dependent And Independent Variables

Elasticity is a measure of sensitivity to a change. Elasticity is the ratio of the percentage change in a dependent variable to a percentage change in

331

ECON 2001.01 Lecture 13: Elasticity

249

ECON 2001.01 Lecture 14: Elasticity (continued)

261

ECON 2001.01 Lecture Notes - Lecture 14: Tax Incidence, Price Elasticity Of Demand, Normal Good

In addition to the effect of the product"s own price on sales, income and the prices of related goods also have an effect that a seller should anticipa

334

ECON 2001.01 Lecture Notes - Lecture 15: Demand Curve, Utility Maximization Problem, Normal Good

We have seen that one side of a market is made up of consumers; the demand side. The law of demand says that, all else equal, as the price of a product

528

ECON 2001.01 Lecture 15: Consumer Theory

12:37 pm (review) that the law of demand says the higher the price is, the lower the demand is gonna be. Consumers buy things to satisfy their needs. U

270

ECON 2001.01 Lecture Notes - Lecture 17: Marginal Product, Production Function, Diminishing Returns

Goal: firms always seek to maximize their profits. The payment required to gain and keep services of a resource. Economic costs = explicit costs + impl

188

ECON 2001.01 Lecture Notes - Lecture 18: Marginal Product, Diminishing Returns, Mass Production

Looking at the average cost of production: average total cost = tc/q, average fixed cost = tfc/q, average variable cost = tvc/q (buser 3) Atc and avc n

2102

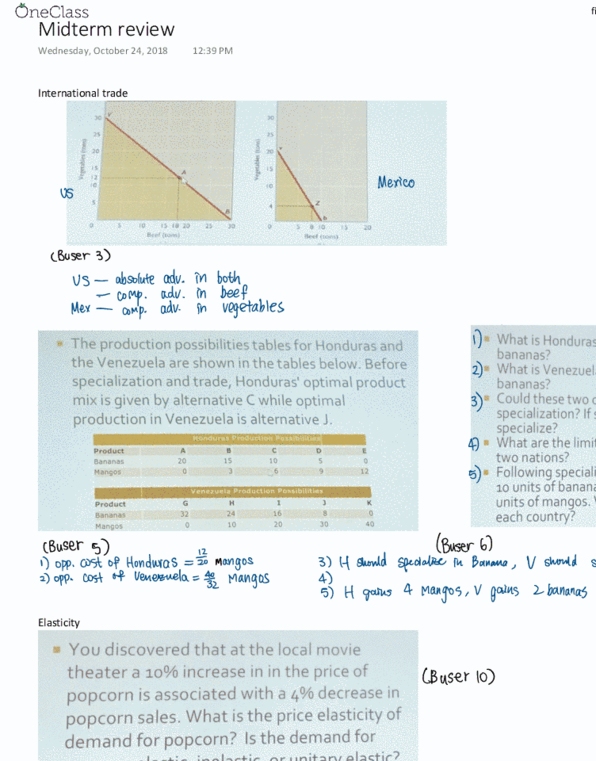

ECON 2001.01 Lecture 19: Midterm review

1104

ECON 2001.01 Lecture Notes - Lecture 21: Demand Curve

261

ECON 2001.01 Lecture Notes - Lecture 22: Fixed Cost

248

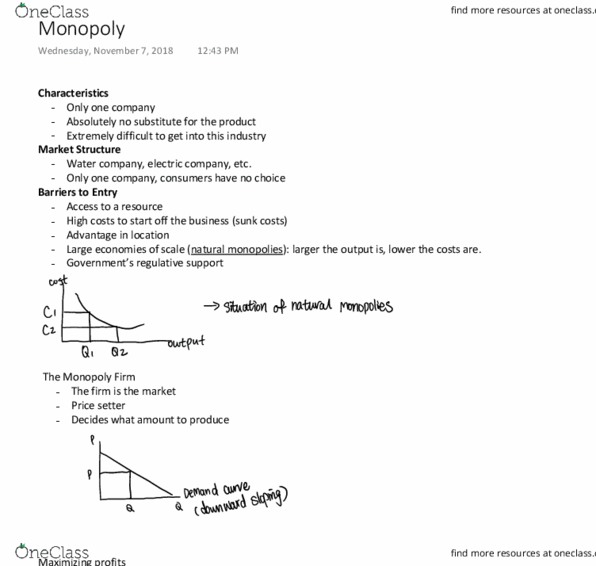

ECON 2001.01 Lecture 23: Monopoly

248

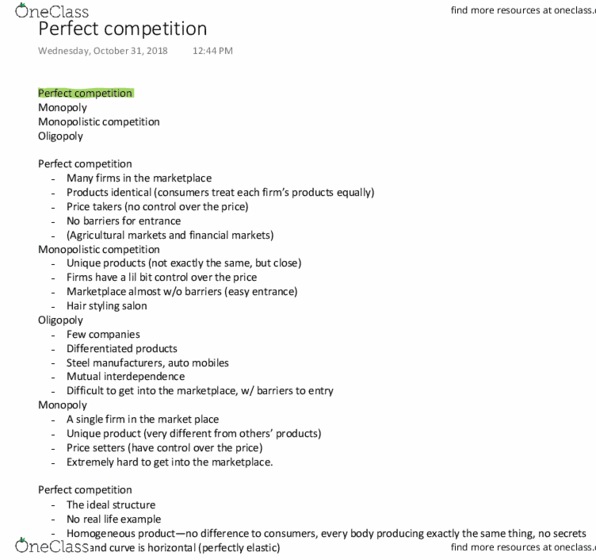

ECON 2001.01 Lecture Notes - Lecture 24: Perfect Competition, Allocative Efficiency, Demand Curve

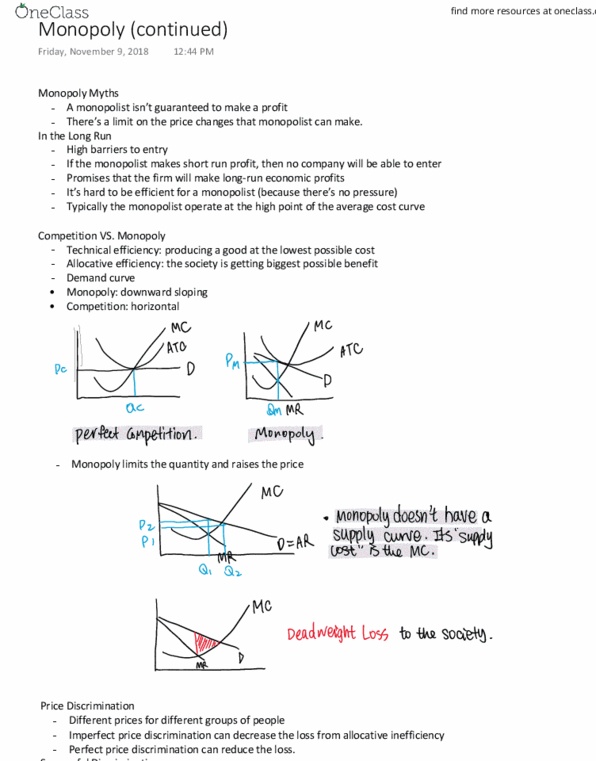

Can"t be higher than the demand curve. Competition vs monopoly: a comparison of monopoly to perfect competition will be made on two issues. Allocative

527

ECON 2001.01 Lecture Notes - Lecture 24: Price Discrimination, Allocative Efficiency, Marginal Revenue

A monopolist isn"t guaranteed to make a profit. There"s a limit on the price changes that monopolist can make. If the monopolist makes short run profit

139

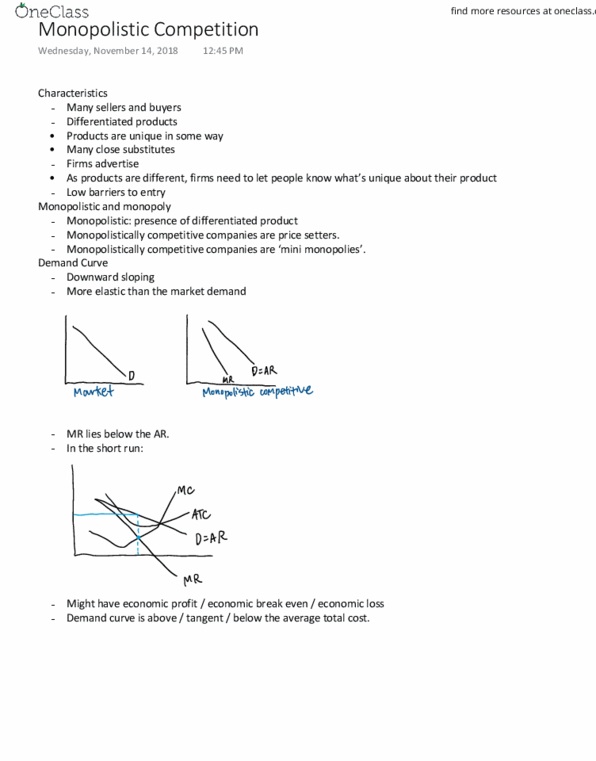

ECON 2001.01 Lecture Notes - Lecture 25: Monopolistic Competition, Demand Curve

142

ECON 2001.01 Lecture Notes - Lecture 26: Autism Spectrum, Frontal Lobe, Grey Matter

More likely to say yes (activates reward-seeking behaviors) More likely to say no (more anxiety) It will be activated when there"s lack of reward or pr

149

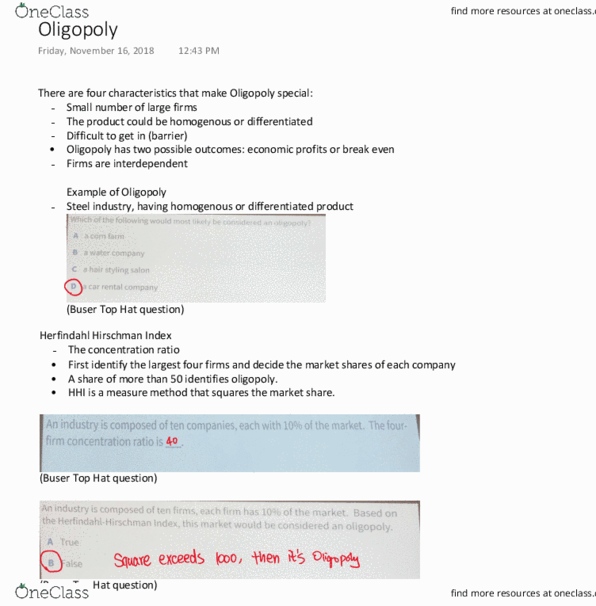

ECON 2001.01 Lecture 26: Oligopoly

261

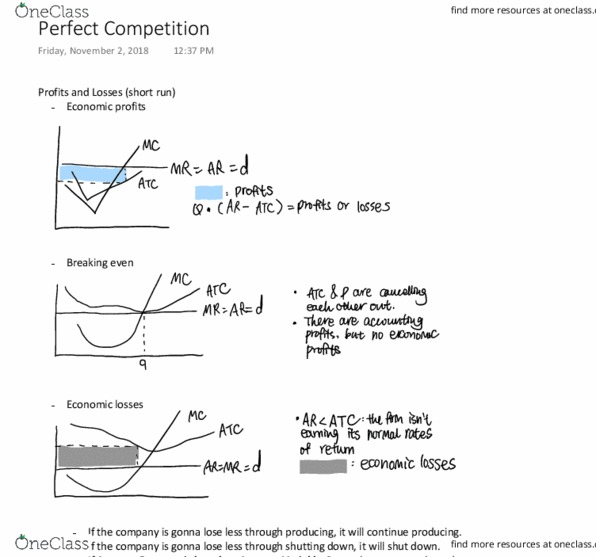

ECON 2001.01 Lecture Notes - Lecture 29: Perfect Competition

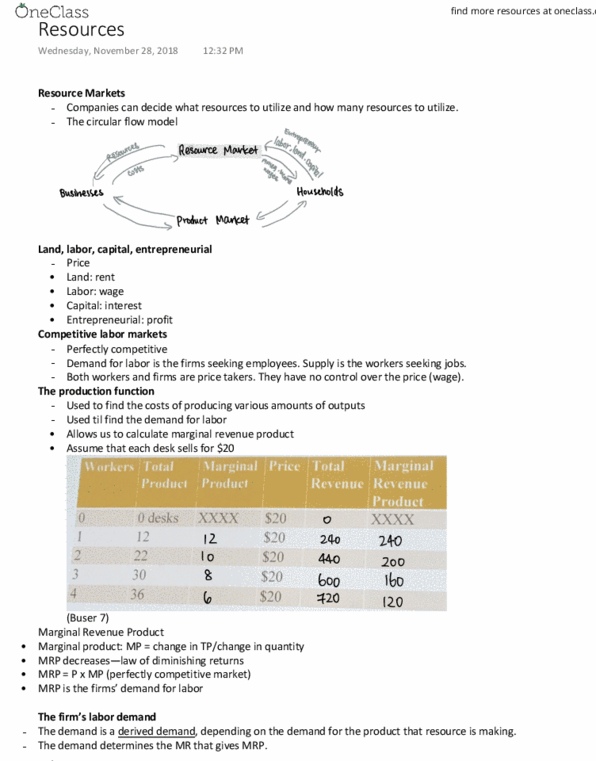

Companies can decide what resources to utilize and how many resources to utilize. Price: land: rent, labor: wage, capital: interest, entrepreneurial: p

275

ECON 2001.01 Lecture 30: Labor Market

Payoff = revenue from the labor - wage. Entire round: sum of payoffs from each hire. Change in number of companies trying to hire workers. Depending on

196

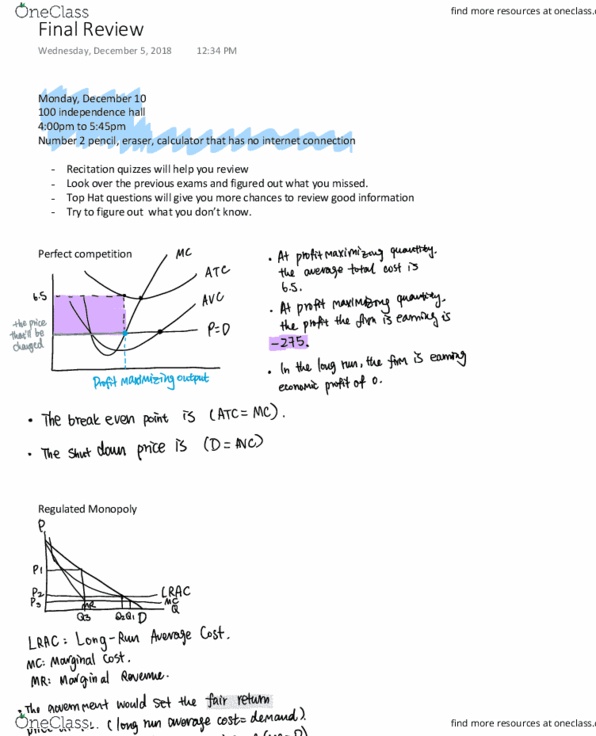

ECON 2001.01 Lecture 31: Final Review

2120