Verified Documents at Rutgers University

- Introduction to Microeconomics

- Rutgers University

- Verified Notes

Browse the full collection of course materials, past exams, study guides and class notes for 01:220:102 - Introduction to Microeconomics at Rutgers University verified by our …

PROFESSORS

All Professors

All semesters

Hohmann

fall

9Daijiro Okada

fall

2Elgawly

fall

18kadambe

fall

4goldband

fall

19JACK SKYDEL

fall

5Verified Documents for Elgawly

Class Notes

Taken by our most diligent verified note takers in class covering the entire semester.

01:220:102 Lecture Notes - Lecture 1: Profit Motive, Opportunity Cost, The Incentive

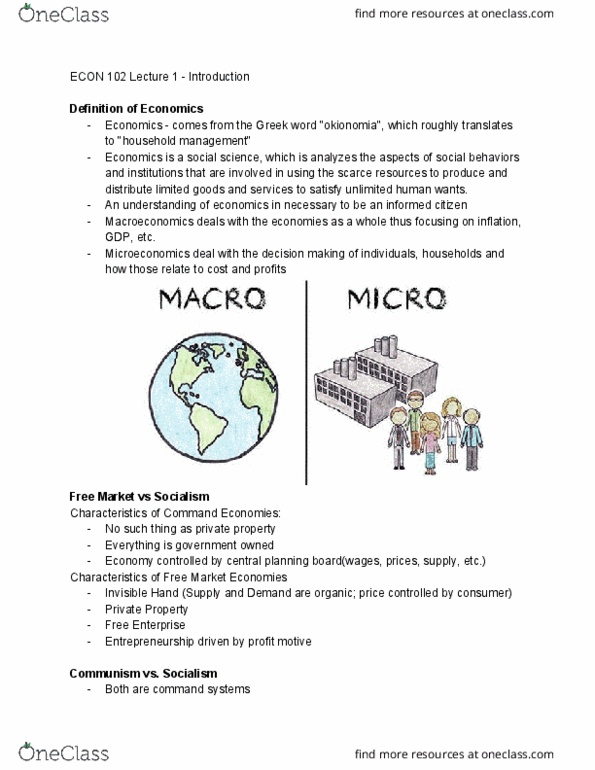

Economics - comes from the greek word "okionomia", which roughly translates to "household management" Economics is a social science, which is analyzes

2266

01:220:102 Lecture Notes - Lecture 2: Opportunity Cost, Demand Curve

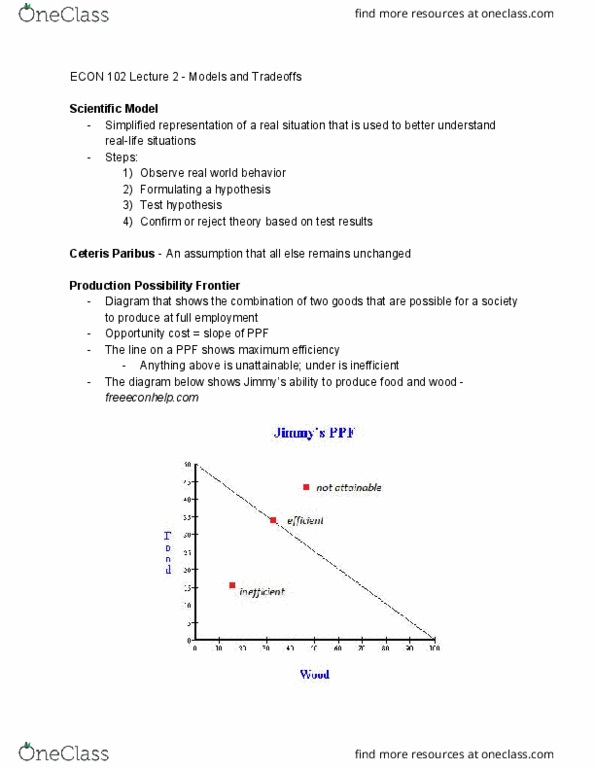

Econ 102 lecture 2 - models and tradeoffs. Simplified representation of a real situation that is used to better understand real-life situations. Steps:

2105

01:220:102 Lecture Notes - Lecture 2: Capital Good, Fallacy, Opportunity Cost

Economics - is derived from a greek word "okionomia", which means "household management" or "management of house affairs . Definition of economics - ec

544

01:220:102 Lecture Notes - Lecture 3: Human Capital, Absolute Advantage, Comparative Advantage

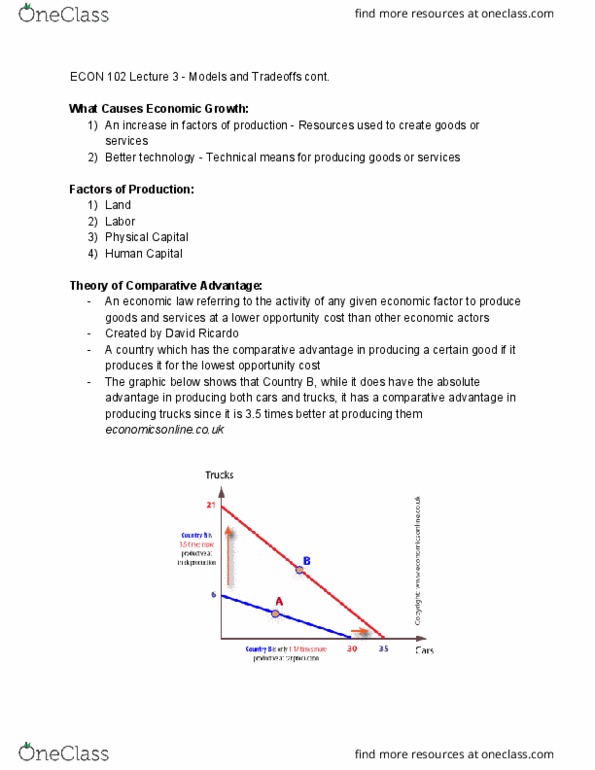

Econ 102 lecture 3 - models and tradeoffs cont. What causes economic growth: an increase in factors of production - resources used to create goods or s

277

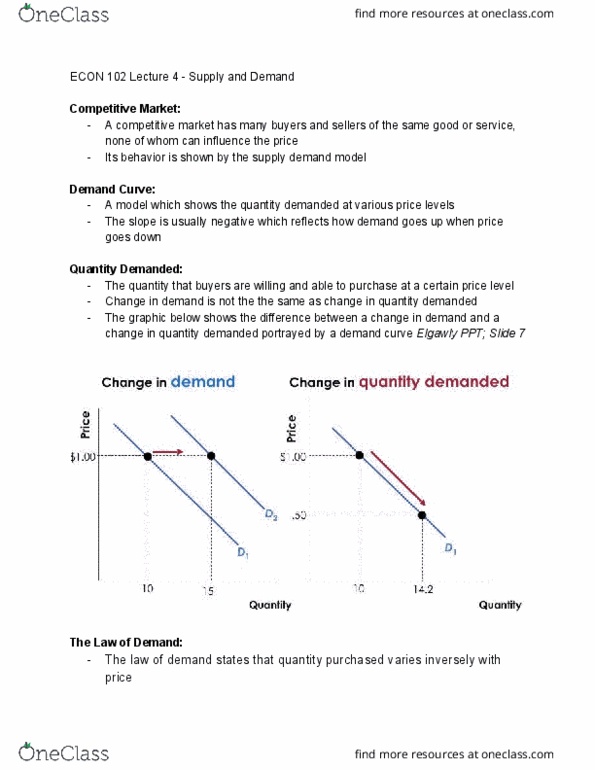

01:220:102 Lecture Notes - Lecture 4: Demand Curve, The Graphic, Economic Equilibrium

Econ 102 lecture 4 - supply and demand. A competitive market has many buyers and sellers of the same good or service, none of whom can influence the pr

3184

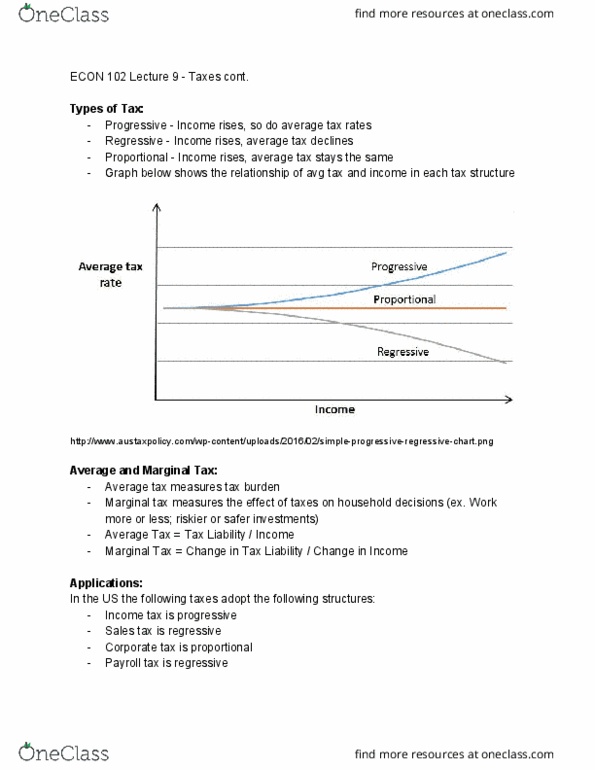

01:220:102 Lecture Notes - Lecture 10: Sales Tax, Tax Bracket, Payroll Tax

Progressive - income rises, so do average tax rates. Regressive - income rises, average tax declines. Proportional - income rises, average tax stays th

3156

01:220:102 Lecture 14: ECON 102 Lecture 14 - Decision Making by Individuals and Firms

Econ 102 lecture 14 - decision making by individuals and firms. Explicit cost is a cost that occurs, is easily identified, and is accounted for in busi

3177

01:220:102 Lecture Notes - Lecture 15: Italian General Confederation Of Labour

399

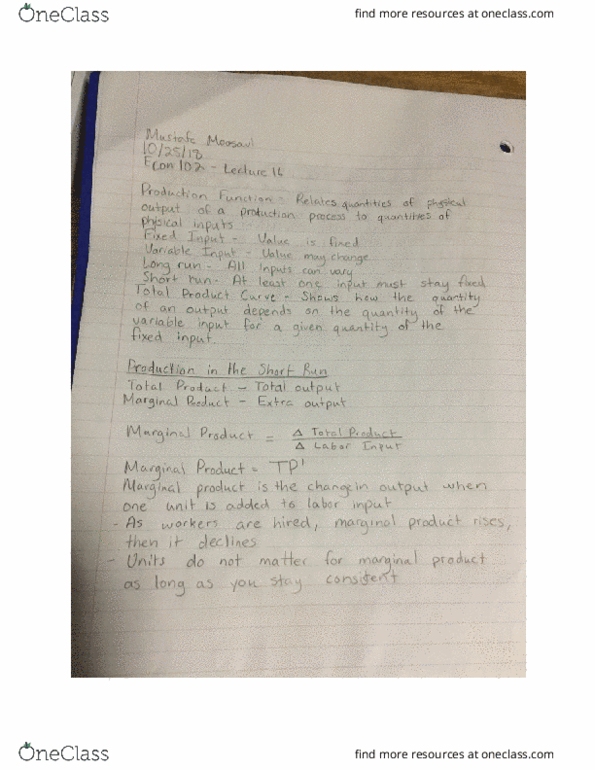

01:220:102 Lecture Notes - Lecture 16: Liquid Oxygen, Cost Curve, Sam Lecure

3111

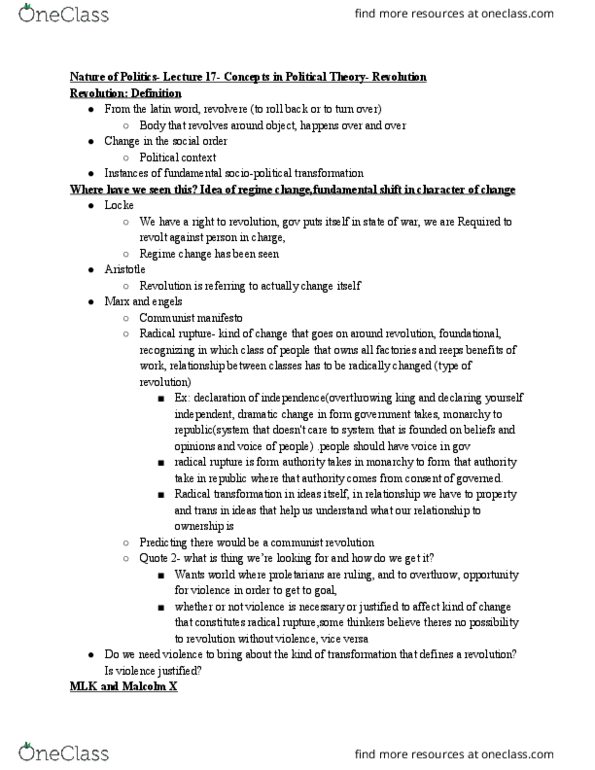

01:220:102 Lecture Notes - Lecture 17: The Communist Manifesto, Institute For Operations Research And The Management Sciences, Black Nationalism

Nature of politics- lecture 17- concepts in political theory- revolution. From the latin word, revolvere (to roll back or to turn over) Body that revol

451

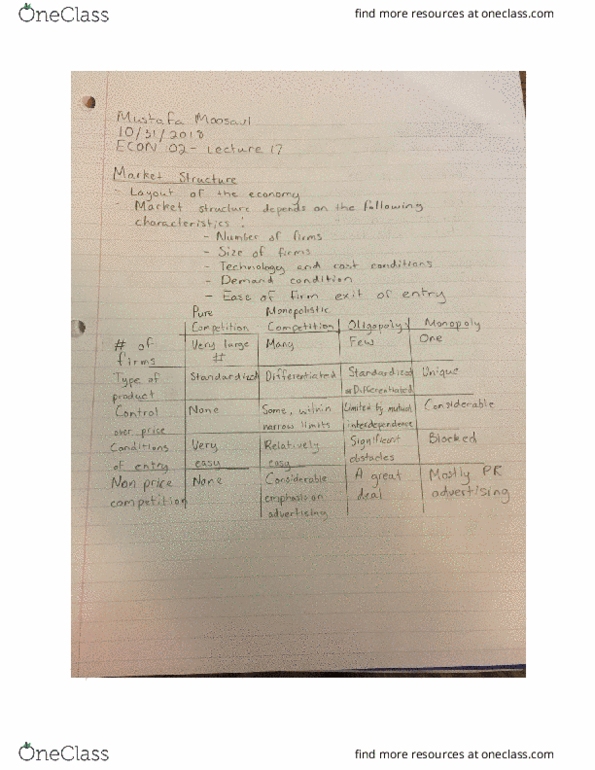

01:220:102 Lecture 17: Market Structure

3109

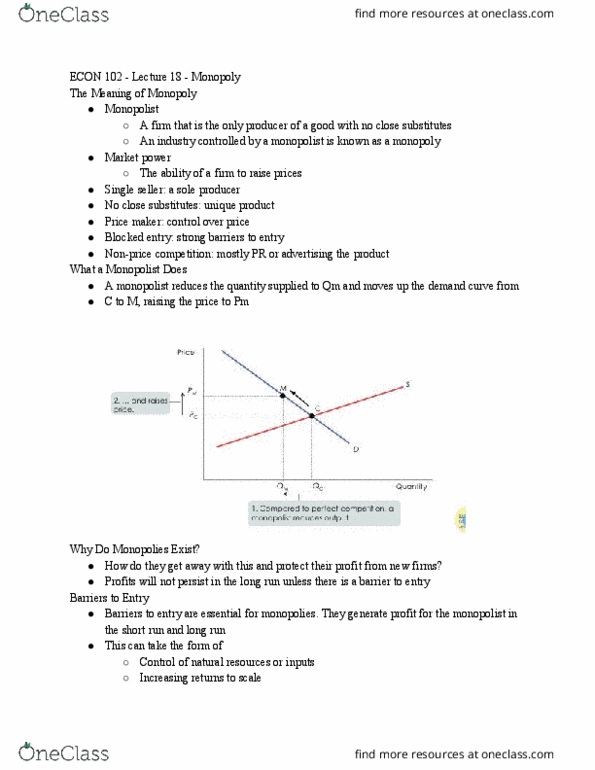

01:220:102 Lecture Notes - Lecture 18: Market Power, Demand Curve, Marginal Revenue

A firm that is the only producer of a good with no close substitutes. An industry controlled by a monopolist is known as a monopoly. The ability of a f

4140

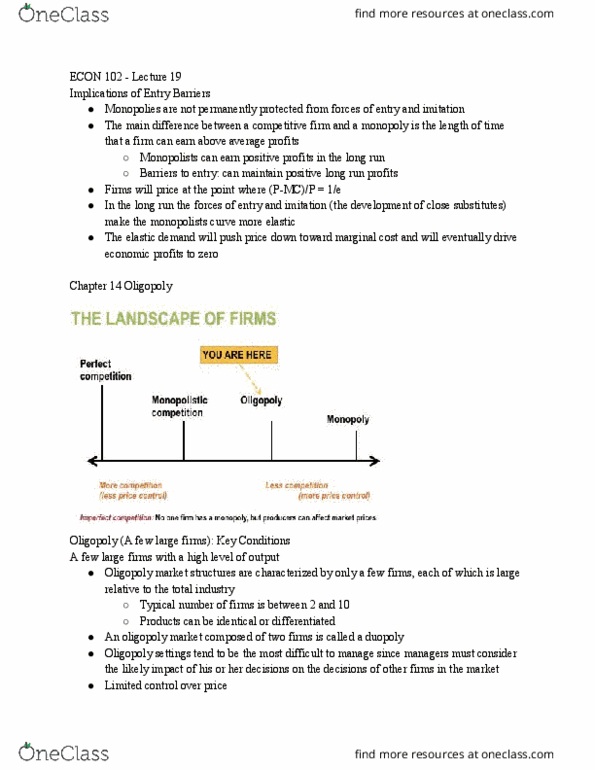

01:220:102 Lecture Notes - Lecture 19: Oligopoly, Marginal Cost, Product Differentiation

Monopolies are not permanently protected from forces of entry and imitation. The main difference between a competitive firm and a monopoly is the lengt

3140

01:220:102 Lecture Notes - Lecture 20: Tacit Collusion, Nash Equilibrium, Oligopoly

A decision rule that describes actions a player will take. Representation of a game indicating the players, their strategies, and the payoffs resulting

3138

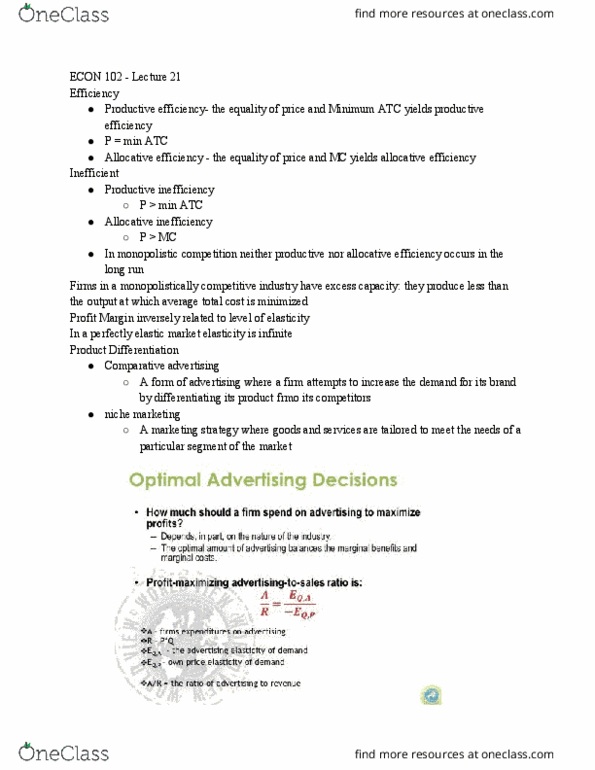

01:220:102 Lecture Notes - Lecture 21: Allocative Efficiency, Monopolistic Competition, Productive Efficiency

Productive efficiency- the equality of price and minimum atc yields productive efficiency. Allocative efficiency - the equality of price and mc yields

2253

01:220:102 Lecture Notes - Lecture 25: Economic Equilibrium

3146

01:220:102 Lecture Notes - Lecture 26: Abstract Window Toolkit, Import Quota

3148

01:220:102 Lecture Notes - Lecture 27: Externality, Market Failure, Lection

3209