5

answers

1

watching

1,747

views

27 Apr 2018

1. A perfectly competitive firm will continue producing in the short run as long as it can cover its:

A.total cost. B.average total cost. C.average variable cost. D.average fixed cost.

2. A perfectly competitive firm will earn a profit and will continue producing the profit-maximizing quantity of output in the short run if price is: A.greater than marginal cost. B.less than marginal cost. C.less than average variable cost. D.greater than average total cost.

3. Monopolistic competition is an industry characterized by: A.a product with many close substitutes. B.a horizontal demand curve. C.a small number of firms. D.barriers to entry and exit.

4. If a perfectly competitive firm increases production from 10 units to 11 units, and the market price is $20 per unit, total revenue for 10 units is: A.$10. B.$20 C.$200. D.$210.

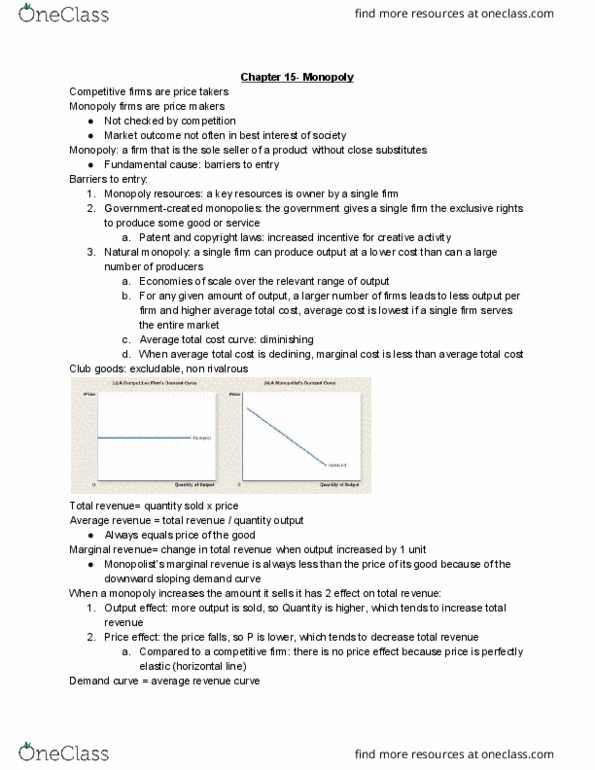

5. The demand curve facing a monopolist is: A.horizontal, the same as that facing a perfectly competitive firm. B.downward sloping, the same as that facing a perfectly competitive firm. C.upward sloping, the same as that facing a perfectly competitive firm. D.downward sloping, unlike the horizontal demand curve facing a perfectly competitive firm.

6. Suppose that a monopolist increases production from 10 units to 11 units. If the market price declines from $30 per unit to $29 per unit, marginal revenue for the eleventh unit is: A.$1. B.$9. C.$19. D.$29.

7. Most electric, gas, and water companies are examples of: A.unregulated monopolies. B.natural monopolies. C.restricted-input monopolies. D.sunk-cost monopolies.

8.If a perfectly competitive firm is producing a quantity that generates P > MC, then profit: A.is maximized. B.can be increased by increasing the price. C.can be increased by decreasing the price. D.can be increased by increasing production.

1. A perfectly competitive firm will continue producing in the short run as long as it can cover its:

| A.total cost. | |

| B.average total cost. | |

| C.average variable cost. | |

| D.average fixed cost. |

| A.greater than marginal cost. | |

| B.less than marginal cost. | |

| C.less than average variable cost. | |

| D.greater than average total cost. |

| A.a product with many close substitutes. | |

| B.a horizontal demand curve. | |

| C.a small number of firms. | |

| D.barriers to entry and exit. |

| A.$10. | |

| B.$20 | |

| C.$200. | |

| D.$210. |

| A.horizontal, the same as that facing a perfectly competitive firm. | |

| B.downward sloping, the same as that facing a perfectly competitive firm. | |

| C.upward sloping, the same as that facing a perfectly competitive firm. | |

| D.downward sloping, unlike the horizontal demand curve facing a perfectly competitive firm. |

| A.$1. | |

| B.$9. | |

| C.$19. | |

| D.$29. |

| A.unregulated monopolies. | |

| B.natural monopolies. | |

| C.restricted-input monopolies. | |

| D.sunk-cost monopolies. |

| A.is maximized. | |

| B.can be increased by increasing the price. | |

| C.can be increased by decreasing the price. | |

| D.can be increased by increasing production. |

Read by 1 person

malupiton2022Lv10

12 Oct 2022

Read by 1 person

papayaprofessorLv10

5 Sep 2022

Already have an account? Log in

Read by 1 person

Read by 1 person

Jeffrey

JD Candidate at Stanford Law School30 Jun 2020

Answer verification

This is a step by step verification of the answer by our certified expert.

Subscribe to our livestream channel for more helpful videos.