ACC 110 Chapter 3: A Critical Approach 3e _ Chapter 3 Answers

14 Apr 2011

School

Department

Course

Professor

Document Summary

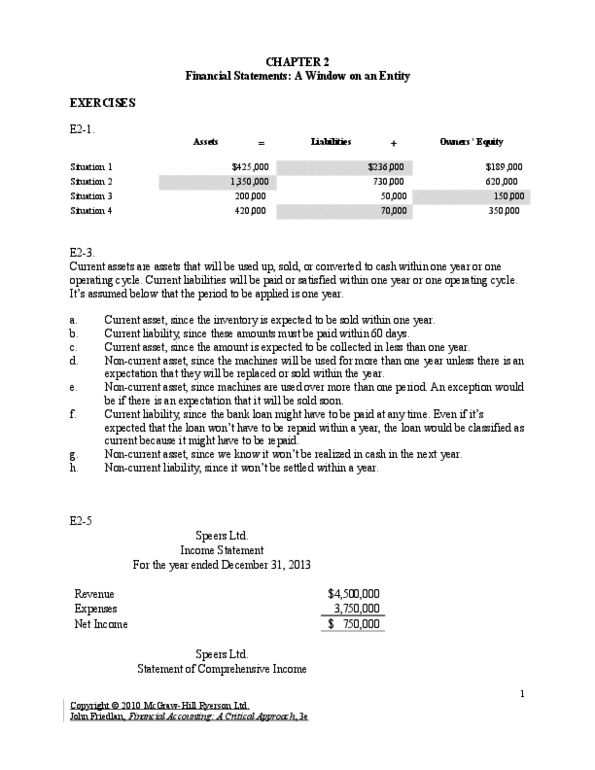

E3 1: adjusting entry b, no entry or adjusting (allowed by ifrs, adjusting entry, no entry f, adjusting entry h. i. j, no entry transactional entry transactional entry transactional entry. 850,000: the primary purposes of closing entries are to reset the balances in the temporary (income statement) accounts to zero and to transfer the amounts in those accounts to retained earnings. 900 a b c d e f g h i j. Professional fees b c d e f g h i j. E3 13: equipment was purchased for . 1 million, with ,000 paid in cash and the remainder on credit. b. Cash is to be received in a later period: land was sold for cash and an amount that is to be paid in the future. ,000 of services provided at the time of payment: supplies that were used during the period were expensed. The spreadsheet for this exercise is shown twice.