ACC 410 Chapter 5: Chapter 5

15 Apr 2011

School

Department

Course

Professor

Document Summary

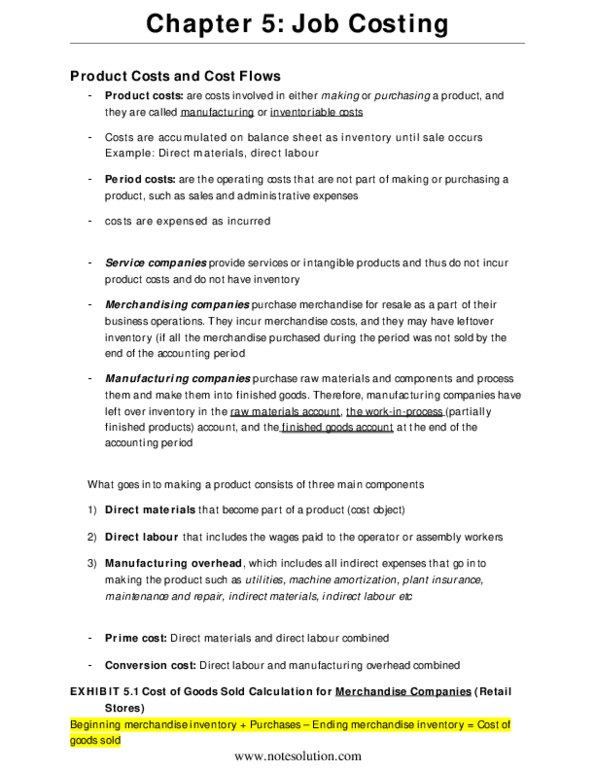

product costs: costs involved in either making or purchasing a product (manufacturing, inventorable costs, direct or indirect costs) period costs: operating costs that are not part of making or purchasing a product, such as sales and administrative expenses (ex: sales or administrative expenses) manufacturing companies may have leftover inventories in the raw materials account, work in process account, and the finished goods account at the end of the accounting period. managers need to prepare the cost of goods sold schedule and cost of goods manufactured schedule as a part of preparing the income statement. prime costs: direct materials and direct labour. conversion costs: direct labour and manufacturing overhead (these two costs convert materials into finished goods) calculating cost of goods sold for merchandising companies. cogs = beginning merchandise inventory + purchases ending merchandise inventory. calculating cost of goods sold for manufacturing companies.