MGT 200 Lecture Notes - Lecture 10: Standard Deviation, Weighted Arithmetic Mean, Lead

Document Summary

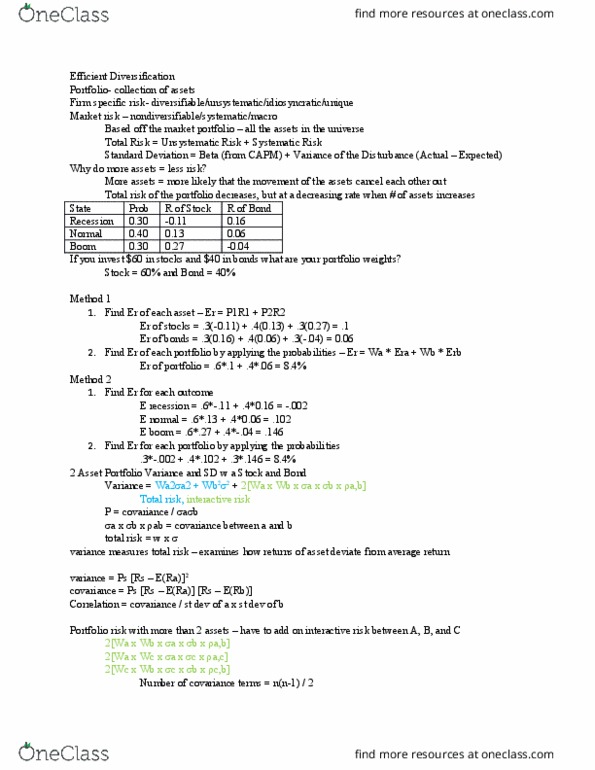

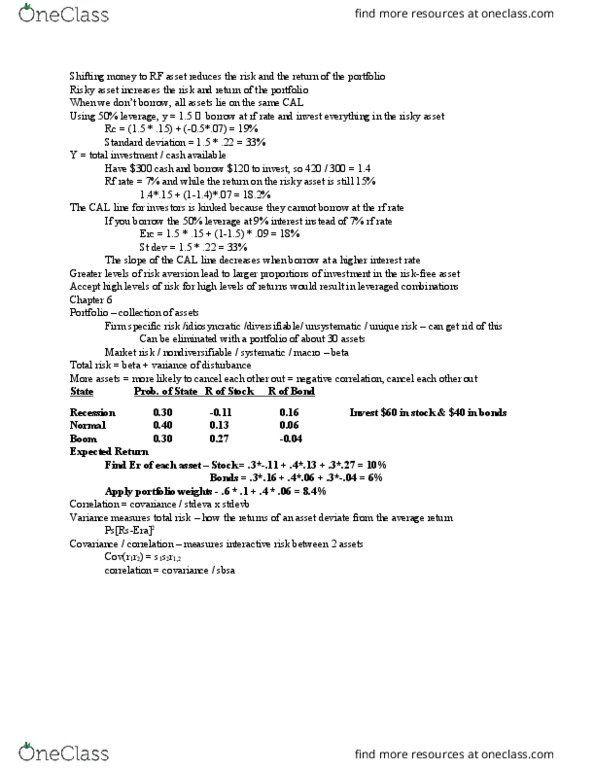

Portfolio risk depends on the covariance between the returns of the assets in the portfolio. Bonds outperform stocks in mild and severe recessions. In normal growth and boom scenarios, stocks outperform bonds. Portfolio return is the weighted average of the returns on each fund. Portfolio risk is reduced when returns of the two assets offset each other. Covariance whether deviations from the mean move together. Correlation coefficient = covariance / st dev a x st dev b (rho or p) Correlation of 1 linear regression; slope coefficient would be negative and r2 = 100% R2 tells you the fraction of variance of one return explained by the other. Two risky asset portfolios: rate of return of portfolio , e(r) of portfolio , variance of portfolio , pb,s is the correlation coefficient between returns on stock and bond funds, we replace the last term with 2wbwscov(rb, rs).