ECON 295 Chapter Notes - Chapter 20: Black Market, Gdp Deflator, Gross National Product

3 Apr 2013

School

Department

Course

Professor

Document Summary

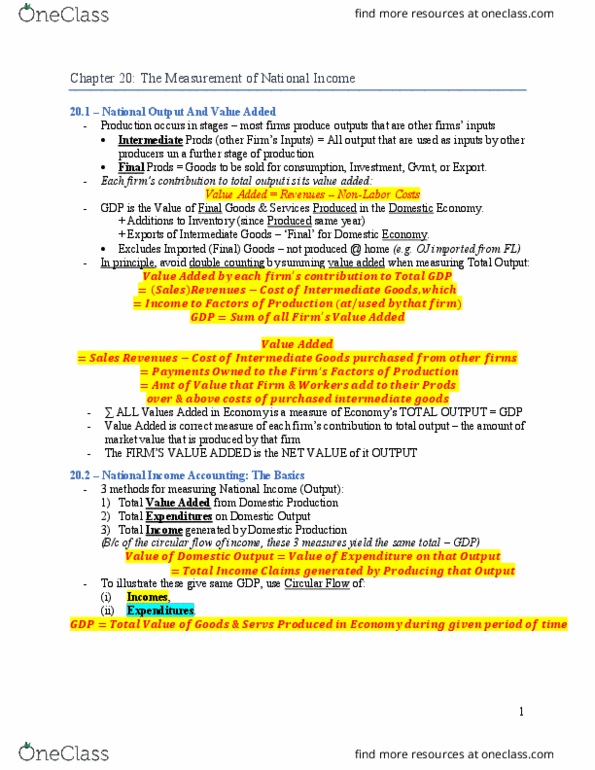

Production occurs in stages: some firms produce outputs that are used as inputs by other firms, and these other firms, in turn, produce outputs that are used as inputs by yet other firms. Intermediate goods: all outputs that are used as inputs by other producers in a further stage of production. Final goods: goods that are not used as inputs by other firms but are produced to be sold for consumption, investment, government, or exports during the period under consideration. Value added: the value of a firm"s output minus the value of the inputs that it purchases from other firms. Value added = revenue cost of intermediate goods. Value added = payments to factors of production (such as wages paid to workers or profits paid to owners) Value added is the correct measure of each firm"s contribution to total output the amount of market value that is produced by that firm.