MGAB01H3 Chapter 5.1: Chapter 5.1

16

MGAB01H3 Full Course Notes

Verified Note

16 documents

Document Summary

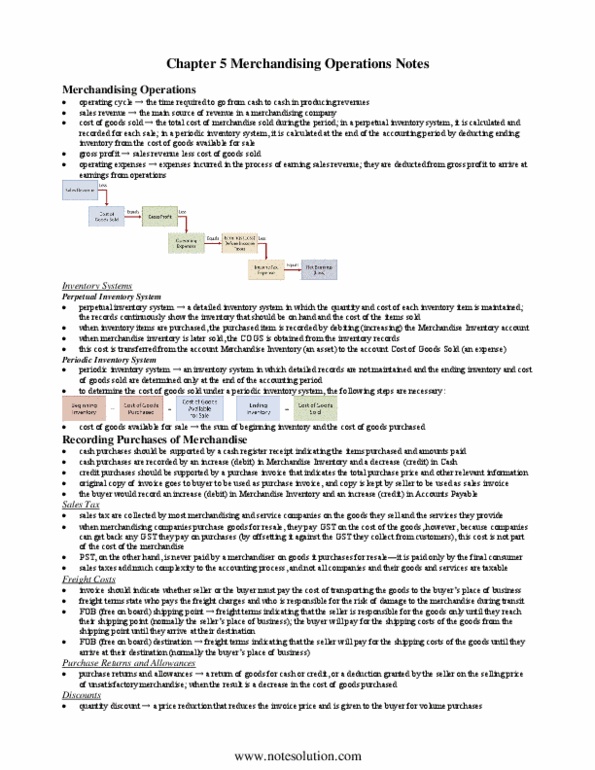

Merchandising involves purchasing products j also called merchandise inventory or just inventory j to resell to customers. The operating cycle j the time it takes to go from cash to cash in producing revenues j is usually longer for a merchandising company than it is for a service company. Unlike expenses for a service company, merchandising companies divide them into two categories: cost of goods sold and operating expenses. The cost of goods sold is the total cost of the merchandise that was sold during the period of time. This expense is directly related to the revenue that is recognized from the sale of goods. Sales revenue less the cost of goods sold is called gross profit. After gross profit is calculated, operating expenses are deducted to determine earnings before income tax. Operating expenses are expenses that are incurred in the process of earning sales revenue. Sales revenue j costs of goods sold = gross profits.