ECO101H1 : 4 - Monopoly

98

ECO101H1 Full Course Notes

Verified Note

98 documents

Document Summary

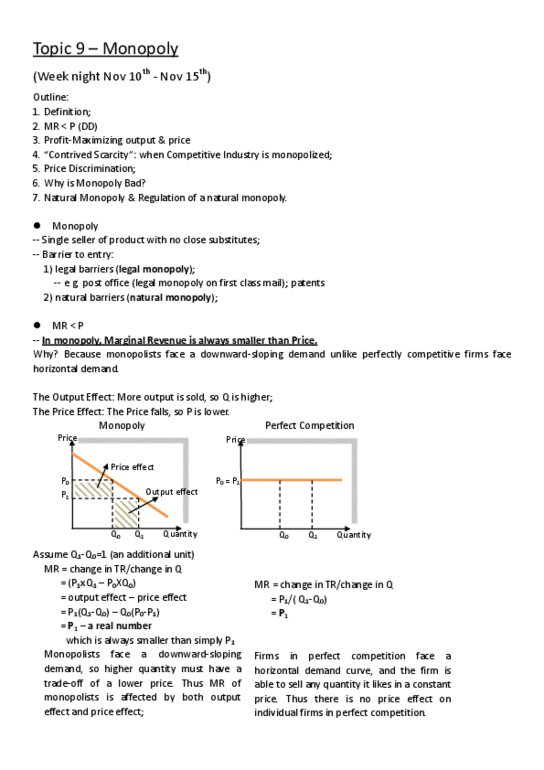

A monopoly is the sole producer in an industry. This means industry demand is demand for the monopoly and that the marginal cost and average cost functions of the monopoly are the marginal cost and average cost functions for the industry. Since price is not constant, marginal revenue is not equal to price for a monopolist. P is not constant and price is dependent upon the output of the monopoly, a monopoly can determine commodity price by restricting output. Profit maximization for a monopolist: mr = mc. Mr for linear demand has the same intercept term as the demand function and twice the slope. Elasticity is unit elastic at the midpoint of a demand function, which means that mr is 0 at the midpoint because total revenue doesn"t change. A monopoly will not produce in the inelastic portion of a demand function since a decrease in quantity will a) increase total revenue and b) reduce variable costs.