ECON 1B03 Chapter Notes - Chapter 14: Fixed Cost, Vise, Opportunity Cost

21 Aug 2013

School

Department

Course

Professor

46

ECON 1B03 Full Course Notes

Verified Note

46 documents

Document Summary

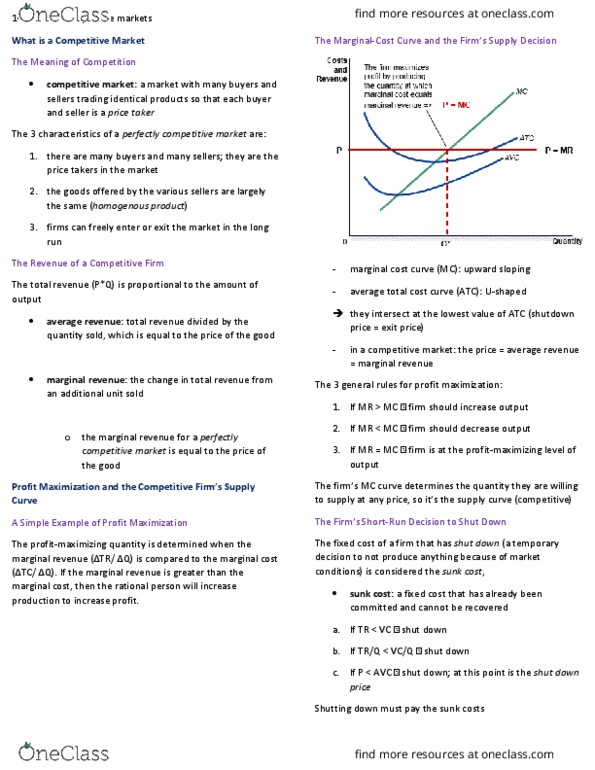

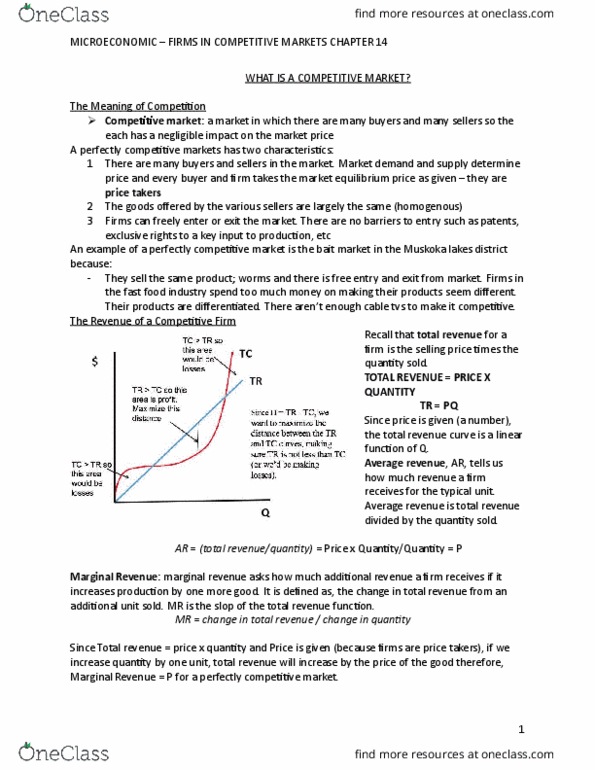

Competitive markets: 1) have many buyers and many sellers 2) the goods offered by the various sellers are largely the same. The actions of a single buyer or seller has minimal affect on the market price. Sometimes considered a characteristic: 3) firms can freely enter or exit the market in the long run. Total revenue is proportional to the amount of output (the price will not change) For all firms the average revenue (revenue/quantity) equals the price of the good. For competitive firms the marginal revenue (change in revenue/additional unit sold) equals the price of the good. Profit maximization and the competitive firm"s supply curve. Compare the marginal revenue and the marginal cost from each unit produced. As long as marginal revenue > marginal cost, increasing the products raises profit. The marginal-cost curve and the firm"s supply decision. Firms price = marginal revenue + average revenue.