Management and Organizational Studies 3370A/B Lecture Notes - Historical Cost, Financial Statement, Income Statement

9 Nov 2013

School

Department

Professor

Document Summary

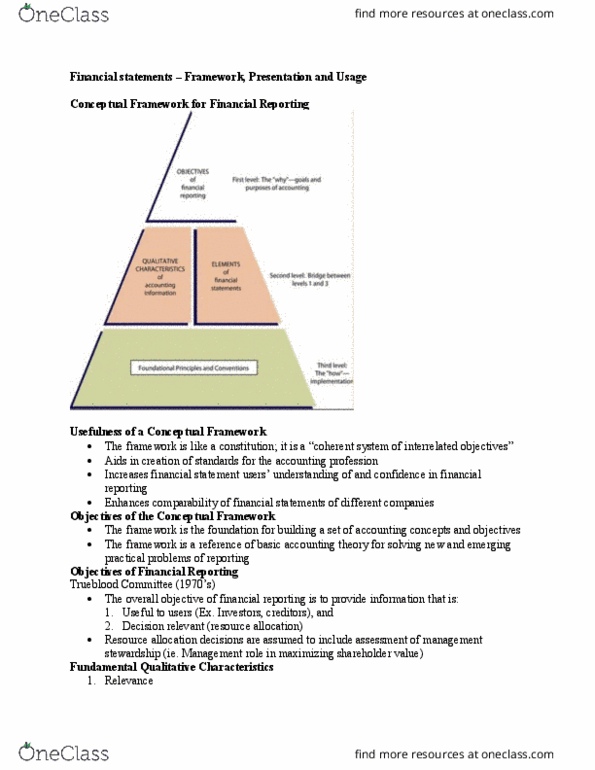

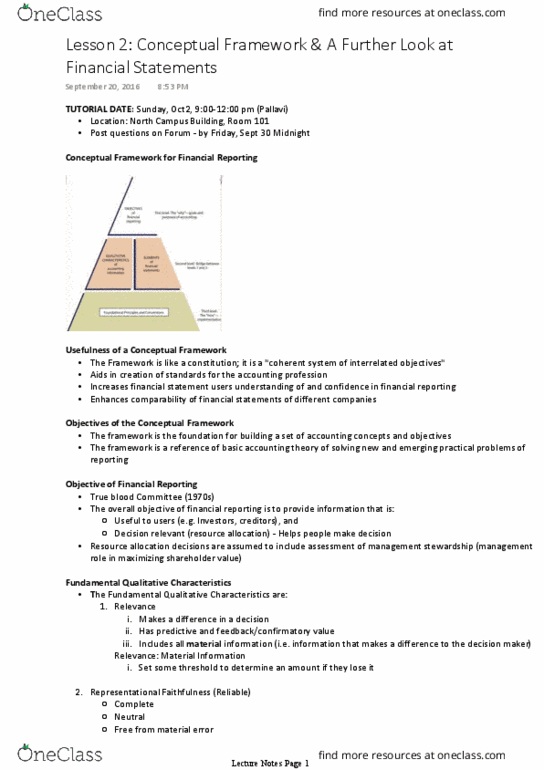

If leaving including information would influence/change the judgement of a reasonable person then that information is considered material. Quantitative guidelines for materiality professional judgement: cost vs. benefits. Benefits of using the information should outweigh the costs of providing that information. Liabilities: represent a duty or responsibility, entity is obligated and has little or no discretion to avoid the duty or responsibility, obligation results from a past transaction or event, what we owe. Equity: net assets, represents residual interest in assets after all liabilities have been paid. Increases in economic resources resulting from ordinary activities. Expenses: decreases in economic resources resulting from ordinary revenue generating activities. Recognition/derecognition: process of including an item on entity"s balance sheet or income statement, elements of financial statements have historically been recognized when . They meet the definition of an element (e. g. asset) Derecognition: process of removing something from the balance sheet or income statement.