BU227 Chapter Notes - Chapter 4: Deferred Income, Debits And Credits, Interest Expense

Document Summary

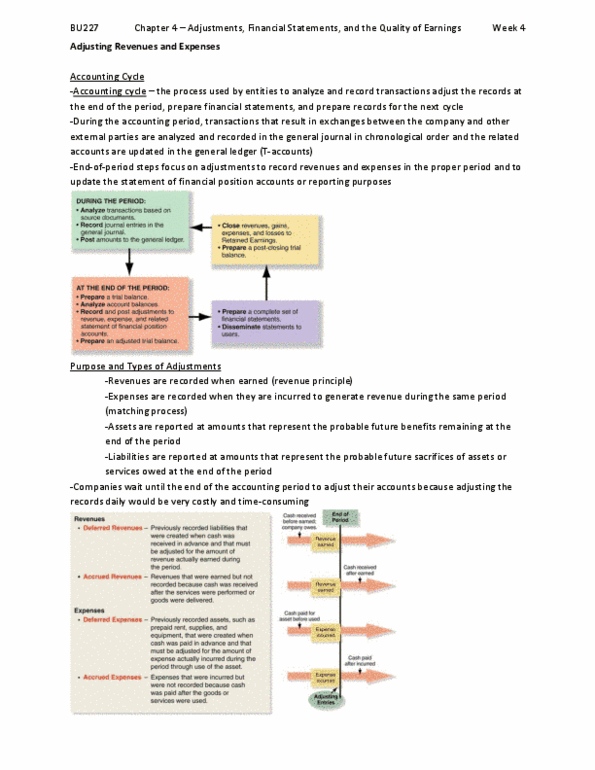

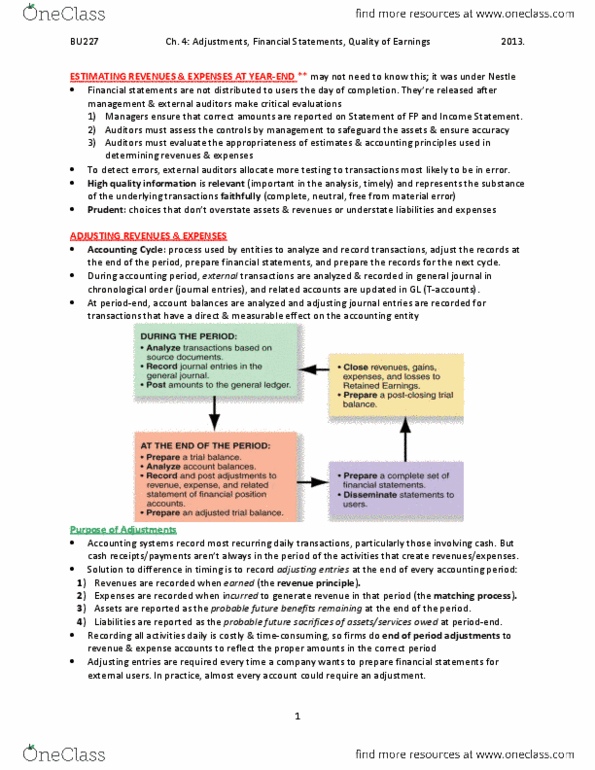

Process): assets are reported at amounts that represent the probable future benefits remaining at the end of the period, liabilities are reported at amounts that represent the probable future costs owed at the end of the period. Types of adjustments: deferred revenues (using fee revenue as an example): Previously recorded liabilities created when cash was received in. Advance, and must be adjusted for the amount of revenue actually earned that period. Entry during the period: + cash (asset, + deferred fee revenue (liability) Adjusting entry at the end of period: Deferred fee revenue (liability: + fee revenue (revenue, shareholder"s equity, accrued revenues (using interest as an example): Revenues that were earned, but not recorded, because cash was. Adjusting entry at the end of period: + interest receivable (asset, + interest revenue (revenue, shareholder"s equity) Entry at the beginning of next period (when cash is received. After the company performs service/earns revenue: + cash (asset)