RSM222H1 Chapter Notes - Chapter 8: Total Absorption Costing, European Cooperation In Science And Technology, Cash Flow

Document Summary

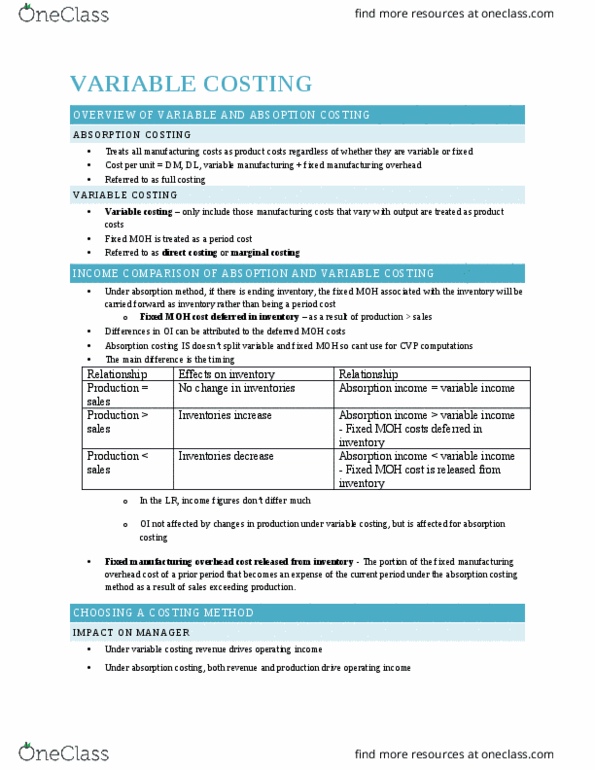

Variable costing focuses on cost behaviour, clearly separating fixed from variable costs: strength is that it harmonizes w both the contribution approach and cvp concepts discussed. Treats all manu costs as product costs, regardless if they are variable or fixed. Cost of a unit of product consists of dm, dl, and both var and fixed mo. Allocates a portion of fixed mo cost to each unit of product, along w var manu costs. A cost of unit in inv or cogs does not contain any fixed overhead cost. Referred to sometimes as direct costing or marginal costing. Are always treated as period costs (exps) and deducted from revs as incurred. Under absorption costing: all manu costs, variable and fixed, are included when determining the unit product cost. Under variable costing: only the variable manu costs are included in product costs. The diff btwn abs costing and var costing centres on timing.