STA457H1 Lecture Notes - Time Series, Independent And Identically Distributed Random Variables

Document Summary

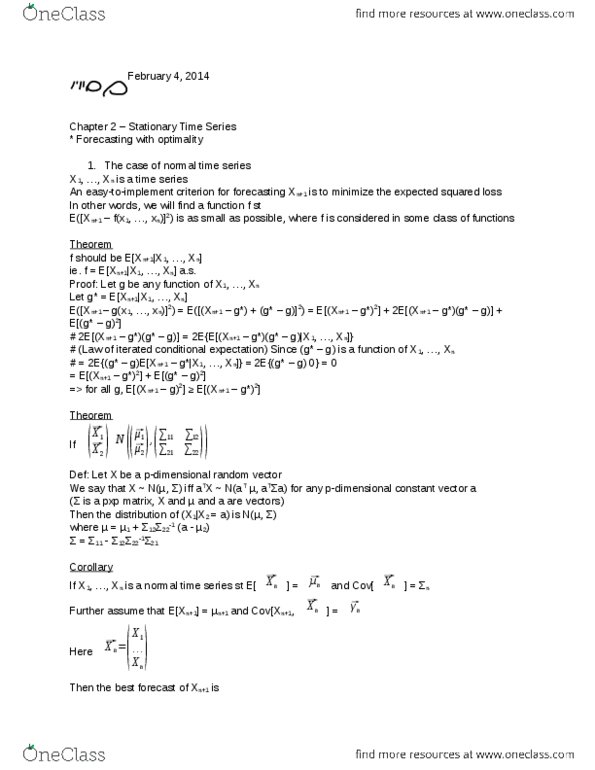

A sequence (maybe multivariate) which is naturally ordered in time is called a time series. {xt} to denote time series t can be continuous or discrete. Data observed closely in time tend to be dependent far away in time tend to be independent. The purpose of time series analysis: to forecast, to extract signals (smoothing, classification. Greedy goal: to model the joint distribution of the time series. Suppose {x1, x2, , xn} is the observed time series. F(x1, x2, , xn) = p(x1 x1, x2 x2, , xn xn) *if goal is to forecast next observation optimally in a certain sense, then the first and second moments of the joint distribution is sufficient. Second moments: vi,j = cov(xi,xj) 1 i j n. *stationarity (weak) stationarity: if: 1 = 2 = = n = , vi,j = vi+k,j+k for any i, j, k. Cov(xi+k,xj+k) = 0 if i j, var(xi) if i = j.