ACT370H1 Lecture Notes - Compound Interest, Call Option, Candela

Document Summary

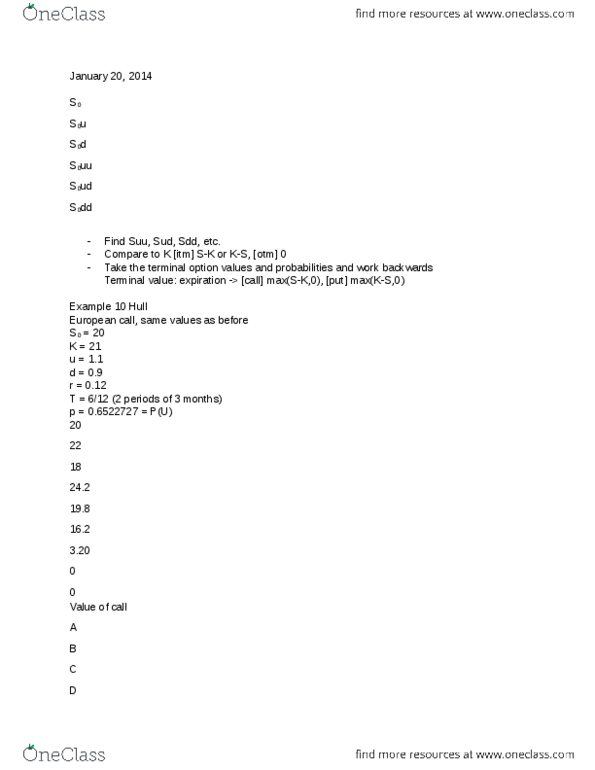

Portfolio a = portfolio b assets u+v+w+x+y = g+h+i+j. 18 = 18/4 = 22/4 1 = 4. 5 = b*r. S c = b => c = s b. P(d) = q so that we would be indifferent towards portfolio a or b. 22p + 18q = 20e0. 12*(3/12) q = 1 p. 4p + 18 = 20e0. 12*(3/12) p = 0. 6522727 = p(u) q = 1 p = 0. 3477273 = p(d) C(0) = [(0. 6522727) max(su k, 0) + 0. 3477273 max(sd k, 0)]*e-0. 03 = 0. 6329951. = c/ s or cu(t) cd(t) / su(t) sd(t) P(u) = p = sr sd / su sd = downside spread/total spread = r-d / u-d d < r < u. T = 1 year hence r = 0. 08. B: buy =2/3 shares stock and borrow . 462 at risk free. C(t) will be 60-40=20 or 0 max(60-40, 0) or max(30-40, 0) B = (2/3)(60) or (2/3)(30) 20 have to repay 18. 462*adf.