BU247 Chapter Notes -Operating Cash Flow, Cash Flow Statement, Budget

Document Summary

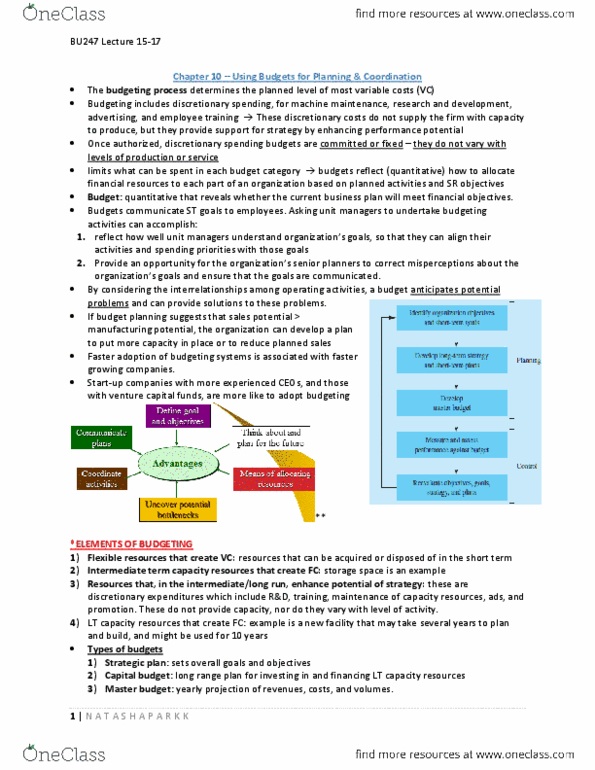

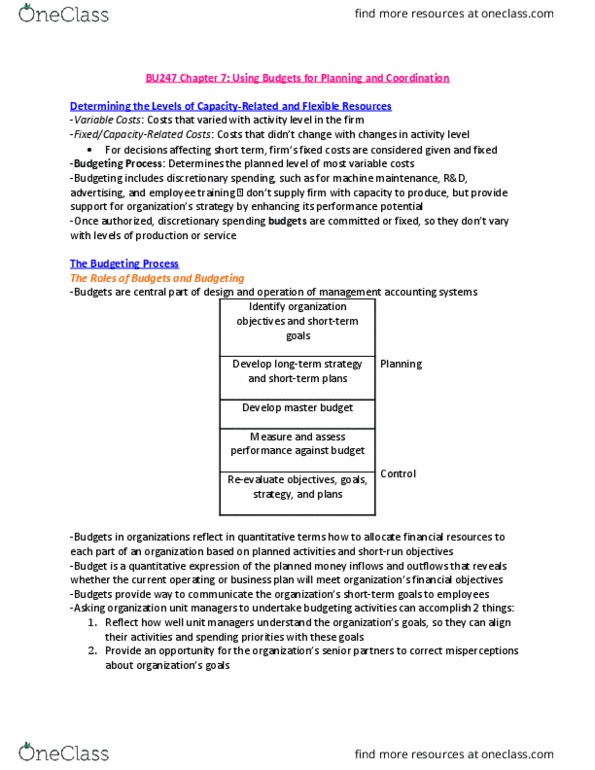

Chapter 10 using budgets for planning & coordination. The budgeting process determines the planned level of most variable costs (vc) Budgeting includes discretionary spending, for machine maintenance, research and development, advertising, and employee training these discretionary costs do not supply the firm with capacity to produce, but they provide support for strategy by enhancing performance potential. Budget: quantitative that reveals whether the current business plan will meet financial objectives. By considering the interrelationships among operating activities, a budget anticipates potential problems and can provide solutions to these problems. If budget planning suggests that sales potential > manufacturing potential, the organization can develop a plan to put more capacity in place or to reduce planned sales. Faster adoption of budgeting systems is associated with faster growing companies. Start-up companies with more experienced ceos, and those with venture capital funds, are more like to adopt budgeting.