BUSI 1003 Chapter Notes - Chapter 11: Net Income, Contribution Margin, Fixed Cost

1 May 2014

School

Department

Course

Professor

Document Summary

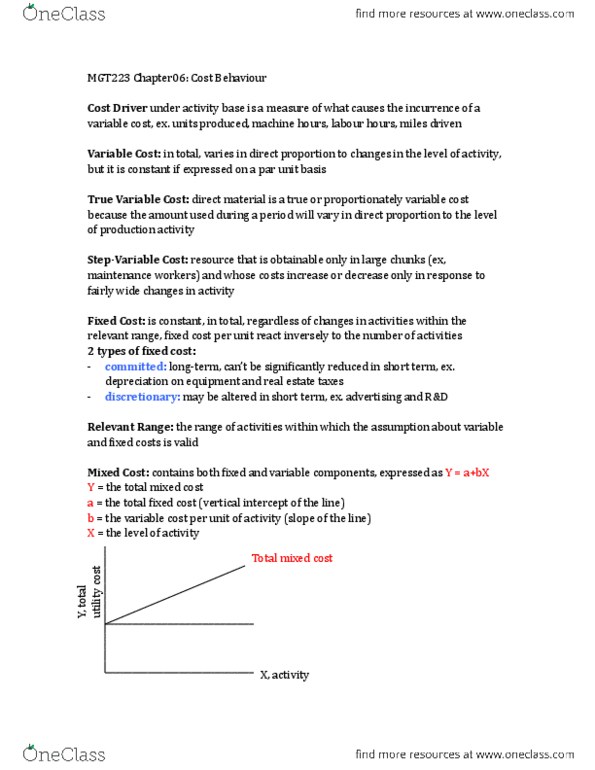

Chapter 11 - cost behaviour and cost volume profit analysis. Cost behaviour refers to the manner in which a cost changes as a related activity changes. Costs that vary in proportion to changes in the activity level. Costs that remain the same in total over the relevant range of activity, but change per unit with the level of activity. Mixed costs share characteristics of both a variable and a fixed cost: fixed over a range, then increasing based on activity. Activity bases measure of whatever causes the incurrence of variable cost. Example: direct labour hours, machine hours, units produced, Units sold, km driven, # of sq. feet, # of text messages. Relevant range range of activity of interest. Need to distinguish between fixed and variable cost components in order predict what total cost will be at a certain activity level. To isolate fixed and variable costs, use formula for a straight line: