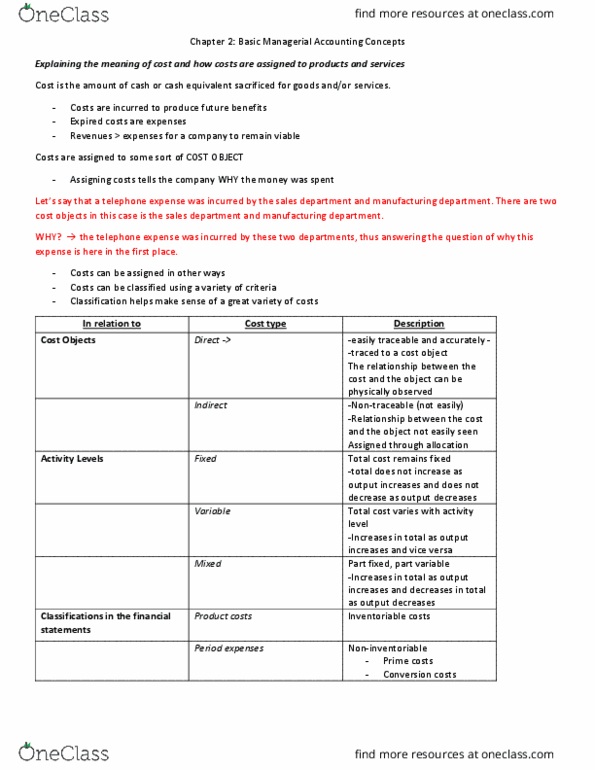

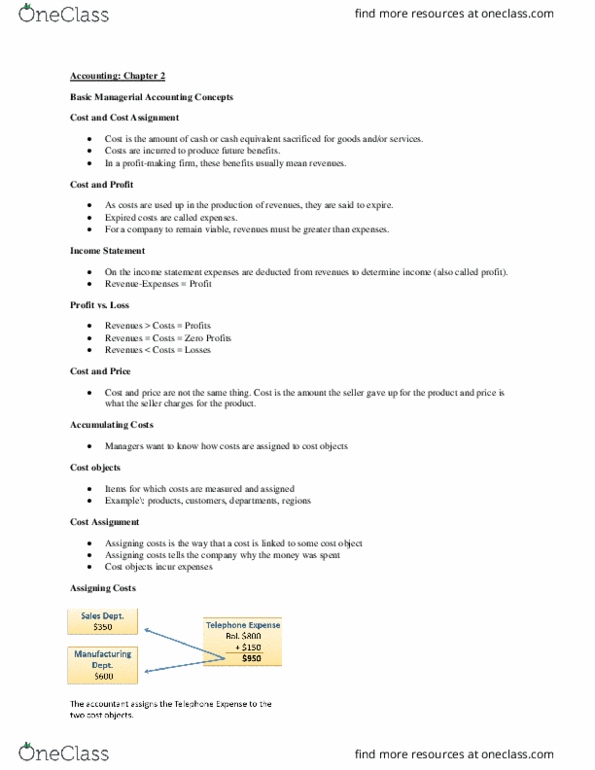

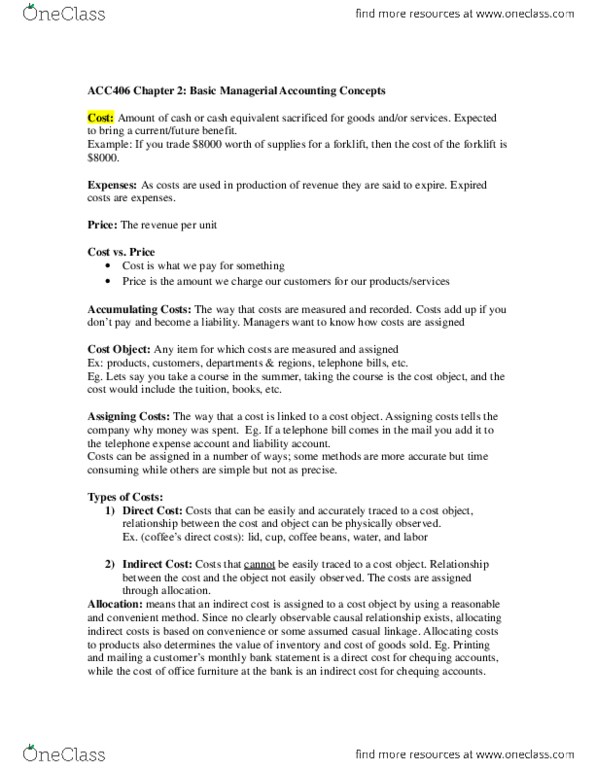

ACC 406 Lecture 2: Week 2 - Ch. 2

Document Summary

Get access

Related Documents

Related Questions

The following data are for the two products produced by Tadros Company.

| Product A | Product B | ||||

| Direct materials | $ | 14 per unit | $ | 24 per unit | |

| Direct labor hours | 0.6 DLH per unit | 1.5 DLH per unit | |||

| Machine hours | 0.5 MH per unit | 1.1 MH per unit | |||

| Batches | 125 batches | 250 batches | |||

| Volume | 10,000 units | 2,000 units | |||

| Engineering modifications | 10 modifications | 50 modifications | |||

| Number of customers | 500 customers | 400 customers | |||

| Market price | $ | 34 per unit | $ | 95 per unit per unit | |

The company's direct labor rate is $20 per direct labor hour (DLH). Additional information follows.

| Costs | Driver | |||

| Indirect manufacturing | ||||

| Engineering support | $ | 22,500 | Engineering modifications | |

| Electricity | 28,800 | Machine hours | ||

| Setup costs | 41,000 | Batches | ||

| Nonmanufacturing | ||||

| Customer service | 74,000 | Number of customers | ||

Required:

(Round your per unit cost answers to 2 decimal places and other answers to nearest whole number. Loss amounts should be indicated with minus sign.)

| ||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

5. Which method of product costing gives better information to managers of this company?

Departmental overhead rate method

Activity-based costing method

Plantwide overhead rate method

1.) When products held in inventory are sold:

A.)Cost of Goods Sold is credited.

B.)Work in Process Inventory is credited.

C.)Finished Goods Inventory is credited.

D.)Finished Goods Inventory is debited.

2.)Since manufacturing costs (direct materials, direct labor,and overhead) are incurred in the process of manufacturing units ofproduct, these costs are credited t

| A.) | The Direct Materials Inventory, Direct Labor, and ManufacturingOverhead accounts respectively. |

| B.) | Liability accounts. |

| C.) | The Work in Process Inventory account. |

| D.) | The Cost of Goods Sold account. |

3.)Management accounting systems are designed to assistorganizations in the performance of all of the following functionsexcept:

| A.) | The assignment of decision-making authority over companyassets. |

| B.) | Planning and decision-making. |

| C.) | Monitoring, evaluating, and rewarding performance. |

| D.) | The preparation of income tax returns. |

4.)In a schedule of cost of finished goods manufactured, thefigure for total manufacturing costs:

| A.) May be less than the cost of direct materials used. | |

| B.) May be less than the direct labor costs assigned toproduction. | |

| C.) May be less than the manufacturing overhead applied toproduction. | |

| D.) May be less than the cost of finished goodsmanufactured. |

5.) When a manufacturing company purchases raw materials orcomponent parts to be used in manufacturing finished goods, thesecosts are initially debited to:

| A.) Expense accounts. | |

| B.) Raw Materials Inventory. | |

| C.) Finished Goods Inventory. | |

| D.) Manufacturing Overhead. |

6.) The wages paid to employees working directly on a company'sproducts would be shown as a:

| A.) Credit to Direct Labor. | |

| B.) Debit to Direct Labor. | |

| C.) Credit to Work in Process. | |

| D.) Debit to Manufacturing Overhead. |

7.) Amounts credited to the Work in Process inventory accountmay best be described as:

| A.) The cost of finished goods manufactured. | |

| B.) Total manufacturing costs charged to production. | |

| C.) The cost of goods sold. | |

| D.) Direct materials purchased, direct labor costs paid, andpayments for items classified as manufacturing overhead. |

Can someone please help me fill this out?

Following a strategy of product differentiation, Arseniq Company makes a high-end Appliance, XT15. Arseniq presents the following data for the years 2016 and 2017:

2016 2017

Units of XT15 produced and sold 50,000 52,500

Selling price $500 $550

Direct materials (square feet) 150,000 153,750

Direct materials costs per square foot $50 $55

Manufacturing capacity in units of XT15 62,500 62,500

Total conversion costs $6,250,000 $6,875,000

Conversion costs per unit of capacity $100 $110

Selling and customer-service capacity (customers) 150 150

Total selling and customer-service costs $2,250,000 $2,343,750

Selling and customer-service capacity cost per customer $15,000 $15,625

Arseniq produces no defective units but it wants to reduce direct materials usage per unit of XT15. Manufacturing conversion costs in each year depend on production capacity defined in terms of XT15 units that can be produced. Selling and customer-service costs depend on the number of customers that the customer and service functions are designed to support. Arseniq had 140 customers in 2016 and 145 customers in 2017.

| Income Statement Amounts in 2016 | Revenue and Cost Effects of Growth Component in 2017 | Revenue and Cost Effects of Price-Recovery Component in 2017 | Cost Effect of Productivity Component in 2017 | Income Statement Amounts in 2017 | |

| Revenues ($) | |||||

| Direct Materials (Variable) | |||||

| Conversion costs (Fixed) | |||||

| Selling and customer service costs (Fixed) | |||||

| Operating income |