FIN 300 Chapter 2: Chapter 2.docx

15 Mar 2012

School

Department

Course

Professor

Document Summary

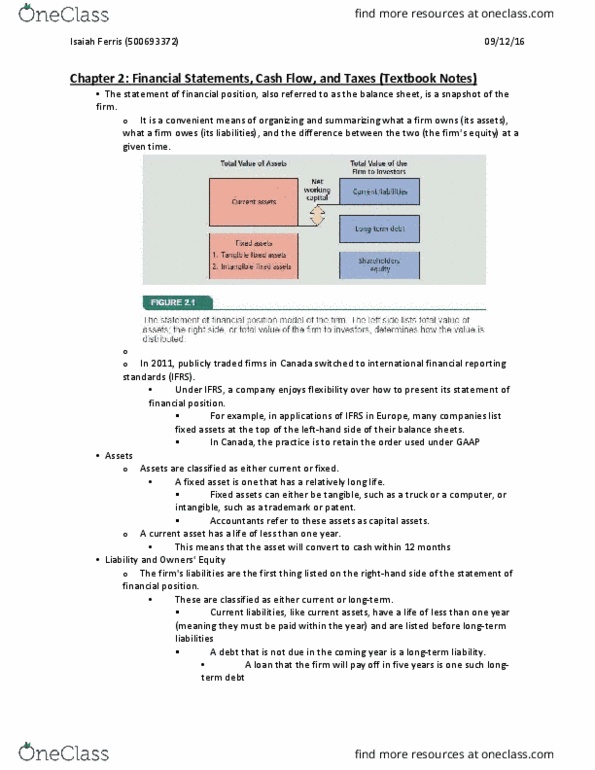

Chapter 2: financial statements: cash flow and taxes. Balance sheet f/s of accounting val on particular date, snapshot, summarize assets (owns), liabilities (owes), and equity (diff b/ 2) left side = right side. Assets = liabilities + sh equity in order of liquidity = length of time to convert to cash. Total liabilities and owners" equity reflects line of business. Current asset life less than 1 yr convert cash w/in 1 yr inventory, a/r. Fixed/ capital asset long life: tangible - truck. Liabilities and owners" equity: the right-hand side reflects use of debt. Current liabilities - life less than 1 yr / obligation paid w/in 1 yr listed b4 long term liabilities: a/p. Long term liability - debt not due w/in 1 yr sources for borrowing = bond and bondholders. Sh equity - if firm were to sell all of its assets and use $ to pay off debt --> residual val = belong to sh.