ECON 1050 Lecture : Perfect Competition

2 Apr 2012

School

Department

Course

Professor

Document Summary

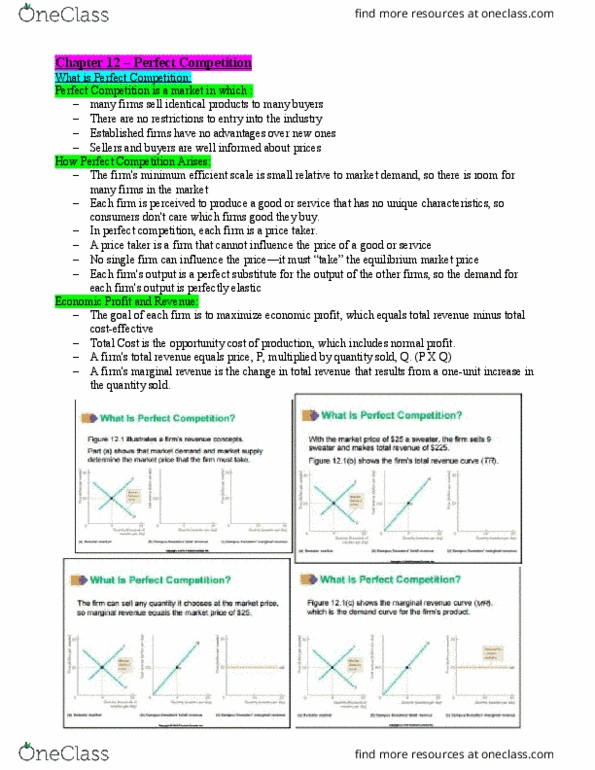

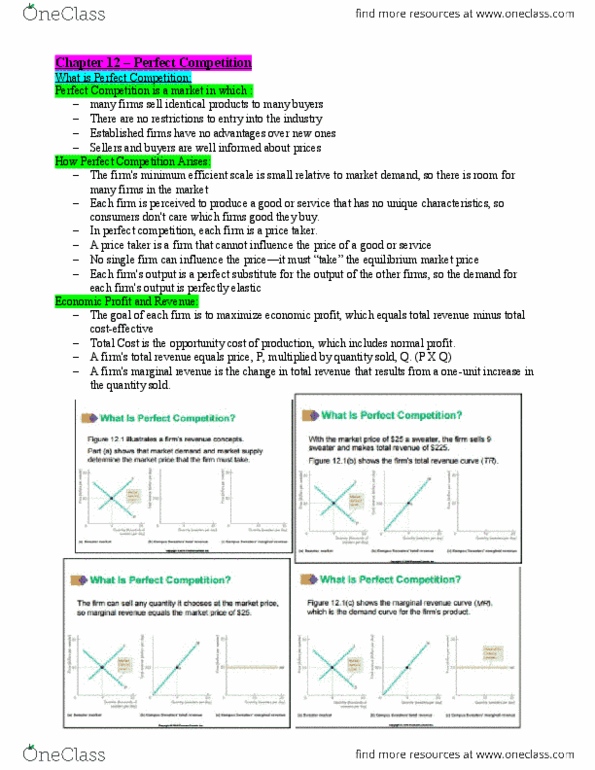

Output, price, and employment decisions in perfectly competitive markets entry and exit of firms into/from the competitive market effects of price changes, demand changes, and technological advantages. Perfect competition: industry in which: many firms sell identical products to many buyers, no restrictions to entry into the industry, established firms have no advantages over new ones. No core competency: one firm does something very well and other firms wish they had that ability. Perfect competition arises when: sellers and buyers are well informed about prices, firm"s minimum efficient scale is small relative to market demand, firm"s product is perceived as having no unique characteristics. Consumers are indifferent as to which firm to buy from. Allows room for many firms in the industry. Price takers: firm that cannot influence the price of a good or service; must. Take equilibrium market price in perfect competition, all firms are price takers. Products are perfect substitutes perfectly elastic demand.