ECON 4400 Lecture Notes - Dividend Tax, Accrual, Time Deposit

Document Summary

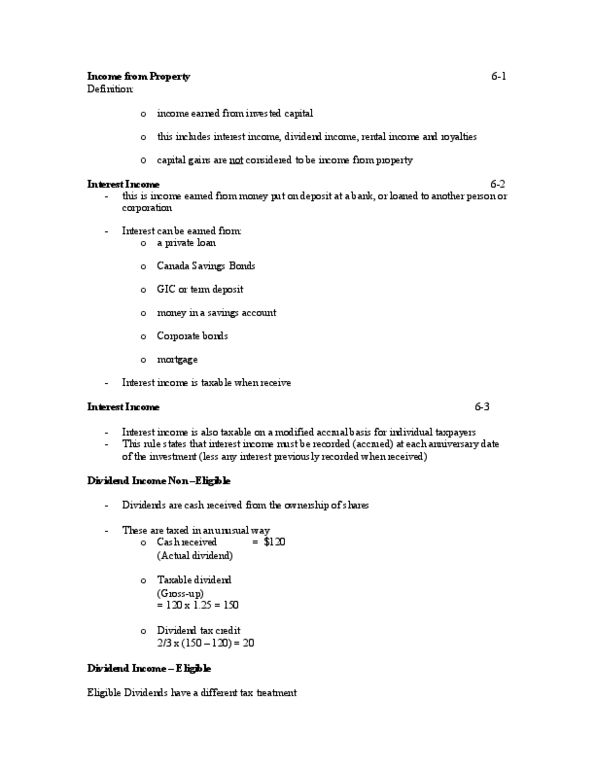

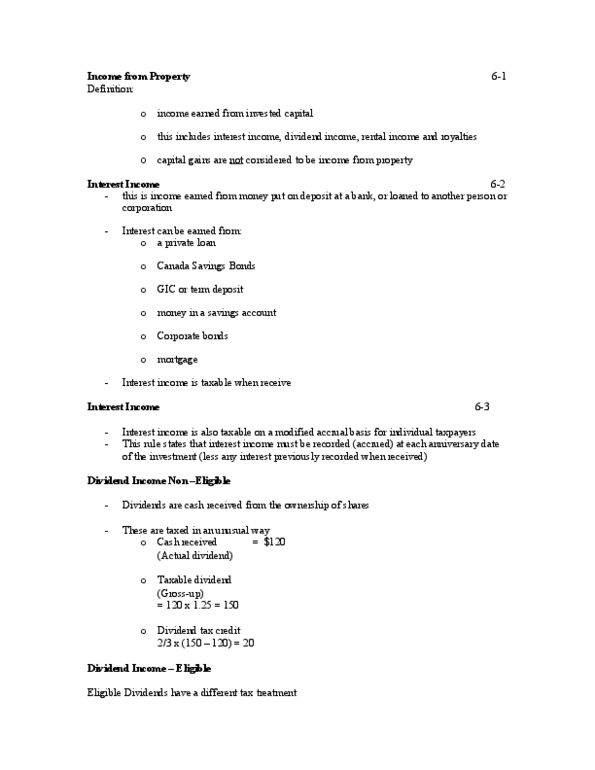

Definition: income earned from invested capital, this includes interest income, dividend income, rental income and royalties, capital gains are not considered to be income from property. Interest income 6-2 this is income earned from money put on deposit at a bank, or loaned to another person or corporation. Interest can be earned from: a private loan, canada savings bonds, gic or term deposit, money in a savings account, corporate bonds, mortgage. Interest income is also taxable on a modified accrual basis for individual taxpayers. This rule states that interest income must be recorded (accrued) at each anniversary date of the investment (less any interest previously recorded when received) Dividends are cash received from the ownership of shares. These are taxed in an unusual way: cash received = (actual dividend, taxable dividend (gross-up) = 120 x 1. 25 = 150: dividend tax credit.