BUS 426 Lecture Notes - American Institute Of Certified Public Accountants, Financial Statement, Internal Control

19 Sep 2012

School

Department

Course

Professor

Document Summary

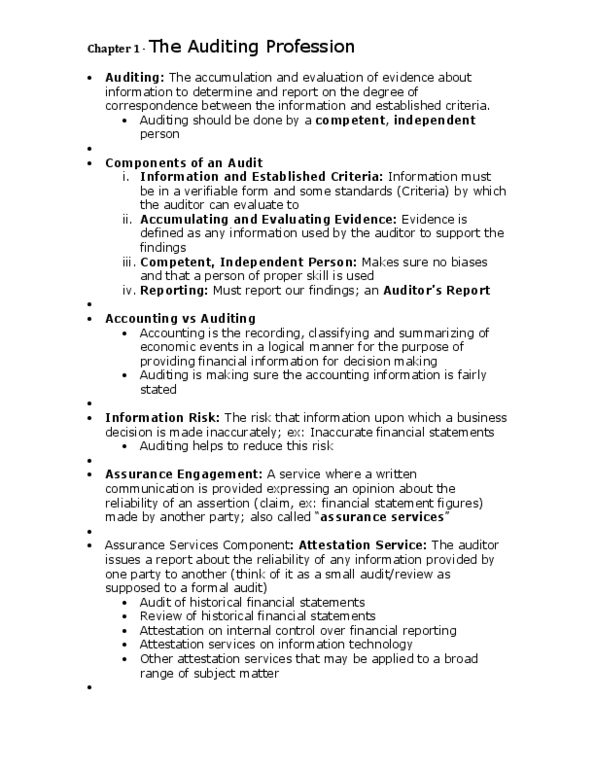

5 components of auditing: quantifiable information, criteria: example, gaap, evidence gathering + evaluate: evidence that supports the financial statement, independent, competent person: makes sure no biases, reporting: must report our findings. Audit is the accumulation (gathering evidence part) and evaluation of evidence about information by an independent and component person to determine and report on the degree of correspondence between the information and a set of established criteria. Public accountants are people who do the auditing. Public because they have the public"s trust. Auditing occurred because of: owners from the remoteness of information, biases and incentives of information provider, voluminous data, complex transactions, cost/benefit. Auditing reduces the information risk, therefore increasing auditing demand. Legal requirement as well for public companies, therefore increasing demand. Assurance services are professional services where the auditor issues a report on the reliability (free of material misstatements) of an assertion (a claim, usually existence) made by another party.