BUS 426 Lecture Notes - Lecture 5: Control Risks, Audit Risk, Stratified Sampling

19 Sep 2012

School

Department

Course

Professor

Document Summary

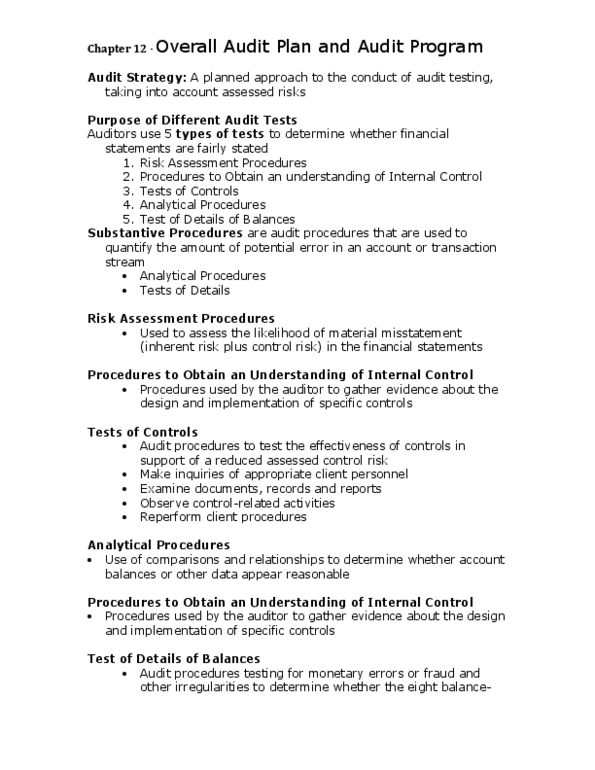

Audit strategy, a planned approach to conduct audit testing, taking into account risks. Therefore, it is developed after the client risk profile is complete. *dual-purpose test, a test of control and a test of details. Performed at the beginning of the audit planning and end of audit, the going concern and reasonableness of amounts. Procedures are selected for each amount and for each balance-related audit objectives within each account. Sampling, a method of obtaining information that will allow an estimate of the value of quantity of a population (n) by examining only a portion (n) of that n. Done for test of controls and test of details. There is always a sampling risk, which is there because you are not testing the whole n. Non-sampling risk, you use an ineffective auditing procedure or a failure to recognize an exception. Statistical sampling, uses probabilities for selecting and evaluating n from n. Statistical calculation to measure + express results.