BU227 Chapter Notes - Chapter 7: Bank Statement, Internal Control, Non-Sufficient Funds

Document Summary

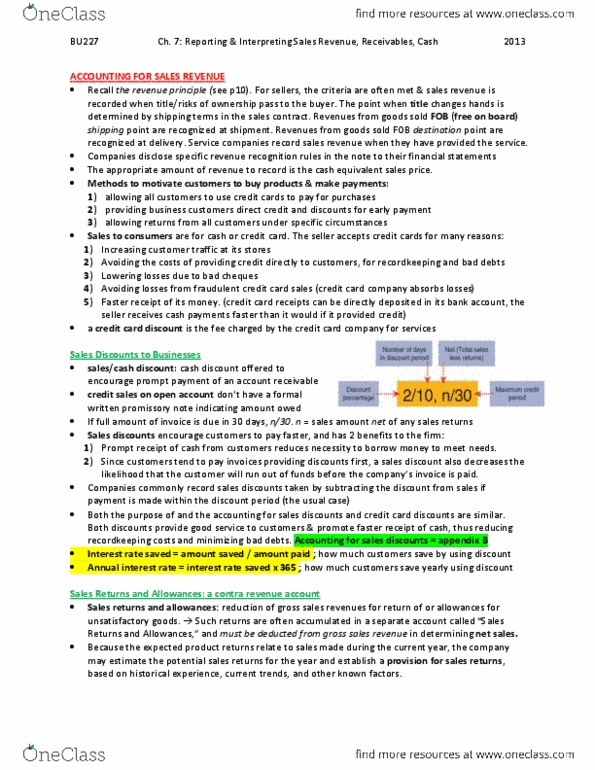

The revenue principle requires that revenues be recorded when the following conditions are met: the entity has transferred to the buyer the significant risks and rewards of ownership of the goods. For sellers of goods, these criteria are most often met and sales revenue is recorded when title and risks of ownership pass ot the byer. Free on board shipping point when goods are shipped, the title changes hands at shipment and the buyer normally pays for shipment. Free on board destination point the title changes hands on delivery, and the seller normally pays for the shipment. Revenues from goods sold fob shipping point are normally recognized at shipment and for destination vice versa. Service companies most often record sales revenue when they have provided services to the buyer. The appropriate amount of revenue to record is the cash equivalent sales price. Revenue from long-term service contracts is recognized most often by using the percentage of completion method.